- Private payrolls expected to revert to trend in December.

- Two weak months, September and November have not carried through to NFP.

- Labor market growth remains a bulwark of the US economy.

Automatic Data Processing (ADP) the US private payroll processing company will release its National Employment Report for December on Wednesday January 8th at 13:15 GMT, 8:15 EDT

Forecast

Payrolls for ADP’s clients are predicted to have added 160,000 new workers in December after November’s gain of 67,000 and October’s rise of 121,000.

ADP and NFP: Indicator and source

The ADP payroll is most important precursor to the Employment Situation Report from the Bureau of Labor Statistics (BLS) the best known and most followed US economic statistic, commonly called non-farm payrolls or NFP for its central job figures.

The BLS report tabulates monthly figures on job creation, unemployment, wages, average work week, labor participation rates and other topics.

The ADP lists payroll changes for its corporate clients and is issued on the Wednesday before the BLS report which is usually on the first Friday of the month.

Labor Market Trends: NFP and ADP

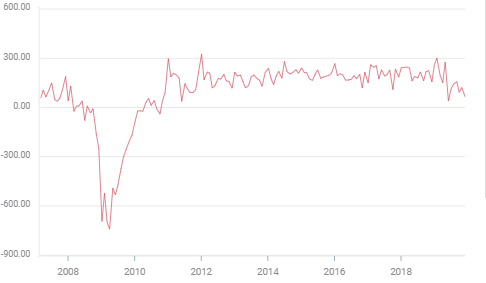

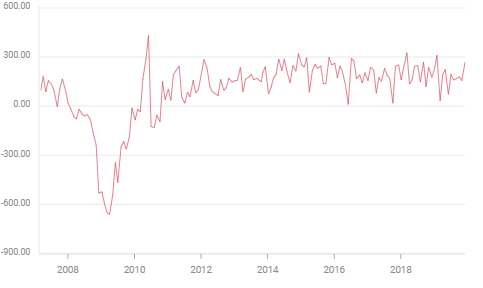

The pace of US job creation slackened last year. Non-farm payrolls dropped 22%, from 235,000 in the 12-month moving average in January to 184,000 in November. Figures from ADP fell 28% from 222,000 in April to 160,000 in November and were dragged down by three months that were well below trend, May at 46,000, June at 107,000 and November at 67,000. Only in May was there corresponding weakness in NFP at 62,000, June recorded 178,000 and November saw 266,000.

ADP Payrolls

Poor ADP numbers in May and June which averaged 77,000 coupled with the NFP average for those months of 120,000 along with the declining trend probably helped to convince the Federal Reserve that the US economy needed support from the then very active threats of the China trade dispute and Brexit. The FOMC began their three 0.75% insurance policy one month later in July.

The US labor market needs between 125,000 and 150,000 new positions each month to provide work for entrants to the work force from population growth and immigration.

NFP

Labor Market Factors: Purchasing managers’ indexes

Purchasing mangers’ indexes (PMI) in manufacturing and services have been falling since late 2018. The recurring reason given by the executives surveyed by the Institute for Supply Management was the actual and feared impact of the US-China trade war.

Overall PMI in services has fallen from 60.8 in September 2018 and 59.7 last February to 52.6 in September. It has since rebounded to 55.0 in December. The employment index dropped from 60.4 in September 2018 and 58.1 this past May to 50.4 in September and has recovered to 55.2 in December.

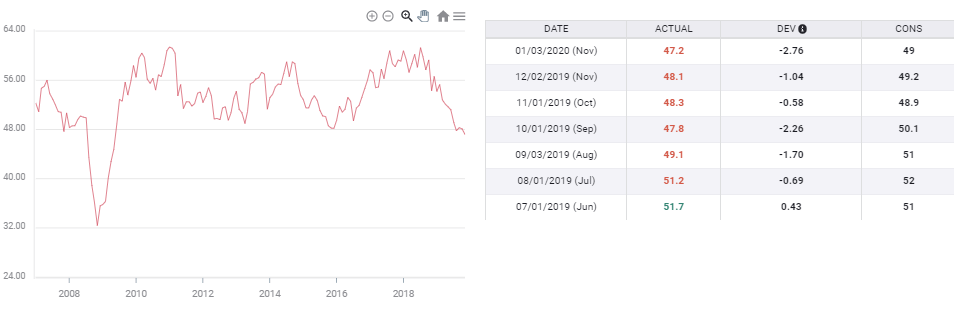

Manufacturing sentiment has declined from 60.8 in August 2018 and 56.6 in January last year to 47.2 in December. It has been below the 50 contraction mark for five straight months. December’s expected bounce from 48.1 to 49.0 did not materialize. The employment index crested last year at 57.5 in March dropped below 50 in August at 47.4 and has continued lower to 45.1 in December which is the lowest since January 2016.

