United States: About the tightening of us monetary policy

Raising key rates in response to a pure energy or food prices shock is a monetary policy mistake that was already committed in 2008. At the time, the Bank of England and the European Central Bank (ECB) raised the cost of borrowing in response to surging oil prices (Brent crude oil rose as high as USD 140 a barrel in summer 2008), just as the subprime crisis was gathering strength and undermining economic prospects. What happened next is well known: after the bankruptcy of Lehman Brothers in September, key rates had to be slashed, right after they were raised. On 16 March 2022, the Federal Reserve announced a new round of monetary tightening in the midst of an energy crisis, even as Russia is waging war on Ukraine. Is the Fed about to make the same policy mistake?

A period of exceptionally accommodating monetary policy comes to an end

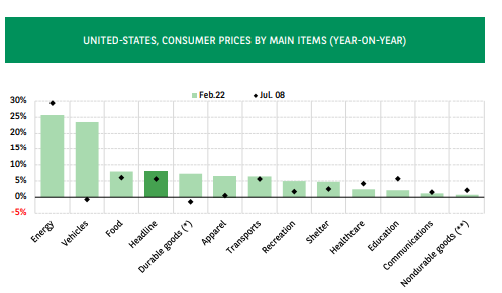

The initial situations of these two periods seem to be very different. First, inflation was not the same. At 7.9% year-on-year in February 2022, inflation is the highest in forty years and stands 2.3 points above the July 2008 peak of 5.6%. It has also spread much more widely. Far from being fuelled solely by surging energy and food prices1, price increases have spread to numerous items, including rents or even more durable goods, foremost of which are cars (see chart 1).

Exacerbated by the global Covid-19 pandemic, price increases have cut short a historical downward trend resulting from two decades of supply chain globalisation.

Lastly, and most importantly, the Fed’s decision comes at the end of an exceptionally accommodating phase of monetary policy, unprecedented in modern US history. Maintained near the lower zero bound since March 2020, real interest rates have plunged into negative territory, sinking to depths never seen before (see chart 2). This was also the case for bond yields, which remained very low thanks to the central bank’s securities purchases. The last wave of quantitative easing (QE), which amounted to USD 4,600 billion (20 points of annual GDP), fuelled exceptional money supply growth and helped rekindle inflation, addition to the supply shock (see chart 3 and Wolf, 20212 ).

The Fed met its initial goal of avoiding liquidity shortages and countering the depressive effects of the Covid-19 pandemic, and the economy recovered beyond all expectations. It has largely surpassed pre-pandemic levels. With the jobless rate dropping below 4%, the US economy is verging on full employment. The keyword thus became the normalisation of monetary policy.

Just how far can the Fed go? According to the latest projections of the Federal Open Market Committee (FOMC), the Fed funds target rate could rise as high as 2.8% over a 15-month horizon, which implies six more rate increases of 25bp each in 2022, and at least three more in 2023. Starting in May, it will scale back the amount of securities outstanding held as part of QE (USD 8,500 bn), at a pace that has to be specified. As presented, the Fed’s current road map is much more demanding than the December 2021 version. In the eyes of Fed Chair Jerome Powell, this road map is workable because the US economy is back to full health.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.