United States: The Fed tries to prevent the money markets from potentially drying up

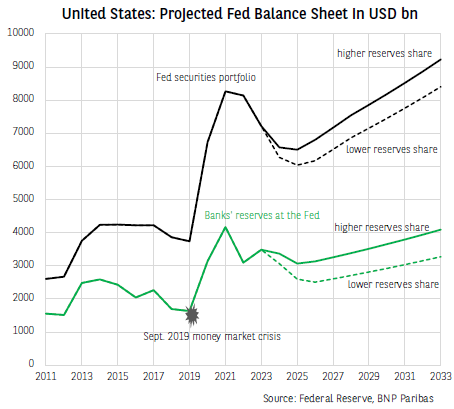

After being left reeling by the unexpected money market crisis during its first round of quantitative tightening (QT1), the Federal Reserve (Fed) intends to manage the reduction of its balance sheet better. This means destroying some of the reserves held by banks at the Fed without triggering a shortage in central bank money, given the liquidity requirements imposed on banks. Since the start of its second round of quantitative tightening (QT2) on 1 June 2022, the reallocation of money market funds holdings, outside of the Fed’s reverse repo facility (USD -1.38 trillion as at 8 May 2024), has helped to absorb the effects of the reduction in the Fed’s balance sheet (USD -1.56 trillion) on bank reserves (USD -30 billion), thereby delaying the risk of a central bank money shortage. However, the liquidity pool that will be able to absorb the QT2 shock is now smaller (money market funds’ “deposits” in the Fed stood at 460 billion on average in early May).

Given how difficult it is to estimate the optimal amount of reserves1 required for the money markets to operate smoothly, the Fed is being extra careful. On the one hand, it announced that it would reduce its balance sheet at a slower pace starting from 1 June.2 On the other hand, it has revised its analytical framework. From now on, it characterises an «ample» reserves system as one with a reserve-to-GDP ratio slightly above the level recorded in September 2019 (8% in the first scenario), or even more (10% in the second scenario). The Fed believes that in order to avoid a shortage in reserves, QT2 should be curtailed, in the case of the high scenario, in early 2025. By that time, the central bank’s balance sheet should be around USD 6.5 trillion (22% of GDP) and reserves should be around 3.4 trillion (11% of GDP). At the end of a year in which the Fed’s balance sheet size is expected to remain stable, the asset purchase programme would be reactivated in order to keep the stock of reserves at 10% of GDP.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.