To pivot from pause – Asian central banks are ready to cut

Summary

With the Federal Reserve signaling the start of an easing cycle in September, U.S. Treasury yields have fallen and the U.S. dollar has displayed modest weakness. The combination of lower interest rates and dollar depreciation is likely to create policy space for foreign central banks to ease monetary policy more aggressively, or more notably, initiate easing cycles of their own. In our view, emerging Asia central banks are likely to be the institutions most sensitive to recent moves in financial markets, and our monetary policy space framework confirms regional central banks indeed now have more room to lower interest rates. In that sense, we believe Asian central banks are now likely to make a concerted effort toward easier monetary policy, and central banks in Indonesia, Thailand and India can begin cutting rates. At the same time, the People's Bank of China and Central Bank of the Philippines are likely to remain committed to easier monetary policy going forward. Regional central banks may be cutting rates at different speeds, but thematically, the region once absent from the global easing trend is now set to join peer institutions.

Emerging Asia central banks have approached the pivot

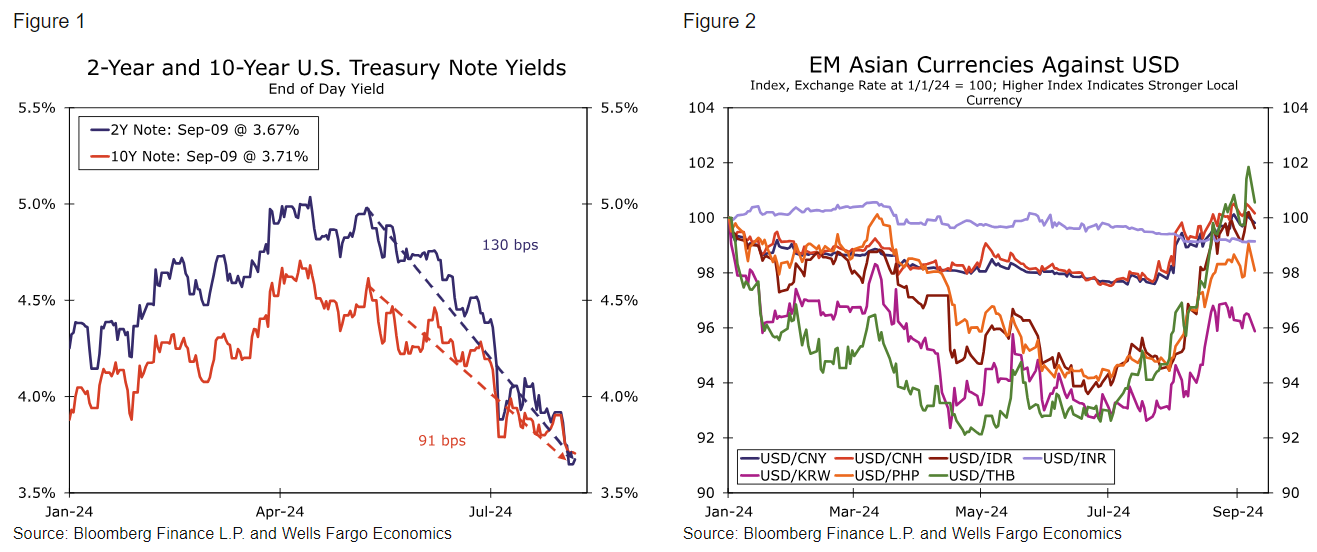

Our August International Economic Outlook contained a section dedicated to the potential spillovers from the Federal Reserve approaching interest rate cuts. We defined “spillovers” as foreign central banks that could be more inclined to either pick up the pace of interest rate cuts or be influenced to start a respective easing cycle now that the Fed is committed to easing. In that publication, we shared our view that most G10 central banks would likely not be influenced by the Fed and would respond to the evolution of domestic economic conditions when considering adjustments to monetary policy settings. However, we did highlight how select institutions in the emerging markets—in particular emerging Asia—could use the Fed's pivot as a catalyst to also lower their own respective policy rates. Policymakers at developing Asia central banks have largely been absent from the easing trend that has taken place in other emerging regions so far. Communications from policymakers often cited upside risks to the local inflation outlook due to potential commodity price shocks and pass through to consumer prices via currency depreciation. While those risks could certainly materialize, regional central bank statements were largely interpreted as policymakers also waiting for the Federal Reserve to start its easing cycle. With the Federal Reserve now all but committed to starting a period of rate cuts in September, U.S. Treasury yields have fallen quickly (Figure 1) and the U.S. dollar has weakened against most Asian currencies (Figure 2). The combination of lower U.S. yields and stronger regional currencies suggests local institutions may now have rationale to either continue easing monetary policy (i.e. People's Bank of China and Central Bank of the Philippines) or more notably, initiate easing cycles.

Author

Wells Fargo Research Team

Wells Fargo