Think ahead: The oohs and ahhs of this week’s electoral and fiscal fireworks

Remember, remember the fifth of November: it’s a rhyme every British person knows as the UK marks Bonfire Night. And who’s going to forget this one? James Smith doesn’t need fireworks - bless him - when he’s got his Bloomberg Terminal and can watch the oohs and ahhs of the US election saga unfold before his eyes…

Think ahead: Electoral explosions and fiscal fireworks

How hard can I hammer the fireworks analogy this week, given that it's Guy Fawkes night and Trump Harris night at the same time on Tuesday? Actually, I'm going to leave it to others, but this is undoubtedly one of the biggest weeks of the year so far. Of course, it could be ages before we know the final result of the US presidential elections.

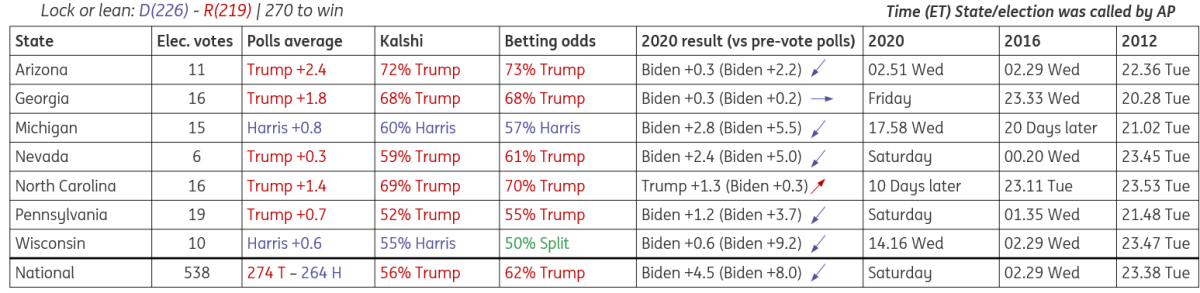

The swing-state polls give Donald Trump a slight edge, but it’s all within the margin of error as Francesco Pesole's excellent cheat-sheet below shows. Turnout will be key. And the polls have been wrong before.

Chatting to our US expert James Knightley, a clear-cut victory for either candidate could easily see the result announced on election day itself or within hours of it. But as he says, if the result isn’t easily determinable from in-person votes, then we’ll have to wait on the mail-in ballots, which inevitably take longer to tally up. Most swing states don’t start counting those until election day, and this method of voting is more widespread than in years gone by.

Add in the potential for recounts in the crucial swing states and maybe some legal delays, and it’s easy to see how it could take several days or weeks for us to get a clear sense of what’s happened. It took four days for the networks to confirm Biden as President back in 2020.

The 2024 US swing states cheat sheet

Source: Five thirty eight (ABC News), Kalshi.com, Betfair, CNN, AP, ING (Francesco Pesole)

Remember that financial markets have begun pricing a Trump victory in recent weeks. The possibility of extended and/or expanded tax cuts, coupled with tariffs, is widely assumed to mean a stronger dollar and higher yields. If there’s a period of time without a clear result, then our strategists reckon some of that Trump positioning could start to unwind as the chances of a Harris victory are reassessed.

That’s before considering the risk of lengthy delays in the closely run Senate races. Don’t forget that the market reaction could look very different if we get a split Congress.

You've got to feel for the Fed high honchos. Officials would be forgiven for wanting to keep a low profile next week, but they'll be in the spotlight on Thursday with their rate decision. And recent data means it’s hard to see them doing anything other than a 25 basis point rate cut, anyway. Hurricanes and strikes mean Fed officials will take October's shockingly low jobs growth with a bucketful of salt.

The Bank of England meets next week, too, but let’s face it, they’ve got bigger problems closer to home. Government bond yields, or gilts, have risen a fair bit since Wednesday’s budget unveiled big tax hikes and even bigger spending rises. This isn’t anything like that turmoil after the infamous 2022 mini-budget. However, markets have concluded that Labour’s first budget will curtail the BoE’s easing cycle.

