UK inflation may finally be at its peak

With the government fixing energy prices until at least April, it looks like October's 11.1% inflation rate could mark the peak. But it's unlikely to fall below double-digits until early next year, and the Bank of England is undoubtedly worried about inflation linked to the tight jobs market. Still, a pivot back to a 50bp hike in December looks likely.

The latest rise in household energy costs was enough to take UK inflation up to 11.1% in October. That’s a bit higher than was expected, and seems to be partly explained by another punchy 2% month-on-month increase in food prices, and a little bit of upside at the core level.

All of this is marginally hawkish for the Bank of England in that its closely watched measure of ‘core services’ inflation, which excludes some volatile components and the impact of VAT changes, came in a few percentage points higher than they’d pencilled in. By our calculation, that sits slightly above 6% YoY, compared to a forecast of 5.7% by the BoE a couple of weeks ago.

As we noted yesterday, worker shortages are proving to be a persistent issue for firms, and that potentially points to stickier inflation rates for service-sector firms where pay is a key pricing input. Still, with hiring demand falling, we suspect we’re near the peak for wage growth.

In fact – famous last words – it looks like UK headline inflation is at its peak too, or there or thereabouts. The fact that the government is effectively fixing electricity/gas unit prices below wholesale costs until next April means this is probably as high as it will get, though admittedly we expect headline rates to stay in double-digits until at least February next year.

From there, we think there are compelling reasons to expect headline inflation to drift lower through the year, ending up closer to the Bank of England’s 2% target by early 2024. That’s especially true of goods categories, where lower input/shipping prices, stalling consumer demand and rising inventory levels not only point to lower inflation rates, but potentially also outright price falls in certain areas as retailers are forced to become more aggressive with discounting. The story, as we discussed earlier, is less clear-cut for services inflation.

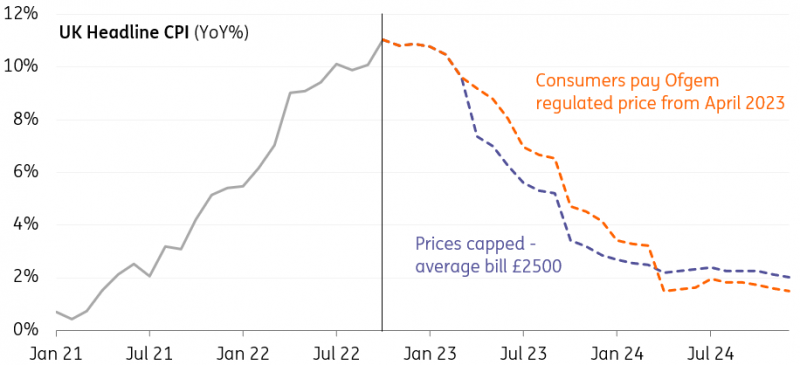

UK inflation in 2023 will depend a lot on how energy support evolves after April

source: Macrobond, ING

The 2023 inflation outlook will also heavily depend on how the government adapts energy support next year. We’re still awaiting detail, but one possibility is that the majority of households switch back to paying the Ofgem regulated price from April. Based on our latest estimates using wholesale energy costs, the average household would pay £3300 in fiscal-year 2023 without any government support, compared to £2500 if prices remain capped. That would initially bump up inflation rates after April by roughly 2pp.

While it’s tempting to say that higher headline inflation rates in that scenario would be hawkish for the Bank of England, in practice the opposite is probably true. Reduced energy support would amplify the UK recession that most, including ourselves, now expect. That would imply lower core inflation further down the line.

With signs that inflation – both in core and headline terms – is close to or at a peak, and signs of recession mounting, we think the Bank of England is likely to pivot back to hiking in 50bp increments in December. Assuming another 25-50bp hike in February, we think the peak for Bank Rate is likely to be around 4%, a little below what markets are now pricing.

Read the original analysis: UK inflation may finally be at its peak

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.