United States: Leading indicators, the labour market and the recession narrative

Despite the ongoing good pace of job creation and slower wage increases, which through their impact on inflation could influence future Fed policy, there is enough ambiguity in the recent data to fuel the debate on whether the US will end up in recession or not. The survey of professional forecasters points towards heightened recession risk and so do the inversion of the yield curve and the downtrend of the Conference Board’s index of leading economic indicators. If this index were to decline further, one would expect, based on the past relationship, a significant weakening in the monthly payroll numbers whereby the narrative that a recession is around the corner would gather force.

The latest US labour market report has been welcomed by investors. In December, the growth of average hourly earnings slowed down to +0.3% versus the previous month and to +4.6% year-over-year rate (+4.8% in November), hinting at easing wage pressures, whereas the monthly pace of job creation -223.000 new jobs remained strong.

It is tempting to call it goldilocks, but that would be too generous and not really appropriate. On the wage front, other measures such as the employment cost index and the Atlanta Fed wage tracker, although having eased, continue to show strong increases. In terms of job creation, the trend is down and fewer sectors than before are still creating jobs. Concerning the economic outlook more generally, the ISM surveys for December were sobering. The manufacturing index declined to 48.4 and the services index dropped from 56.5 to 49.6.

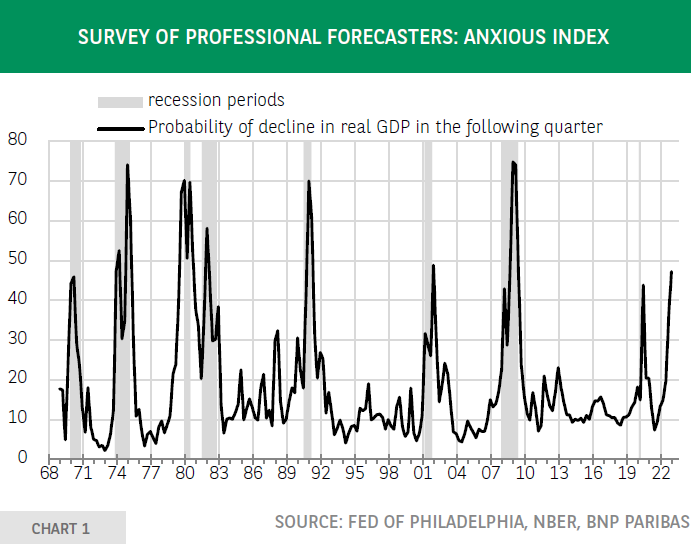

In summary, there is enough ambiguity in these data to fuel the debate on whether the US will end up in recession or not. Evaluating this risk is a tricky and very judgmental exercise that requires making a call about the reaction function of households and firms to economic shocks last year’s jump in inflation, rising interest rates, etc. and the ensuing impact on income expectations, confidence, company profits, etc. Looking at stylized facts is also important. Based on the historical record, the inversion of the yield curve points towards a recession. The anxious index -a survey amongst economists of the likelihood of the US entering a recession in the next quarter has reached a level that in the past has always been followed by a recession (chart 1).

The Conference Board index of leading indicators is another important input. Based on its cumulative decline since its most recent peak February 2022, it seems that the likelihood of recession is increasing. However, the ongoing strong pace of job creation suggests that a recession is not imminent, so the question is when the situation might change.

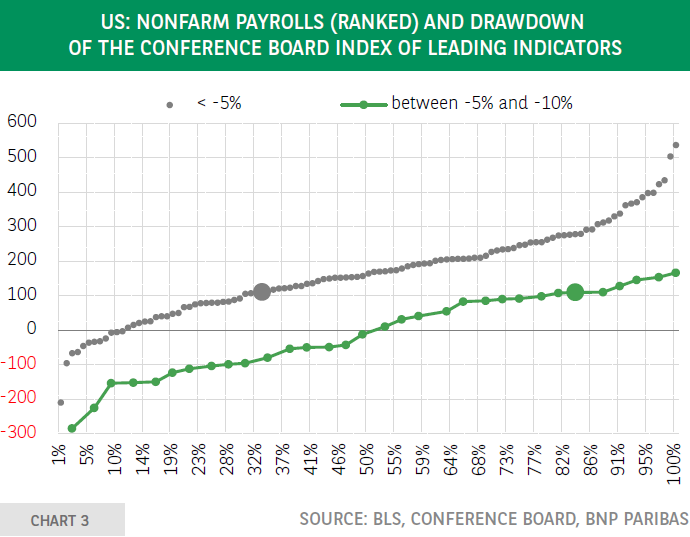

The historical correlation between the Conference Board’s index and job creation allows to shed light on this. Chart 2 shows the relationship between the drawdown of the index of leading indicators -the decline in percent since its historical peak- and the monthly nonfarm payrolls. If the former would continue to decline in the coming months, one should expect, based on the past relationship, a further slowdown in the pace of monthly job creations.

As illustrated by chart 3, when the drawdown is between 0% and -5% (blue dots), in 33% of observations, monthly job creation has been at 110.000 or lower. When the drawdown has been between -5% and -10%, this number rises to 84%. Inevitably, when the frequency of low nonfarm payroll numbers increases, the narrative that a recession is around the corner will gather force.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.