Manufacturing PMI

FXStreet

Three factors are notable about the decline in business sentiment and the performance of the labor market. The first is that even though business executives have said that they are increasingly concerned about the future, their hiring decision have reflected US economic growth of 2.4% and a tight labor market. They are responding to actual demand and not their own concerns.

Second is if job creation of 150,000 a month is necessary for work force expansion, the US economy has throughout the past year found more jobs than workers. The five decade low unemployment rate of 3.5% is evidence.

Finally the US-China trade dispute has been mitigated with the deal set for signature in Washington on January 15, but positive effects are likely still a few months away.

Conclusion

Job creation in the US economy has fallen from its exceptionally high levels of 2018 but gives no indication of having run its course.

Even the manufacturing sector, whose overall and employment indexes have been in contraction for five months through December has created jobs throughout 2019. The 12-month moving average dropped from 22,000 in January to 11,000 in September, 4,100 in October and 6,000 in November. Factories are forecast to add 5,000 job in December.

Private sector payrolls from the NFP report have a similar profile. The 12-month the average peaked at 224,000 in January, had fallen to 166,000 by October and bounced to 170,000 after November’s 254,000 figure.

Coincident labor markets statistics also give no indication labor market stresses.

The 4-week moving average for initial jobless claims has risen about 20,000 since the end of the third quarter, from 213,000 in late September to 233,000 in the final week of the year. This gain however comes from lows not seen in 50 years and at the current level, which is the highest for the average since early 2018, the average remains below all rates from January 2018 to April 1973. Over the past five years the rate has moved higher in like fashion five times without signaling a shift in the job market.

Wages and compensation are near the best levels in a decade, notice that employers must offer good wages to secure scarce employees.

Federal Reserve Chairman Jerome Powell cited the desire to keep the labor market healthy as one of the motivations for the bank’s three summer and fall rate cuts. November’s excellent NFP may be proof that the Fed’s fears were misplaced or that its rate policy provided extra juice for the economy. Either way the governors will watch the ADP and NFP results carefully.

Likewise for currency traders the two jobs numbers are often a signal for immediate dollar direction

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended Content

Editors’ Picks

AUD/USD holds gains near 0.6250 but upside appears limited

AUD/USD remains on the front-foot near 0.6250 following the previous day's good two-way price swings amid confusion over Trump's tariff plans. The Aussie, meanwhile, remain close to over a two-year low touched last week in the wake of the RBA's dovish shift, China's economic woes and US-China trade war fears.

USD/JPY: Bulls retain control above 158.00, Japanese intervention risks loom

USD/JPY is off multi-month top but stays firm above 158.00 in the Asian session on Tuesday. Doubts over the timing when the BoJ will hike rates again and a broad-based US Dollar rebound, following Monday's Trump tariffs speculation-led sell-off, keep the pair supported ahead of US jobs data.

Gold traders appear non-committal ahead of US jobs data

Gold price is battling the short-term critical barrier at around $2,635 early Tuesday, consolidating the two-day corrective decline from three-week highs of $2,665. Gold traders refrain from placing fresh directional bets ahead of the top-tier US ISM Services PMI and JOLTS Job Openings data.

Solana Price Forecast: Open Interest reaches an all-time high of $6.48 billion

Solana price trades slightly down on Tuesday after rallying more than 12% the previous week. On-chain data hints for rallying continuation as SOL’s open interest reaches a new all-time high of $6.48 billion on Tuesday.

Five fundamentals for the week: Nonfarm Payrolls to keep traders on edge in first full week of 2025 Premium

Did the US economy enjoy a strong finish to 2024? That is the question in the first full week of trading in 2025. The all-important NFP stand out, but a look at the Federal Reserve and the Chinese economy is also of interest.

Best Forex Brokers with Low Spreads

VERIFIED Low spreads are crucial for reducing trading costs. Explore top Forex brokers offering competitive spreads and high leverage. Compare options for EUR/USD, GBP/USD, USD/JPY, and Gold.