UK: Budget aims for growth but easing of fiscal rules raises economic risks

The UK budget sets an ambitious growth-oriented approach, but questions remain over its ability to meaningfully boost long-run economic growth. The easing of budgetary constraints and reduced monetary flexibility pose economic risks.

UK Chancellor of the Exchequer Rachel Reeves’s strategy for the next five years emphasises economic growth partially funded through progressive policies. However, this plan faces pressure to balance interests among varying stakeholders, from traditional middle-class “Middle England” voters to business and bond markets. The strategy addresses a GBP 22bn deficit that the Labour government attributes to the previous government as well as self-imposed fiscal commitments defined during the election campaign that returned Labour to power after 14 years.

The budget marks the seventh adjustment to UK fiscal rules since just 2011 and is focused on balancing the current budget to free up resources for investment. The new target of reducing net financial liabilities by fiscal year (FY) 2029-30, rather than net debt, as a share of gross domestic product underscores the lack of a meaningful straight jacket in UK fiscal rules, especially in the post Brexit context without EU fiscal oversight.

While the debt reduction timeline was shortened from five to three years, this adjustment only affects the next government and may always be revised as appropriate. The Office for Budget Responsibility (OBR) is projecting a comparatively flat debt trajectory over the forecast horizon based on public sector net financial liabilities. But under the former public sector net definition excluding the Bank of England, the OBR anticipates that debt will rise annually, reaching 95.8% of GDP by FY2029-30, driven by the extra GBP 142bn of borrowing.

Scope Ratings (Scope) has projected an increase under a general government debt definition to exceed 110% of GDP by 2027. The easing of the budgetary rules and deferral of correcting long-run fiscal imbalances are economic concerns, as highlighted in Scope’s announcement last month affirming the UK sovereign rating at AA.

The budget’s impact on limiting central bank space for easing poses a challenge for Labour’s plans

The budget presents challenges for the Bank of England. Increased spending, higher taxes, a 6.7% rise in the minimum wage, and enhancements of workers’ rights are net inflationary. Also, businesses are hiking wages for those paid above the minimum. This has already forced the Bank to consider a more cautious approach around rate cuts after an expected 25bp reduction next Thursday.

The OBR projects higher inflation by 0.4pps next year and 2026, and inflation averaging 2.6% next year (Figure 1). That is more than 1pp above its March projections. The OBR sees inflation remaining above the 2% target until 2029. The more accommodative the Bank of England can be, the more support Reeves receives for the pro-growth agenda, offering more leeway through accommodative capital markets. Conversely, if the Bank is forced to keep rates tight and continue quantitative tightening to address elevated inflation, Labour may face challenging borrowing conditions and closer bond market scrutiny.

Ten-year Gilts have risen to above 4.4% in the aftermath of the budget statement, compared to 4.2% before the general election. The fact that the spending programme is partially funded likely prevented an even more-outsized market response to date. Markets are concerned by the budgetary expansion that will be financed predominantly by long-end supply. Reeves must maintain market confidence especially if the Bank of England’s space for intervention is reduced.

The budget aims to address many priorities including accelerating growth and improving public services. However, with borrowing at near record levels even prior to this significant budgetary loosening, long-run outcomes remain uncertain.

The tax rises are appropriate within self-imposed tax locks and signal a departure from “New Labour”

Uncertainty around tax hikes had been a drag on economic sentiment ahead of the budget. The tax rises ultimately announced were probably not as broad as many had speculated. A GBP 25bn a year (by 2029) hike of national insurance contributions for employers is the main conduit of revenue raising although the Institute for Fiscal Studies estimated net revenue from the change at a more modest GBP 16bn. The on aggregate GBP 40bn a year of added levies was more than foreseen, although any under-performance of that figure might force further tax rises and/or higher borrowing.

The budget commits to GBP 70bn (just above 2% of GDP) of added spending over the coming five years, two-thirds of which goes to current and one-third to capital expenditure. This includes a substantial investment in the National Health Service. Public spending commitments reverse Tory plans for GBP 19bn of real cuts in FY2028-29, although Reeves requested a moderate GBP 3bn of savings from government departments. Other savings had been announced pre-budget, such as scrapping winter fuel payments for most pensioners. Under Conservative plans, capital investment had been predicted to drop to 1.7% of GDP by 2029, but Reeves seeks prudently to keep this at 2.5% for new hospitals, prisons, and roads.

The OBR has projected that the combined spending and tax programme offers muted medium-run growth dividends, citing “broadly neutral” effects for potential output over a five-year horizon (to the end of the Labour term) and a net boost for the economy not arriving until the 2030s. Scope estimates potential growth of the UK economy at a conservative 1.5% a year. UK growth was nearly double this rate (2.9% on average) over the decade before the global financial crisis.

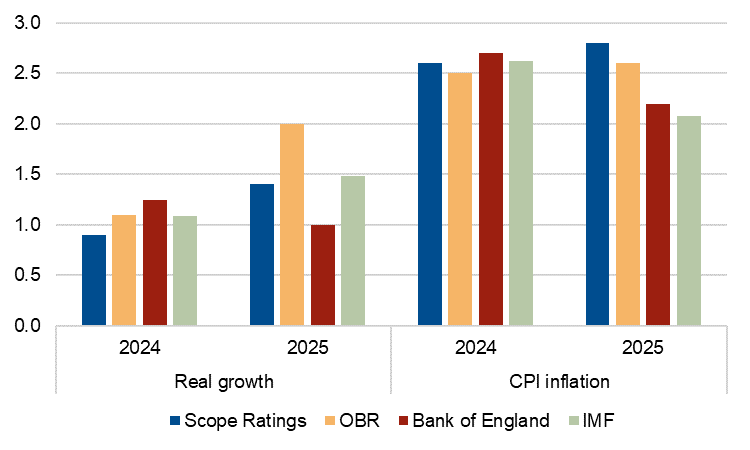

OBR growth and inflation projections for 2025: Optimistic growth but aligned with Scope on above-2% inflation

Annual growth and inflation projections, United Kingdom.

Source: OBR (Economic and fiscal outlook October 2024), Bank of England (Monetary Policy Report August 2024), IMF (World Economic Outlook October 2024) and Scope Ratings forecasts.

Scope Ratings’ projections assume lacklustre growth of 0.9% this year and 1.4% next year – only half the pace of the US economy. If realised, such near and medium-term projections may fuel criticism that the government’s performance falls short of Labour’s pre-election commitment of 2.5% annual growth, outpacing the remainder of the G-7.

Author

Dennis Shen

Scope Ratings

Dennis Shen is Chair of the Macroeconomic Council and Lead Global Economist of Scope Ratings, the European rating agency, based in Berlin, Germany.