US April CPI Preview: How will inflation data influence Fed rate outlook?

- Annual CPI inflation in the US is forecast to stay unchanged at 5% in April.

- Markets are fairly certain that the Fed leave its policy rate unchanged in June.

- Monthly Core CPI reading could influence the Fed's rate outlook.

Inflation in the US, as measured by the change in the Consumer Price Index (CPI), is forecast to stay unchanged at 5% on an annual basis in April. The Core CPI, which excludes volatile food and energy prices, is expected to rise 5.5% in the same period, compared to the 5.6% increase recorded in March.

Since the year-on-year rate of inflation is subject to base effects, investors will pay close attention to monthly figures to see whether price pressures remained uncomfortably high in April.

Market implications

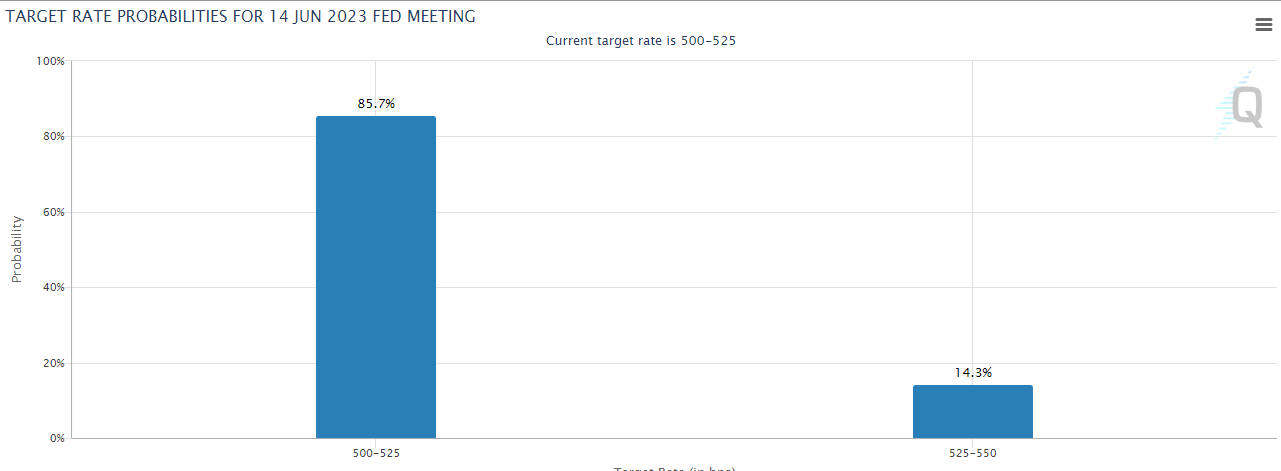

The US Federal Reserve (Fed) raised its policy rate by 25 basis points (bps) to the range of 5-5.25% as expected following the May policy meeting. The US central bank stopped using the language saying "some additional policy firming may be appropriate” in its policy statement and revived expectations for a pause in the tightening cycle in June. Although FOMC Chairman Jerome Powell left the door open for one more rate increase by reiterating the data-dependent stance, it failed to persuade investors. According to the CME Group FedWatch Tool, markets are pricing a nearly 90% probability that the Fed will leave its interest rate unchanged at the upcoming policy meeting.

The US Dollar (USD) suffered heavy losses against its major rivals in the Fed aftermath last week and the US Dollar Index (DXY), which tracks the USD’s performance against a basket of six major currencies, came within a touching distance of the multi-month low it set below 101.00 in mid-April. The risk-averse market environment at the beginning of the new week helps the USD stage a rebound but a steady advance in the DXY depends on hawkish bets making a comeback after the US inflation report.

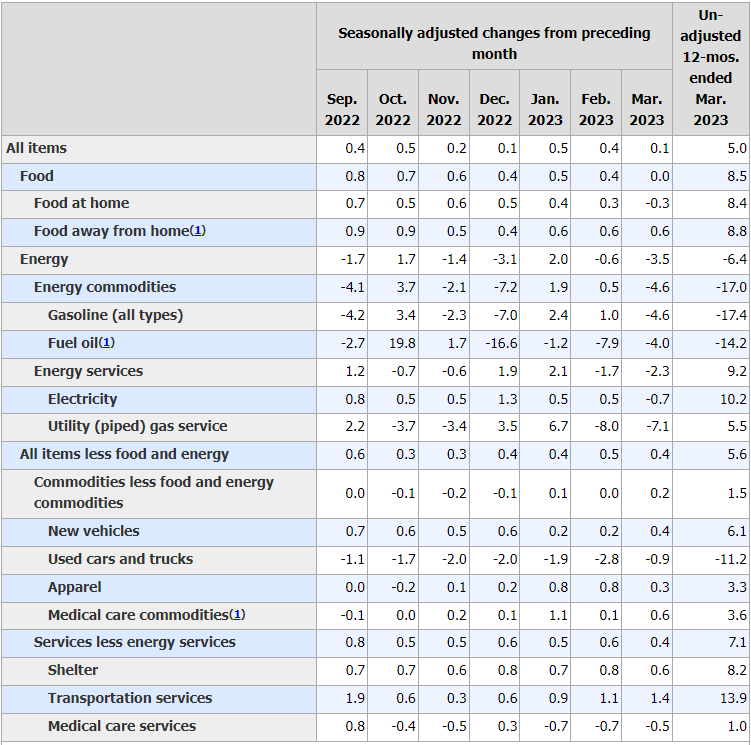

The CPI and the Core CPI are both estimated to increase 0.4% on a monthly basis. In March, the index for shelter, which makes up about a third of the Core CPI, was by far the biggest contributor to the month-on-month increase in the CPI. Hence, a stronger-than-expected monthly inflation reading by itself might not be able to convince markets of one more Fed rate hike in June if the shelter index, which tends to reflect price changes with a lag due to the contract lengths, remains as the dominant factor. In case Core CPI rises more than expected while shelter prices increase at a softening pace, investors could reassess the Fed’s policy outlook and lean toward a rate hike in June. In that scenario, the USD should continue to gather strength against its peers in the near term.

Source: bls.gov

On the other hand, a lower-than-expected increase in monthly Core CPI should allow markets to continue to position themselves for a Fed policy shift and put the USD under renewed selling pressure.

Earlier in the week, the Fed’s Senior Loan Officer Opinion Survey on Bank Lending Practices reminded investors of tightening financial conditions. The Fed’s quarterly publication showed that survey respondents noted “tighter standards and weaker demand for commercial and industrial loans to large and middle-market firms”. Banks also reported that demand for all commercial real estate loan categories was weakening. “On balance, banks widely reported expecting to tighten their lending standards over the rest of the year,” the Fed further noted. The Fed is yet to fully understand the impact of the recent banking crisis on economic activity but a soft core inflation reading in April should buy the Fed some time before it decides whether it has reached the terminal rate.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Eren Sengezer

FXStreet

As an economist at heart, Eren Sengezer specializes in the assessment of the short-term and long-term impacts of macroeconomic data, central bank policies and political developments on financial assets.