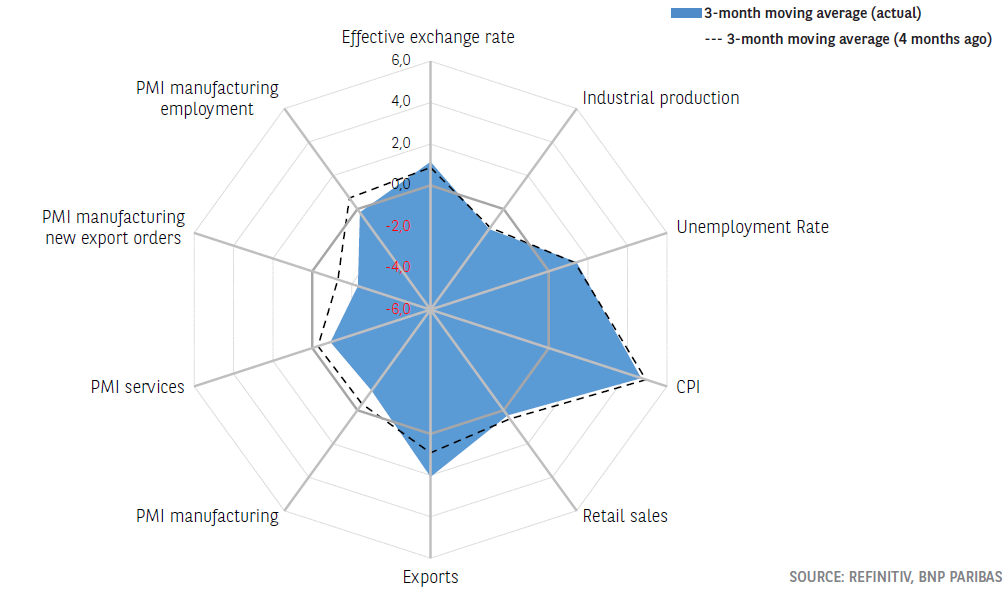

United Kingdom: Peak inflation?

UK inflation finally fell in November to +10.7% y/y (+0.4% m/m), compared with +11.1% in October (+2% m/m). Other good news is that core inflation is also falling, for the first time since September 2021 (-0.2 points, i.e. 6.3% y/y). In the face of still very high inflation, however, the Bank of England (BoE) Monetary Policy Committee (MPC) decided to raise its key rate further by 50 basis points, thus bringing it to 3.5%. The rise is less significant than in November (+75 bp) as the BoE must also reconcile it with the risk of recession.

While BoE Governor Andrew Bailey said inflation had peaked, he expressed concern that UK companies would keep raising prices too fast for too long, for two reasons. In October, the upturn in inflation was mainly driven by the increase in electricity prices (+17% m/m) and gas prices (+37% m/m), despite the implementation of the energy price guarantee. This cap on energy prices did have an effect in November and mechanically helped to limit the rise in inflation. However, it is not expected to be renewed for companies from the end of March 2023. And yet the lifting of this measure should expose them to a sharp increase in their operating costs, which is likely to have a repercussion on sale prices.

Furthermore, the slowdown in the price of goods remained limited in November. The prices of food, alcoholic beverages and tobacco (+12.7% y/y, compared to 13.2% in October) and industrial goods (+14.6%, compared to 15.4%) are decelerating, but the pace of the rise remains higher than in September. Although inflation in general is expected to move gradually lower, in retail trade this evolution will probably be more limited. According to the Confederation of British Industry’s (CBI) Distributive Trades Survey (DTS), the vast majority of wholesale and retail trade companies are expecting short-term price increases, which would dampen disinflation. Inflation in services remained stable, at 6.3% year-on-year (i.e. +0.2% m/m). The CBI’s Service Sector Survey (SSS) suggests that the slower price increase is likely to continue, although the balance of responses expecting a price increase in the next three months remains particularly

high. The new hike in the BoE’s key interest rate is also increasing pressure on households: already penalised by the increase in the cost of living, their financial situation is also deteriorating due to the effect of the rise in interest rates on mortgages. However, in its Financial Stability Report (FSR), the BoE’s Financial Policy Committee (FPC) indicates that households are more resilient than during the 2007 financial crisis and the recession in the early 1990s: the proportion of disposable income spent on mortgage payments is expected to rise but remain below the record levels reached in 2007 and the 1990s.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.