UK employment and inflation numbers ahead: GBP/USD drifting around resistance

While the UK is evading US tariffs for now, its economy continues to face a somewhat undecided future, with taxes on business set to increase in April and a lingering drag from the elevated interest rates.

However, this week’s focus shifts to a rather busy slate of economic data in the UK. Regarding tier-1 metrics, I will largely focus on Tuesday’s employment figures for December 2024 and the January CPI inflation (Consumer Price Index) report on Wednesday. The data comes on the heels of last week’s better-than-expected GDP (Gross Domestic Product) numbers for December 2024.

BoE: ‘Gradual and careful’ approach

You will recall that the Bank of England (BoE) recently cut the Bank Rate by 25 basis points (bps) to 4.50% – which did not raise too many eyebrows – and the BoE Governor signalled a ‘gradual and careful’ approach to easing policy. However, the 7-2 MPC vote split (Monetary Policy Committee) caused a stir. BoE member Catherine Mann – a known hawk – joined Swati Dhingra (dove) and voted to cut the Bank Rate by 50 bps.

The central bank also released updated quarterly projections revealing an upward revision to inflation and weaker GDP, and it forecasted that the Bank Rate would remain higher for longer. Inflation is expected to rise by 2.8% in Q1 25 (versus 2.4% in the previous forecast) and increase by 3.0% in Q1 26 (versus 2.6% in the previous forecast), followed by inflation cooling back to the BoE’s 2.0% target in 2027. GDP growth is now expected to grow by 0.4% in Q1 25 (down from 1.4% in the prior forecasts), with economic activity predicted to grow by 1.5% in Q1 26. The BoE also estimates that the Bank Rate will remain around 4.5% in Q1 25 but likely fall to 4.2% in Q1 26, against previous forecasts for 3.7%. Markets are currently pricing another 57 bps worth of cuts this year (little more than two rate cuts).

UK employment and inflation data eyed

UK employment numbers will be released tomorrow at 7:00 am GMT and are expected to show unemployment ticked higher to 4.5% between October to December 2024, up from 4.4% in November. In terms of wages, both regular pay and pay that includes bonuses are forecast to increase by 5.9% on a year-on-year basis (YY), up from 5.6%. However, while market participants will widely watch the jobs report, which can prove market moving, it is essential to remember the validity of the survey’s data remains in question.

Wednesday welcomes the January CPI inflation data at 7:00 am GMT, which is expected to reveal increasing price pressures across key measures. Headline YY CPI inflation is forecast to increase by 2.8% (from December’s reading of 2.5% [2024]), consistent with the BoE’s updated forecasts. The current estimate range is between a high of 2.9% and a low of 2.4%. YY core CPI inflation – excluding volatile food, energy, alcohol, and tobacco items – is estimated to have increased by 3.7%, up from 3.2% in December (estimate range between 3.8% and 3.3%). Regarding services inflation, the YY print is anticipated to rise by nearly a whole percentage point to 5.2%, compared to December’s reading of 4.4%. A rise in price pressures, particularly data that meets or exceeds upper estimates, could prompt investors to pare back rate-cut bets this year. This also places the central bank in a somewhat difficult position, given that it not only reduced the Bank Rate last week, but two MPC members also voted for an outsized 50 bp reduction.

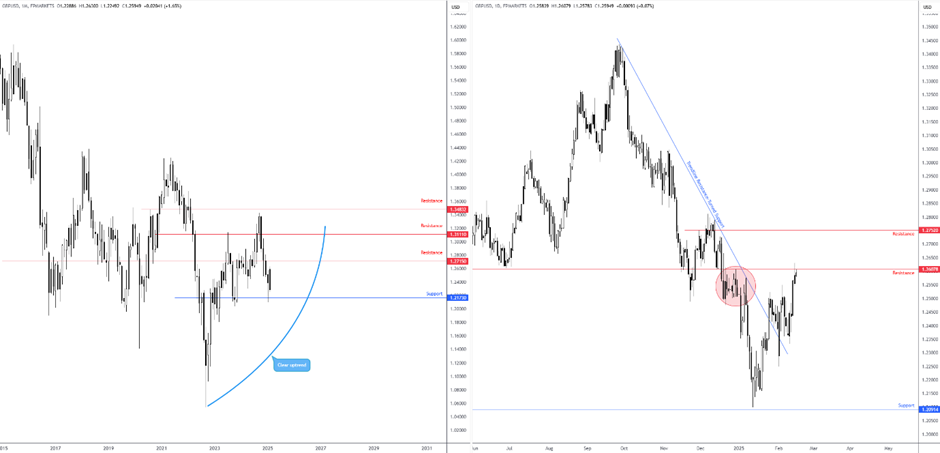

GBP/USD: Monthly bullish engulfing formation?

The monthly chart shows price is on the verge of pencilling in a bullish engulfing pattern from support at US$1.2173 (textbook engulfing patterns focus on the real bodies, not the upper and lower shadows). Monthly resistance demands attention overhead at US$1.2715, with a break of this barrier likely paving the way north for further outperformance towards another layer of monthly resistance coming in at US$1.3111.

Interestingly, buyers and sellers are squaring off at resistance from US$1.2608 on the daily timeframe. The supply area directly to the left of current price (red area) was weak (as noted in a previous piece I posted), with technical buying gathering steam from retesting trendline resistance-turned-support, extended from the high of US$1.3428.

If inflation comes in broadly higher than expected, this will likely underpin a bid in the GBP/USD (British pound versus the US dollar) and perhaps pull the currency pair beyond current daily resistance towards the monthly resistance mentioned above at US$1.2715, closely shadowed by another layer of daily resistance at US$1.2752.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,