Think ahead: Jobs data in focus

The consensus is for US non-farm payrolls to have risen 153k in December while the unemployment rate is expected to hold at 4.2%. This would be consistent with a general cooling of the jobs market. Data from Hungary and the Czech Republic, meanwhile, may show unemployment ticking up

Think ahead in developed markets

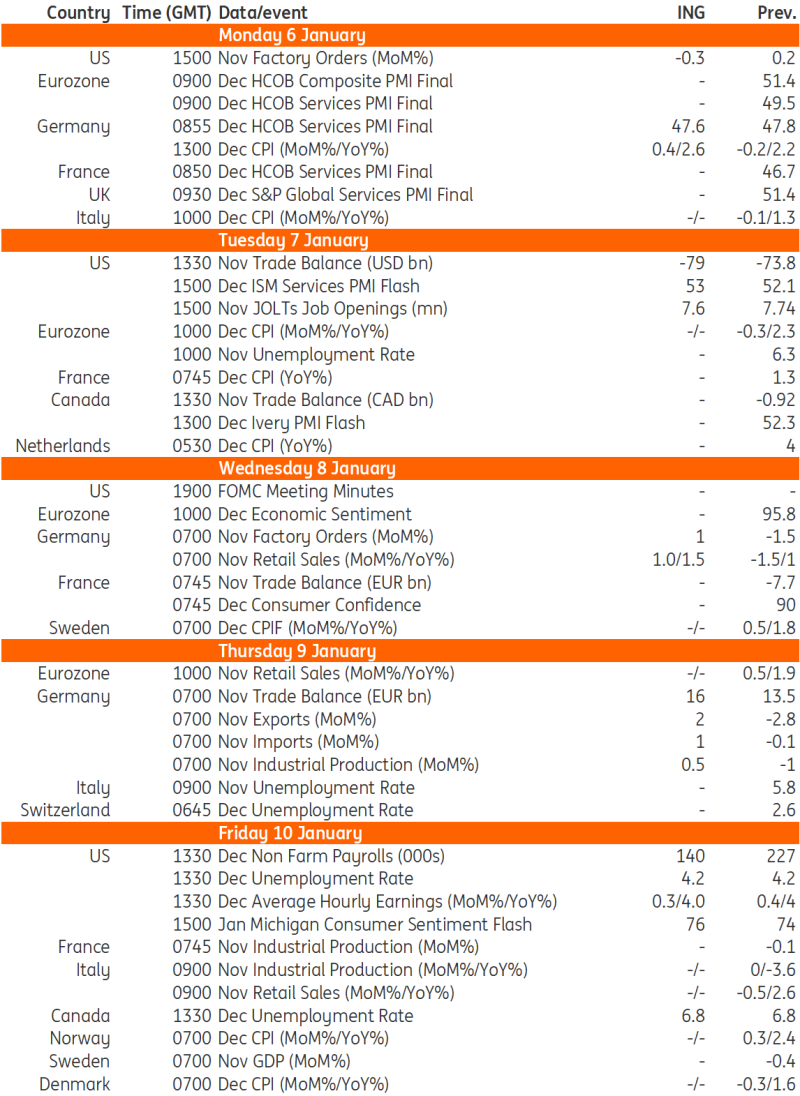

The first jobs report of the year comes next Friday (January 10). The early consensus is for December non-farm payrolls to have risen 153k with a range of 125k to 200k, but expectations will be firmed up through the week with the release of job openings numbers, ADP private payrolls and the ISM employment components. The unemployment rate is expected to hold at 4.2%, while wage growth is expected to hold at 4% year-on-year. This would all be consistent with the general cooling of the jobs market, but after 100bp of Fed rate cuts in 2024, the widely held view is that we will see a much slower and less aggressive series of moves in 2025.

The Federal Reserve dot plot update from the December FOMC meeting suggested the central forecast amongst officials is for only two 25bp cuts in 2025. Just 3bp is priced for the 29 January FOMC meeting with 15bp priced by March. We certainly agree with a no-change outcome later this month but are still projecting a 25bp cut in March. While the Fed has been cutting the policy rate, longer-dated borrowing costs have surged higher on a combination of government debt sustainability concerns and potentially sticky inflation. The dramatic steepening of the yield curve is pushing mortgage rates and corporate borrowing costs sharply higher. The dollar has also risen to its strongest level in more than two years against key trading partners and these two factors will act as a brake on economic activity that the Fed may feel it needs to offset.

Think ahead for central and Eastern Europe

Hungary

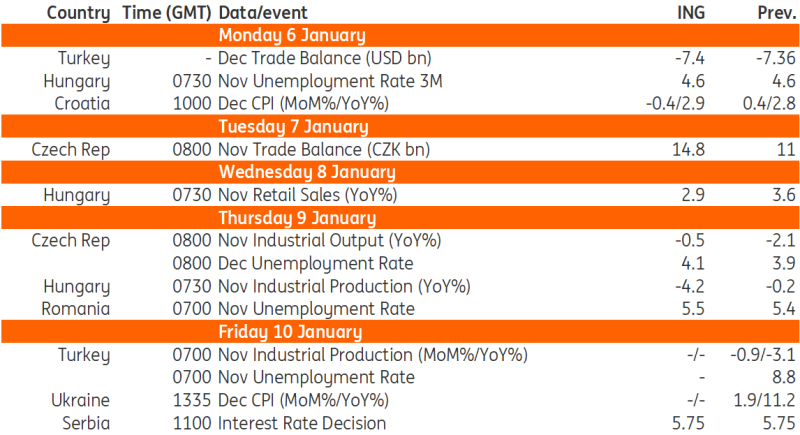

Unemployment (Mon): We see a slightly higher, but still stable, official unemployment rate. The 4.6% rate continues to look favourable amid a still-high level of labour hoarding (around 17%). So far, so good, but should we see a further deterioration in the economic outlook, this could trigger significant layoffs.

Economic activity: The November economic data is due in early January and we see a rather downbeat collection of data prints. After the surprisingly strong October figures, we expect some corrections and see declines in both retail sales and industrial production on a monthly basis. However, we still believe that the big picture will show just enough improvement for Hungary to emerge from a technical recession in the fourth quarter.

Czech Republic

Production (Thu): The annual decline in industrial output softened in November, with Czech industry likely hitting the bottom. That said, the industrial outlook remains foggy, as the European and, in particular, the German economic performance remains under pressure. Still, the levelling off in Czech industry has contributed to a somewhat improved trade balance in the same month.

Unemployment (Thu): The unemployment rate likely picked up in December, mostly due to the usual seasonal effect. Meanwhile, the labour market remains tight, with the rebound in the construction sector set to drive hiring in the spring.

Key events in developed markets next week

Source: Refinitiv, ING

Key events in EMEA next week

Source: Refinitiv, ING

Read the original analysis: Think ahead: Jobs data in focus

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.