Unraveling the German housing market: Inflation, interest rates, and the perfect storm

Germany’s housing market, once the poster child of stability, is currently facing a significant crash. This sudden turn of events has left many wondering about the role of inflation and interest rates in this turmoil.

For several years, Germany enjoyed a booming housing market. Low-interest rates, robust economic growth, and a steady stream of international investors fuelled a surge in property prices. However, this upward trajectory was unsustainable.

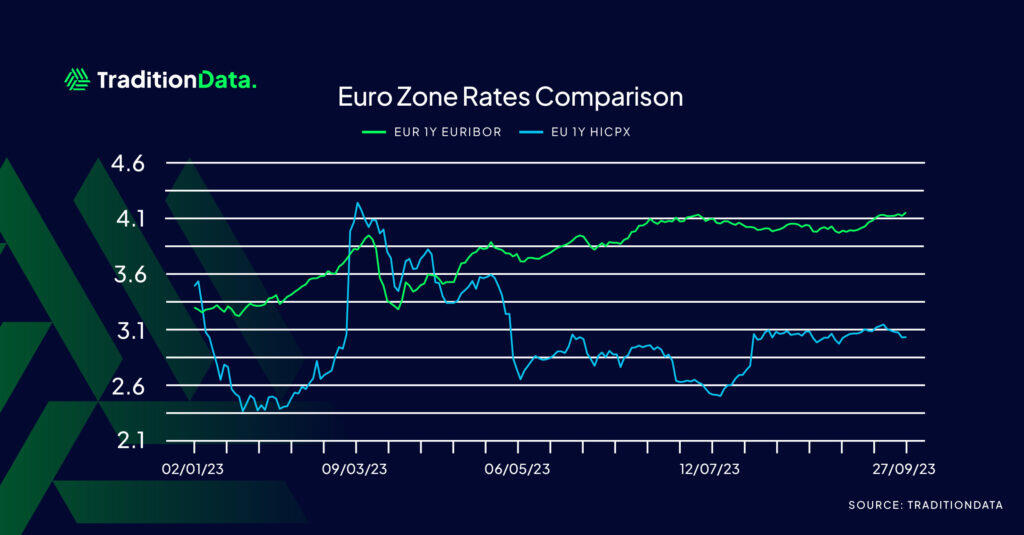

Inflation is a critical driver of housing market dynamics. Low and stable inflation tends to boost confidence in the economy, making property investments attractive. However, a sudden spike in inflation can erode purchasing power, making people wary of investing in real estate. Moreover, central banks may respond to high inflation by raising interest rates to control economic overheating, which can dampen property demand and prices.

Interest rates are the lifeblood of the housing market. They dictate the cost of borrowing, influencing both homebuyers and property investors. Germany, being part of the Eurozone, relies on the European Central Bank (ECB) to set interest rates. For years, the ECB maintained historically low rates to stimulate economic growth and combat deflationary pressures. This policy contributed to the housing market bubble.

Low interest rates make borrowing cheap, helping demand for homes and enticing investors into real estate. However, when interest rates start to rise, it can cool down the housing market by making borrowing more expensive, which exerts downward pressure on property prices.

The German housing market crash began when inflation rates started to climb, causing the ECB to consider raising interest rates. Simultaneously, the government introduced stricter regulations on real estate investment, primarily in hotspots like Berlin and Munich, aiming to curb skyrocketing prices.

The convergence of rising inflation, the threat of higher interest rates, and regulatory adjustments created the perfect storm. Investors began exiting the market, leading to a sharp drop in property prices. This, in turn, could see some homeowners left with substantial mortgages trapped in negative equity.

The German housing market crash is a multi-faceted issue with intertwined economic factors at play. While inflation and interest rates played substantial roles in the bubble’s formation and eventual burst, regulatory changes and market sentiment also contributed significantly. This crisis serves as a stark reminder of the delicate balance between economic growth, inflation, and interest rates in the realm of real estate. As Germany grapples with the aftermath, it underscores the importance of prudent policies and vigilance to maintain a sustainable housing market.

Author

Ian Sams

TraditionData

Ian has run both IT and Market Data support teams at TraditionData. He then moved to Refinitiv to work as a relationship manager/sales specialist, looking after the large European Hedge Fund accounts.