We’re far less convinced. This may look like a big fiscal stimulus, but only if you compare it to the March budget’s tax and spending plans, which were widely seen as undeliverable, irrespective of who won July’s election.

Day-to-day spending would always have needed to rise, even if what was announced still eclipsed most people’s expectations. And steep tax rises make the medium-term economic impact of higher spending less clear-cut. That’s the conclusion we expect the BoE to reach, too, and a 25bp cut is still overwhelmingly the base case on Thursday.

I don't need to tell you that next week will be the most pivotal of the year so far. So sit back, light a sparkler, toast some marshmallows, load up a chart of 10-year Treasury yields, and enjoy the show.

Think ahead in developed markets

United States (James Knightley)

Election (Tue): Next week’s election will be huge for the outlook for the US economy. While opinion polls suggest the election will be an incredibly close vote, financial markets have appeared increasingly confident of a Trump victory with equity markets the dollar and Treasury yields all rising in recent weeks. If Trump wins these trends may continue, but could sharply reverse under a Harris victory.

In general, we argue that a Trump victory will ensure a lower tax environment that should boost sentiment and spending in the near term. However, promised tariffs, immigration controls and higher borrowing costs will increasingly become headwinds through his presidential term. Conversely, a Harris victory implies continuity, but with Congress likely split, her ability to deliver her manifesto is questionable. Slightly higher taxes and only modest increase in spending may be seen as the best election outcome possible by the Treasury market, but it puts more pressure on the Fed to deliver rate cuts and support growth.

Federal Reserve (Thu): With regards to the Fed, we expect a 25bp rate cut on Thursday, irrespective of the election outcome. The Fed is more relaxed about inflation and is putting more focus on the jobs market as it attempts to secure a soft landing for the economy. Even after September’s 50bp rate cut monetary policy is in restrictive territory and the Fed has scope to keep cutting rates back to a more neutral level to give the economy a little more breathing space to continue growing strongly.

United Kingdom (James Smith)

Bank of England (Thu): A 25bp rate cut is highly likely, but investors are much more interested in what officials say about October's budget. The Office for Budget Responsibility reckons it will lift GDP and inflation next year, but we suspect it won't as significantly alter the BoE's view. The fact that services inflation has undershot the BoE's August forecasts is arguably more important. Still, in a potentially volatile week for markets, the BoE won't want to rock the boat and remember, officials so rarely comment on market pricing anyway. Expect the Bank to reiterate that further gradual cuts are likely. The next couple of inflation releases will determine whether we're right with our call that the BoE will cut rates again in December.

Sweden (James Smith)

Riksbank (Thu): Back in September, Sweden's central bank opened the door to a 50 basis-point rate rate cut before year-end. It looks like that's what we'll get on Thursday. Just like the ECB, the Riksbank is more heavily focused on Sweden's ever-weaker activity data. The only risk is if the US election generates a sharply weaker Krona, though the central bank seems less fazed by the threat of FX depreciation than it was a few months ago.

Think ahead for Central and Eastern Europe

Poland (Adam Antoniak)

NBP rate (Wed): The MPC is expected to keep the main policy rate unchanged at 5.75%, with headline inflation not projected to peak until March 2025. The November staff projection will likely point to a decline in CPI inflation in 2H25, but given the uncertainty surrounding key assumptions (e.g. the electricity price cap), policymakers are unlikely to put much weight on those forecasts. Those projections will also point to persistently elevated core inflation We think that the March projection will show a clearer picture of the inflation outlook and the MPC will deliver the first 25bp rate cut in 2Q25.

Hungary (Peter Virovacz)

Retail & Industry (Wed/Thu): As we've already seen the nightmarishly bad Q3 GDP data, we don't expect any positive news from Hungary's September retail sales and industrial production data. We expect both sectors to show a significant month-on-month decline, with year-on-year indices falling. The lack of external demand and the high degree of consumer caution is taking its toll.

Romania (Valentin Tataru)

Interest rate (Fri): The National Bank of Romania (NBR) is expected to hold the policy rate unchanged at 6.50%, likely citing a higher-than-expected inflation path versus its previous projections. Additionally, we think that fiscal slippage, coupled with strong credit activity and high wage growth, are likely to add more weight to medium-term monetary policy considerations, essentially supporting a more prudent policy response.

Czech Republic (David Havrlant)

Czech industrial malaise might be past its worst and we expect stronger output in September relative to the previous year. Such a long-awaited turnaround is essential if the Czech recovery is to gain pace. Still, lukewarm external demand is a drag, making it harder to achieve a full industrial recovery. Meanwhile, households likely continued to splash the cash, taking real retail sales to lofty heights, confirming the shoppers are the main engine of economic expansion. That said, the economy is still operating well below its potential, so we see another 25bp rate cut as the most likely outcome for next week’s CNB meeting. Continued employee dismissals within industry are likely to offset the positive seasonal effect we usually see in the employment rate during October.

Turkey (Muhammet Mercan)

Inflation (Mon): The combination of the central bank's disinflation strategy, which relies on the exchange rate and supportive base effects, has driven a downtrend in headline inflation since June. However the pace of decline has been slower because of inertia in services inflation. Given the absence of a more rapid improvement, the CBT seems to have slowed TRY depreciation recently. Given this backdrop, we expect October inflation at 2.4% MoM, leading to a further decline in the annual figure to 47.9% from 49.4% a month ago.

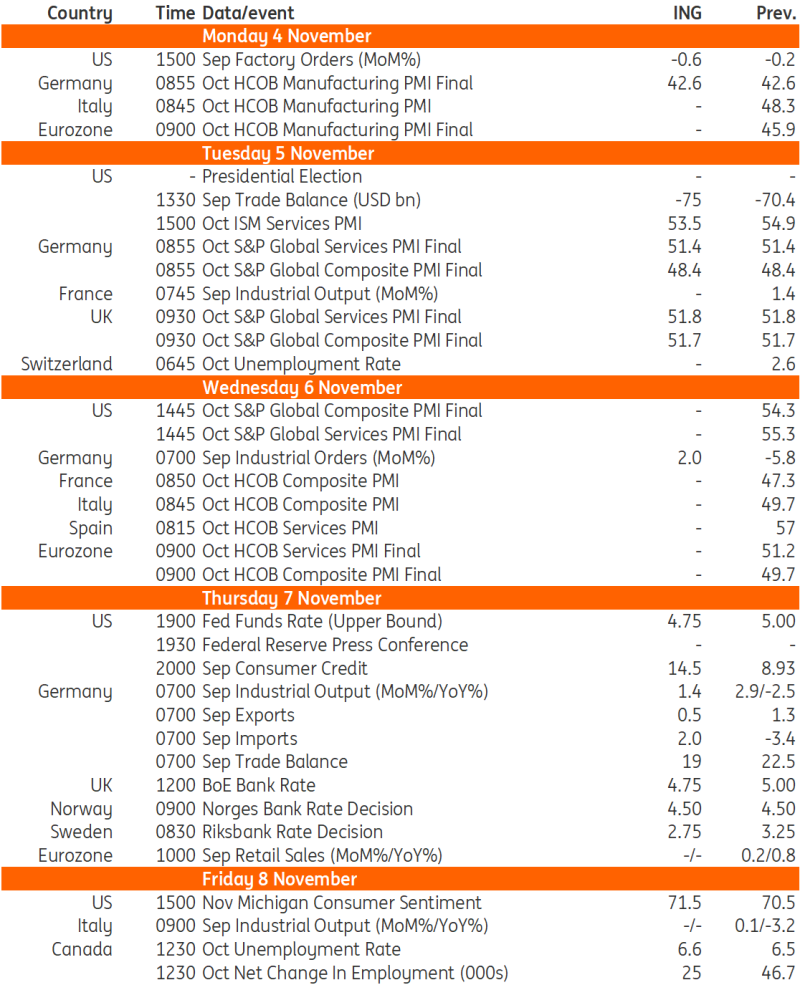

Key events in developed markets next week

Read the original analysis: Think ahead: The oohs and ahhs of this week’s electoral and fiscal fireworks

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.