The weekender: US exceptionalism

This week, US equity markets showcased a meaningful surge, with the S&P 500 advancing 1.7%, fueled by robust performances from industrials and small caps. These sectors, emboldened by the promise of a favorable business climate and potentially lighter regulations anticipated under Trump's forthcoming administration, led the market's charge.

However, the technology sector didn't share in the week's overall gains, with tech stocks typically known for driving index growth faltering. Notably, the information technology sector trailed significantly, marking it as Friday's least successful performer within the S&P 500. The tech landscape was awash in drama: Nvidia's recent earnings have left investors pondering the sustainability of AI's influence on market dynamics.

Further intensifying the tech sector's tumult, the "Magnificent Seven" tech megacaps navigated choppy waters stirred by regulatory uncertainties. Alphabet, in particular, faces a looming threat of a potential breakup, with the U.S. Department of Justice suggesting drastic remedies like divesting Google's Chrome browser and altering its default setting agreements—a move that could dramatically reshape the tech giant's future.

Despite these tech tremors, the broader market sentiment remained strikingly optimistic, capturing a spirit of revival and buoyancy across Wall Street. This week’s market dynamics paint a vivid picture of a landscape punctuated by both challenges and resilience, underscored by strategic shifts in anticipation of a new economic era.

According to the latest EPFR update, US-focused equity ETFs and mutual funds have been on a spectacular run, with inflows reaching an astronomical $448 billion. this year. By region, US stocks marked their seventh consecutive week of inflows with $16.4 billion. In contrast, emerging market equities saw their sixth week of outflows, totaling $1.8 billion, while Europe continued its losing streak with $3.6 billion in outflows, its eighth consecutive week.

As US markets continue to thrive, there's a stark contrast with the broader global investment scene. The once-celebrated "China can't miss" strategy, initially seen as a guaranteed win amid stimulus-driven growth, has now faltered. What was once heralded as a strategic masterpiece has degraded into what many see as speculative excess, often criticized as a pump-and-dump scheme. Similarly, European markets are struggling to match the economic vibrancy of their American counterparts, lagging behind without the necessary underlying economic momentum to propel them forward. This divergence highlights a clear split in the dynamism and potential between the booming U.S. financial landscape and its global peers, which are wrestling with their own economic challenges.

Adding to the complexity is the precarious position of both China and Europe, teetering on the brink of what could be a prolonged period of economic stagnation. This looming threat could be exacerbated if President Trump’s proposed tariffs come into effect, potentially compounding these economies' challenges.

This global divergence underscores investors' marked preference for US financial markets' dynamic resilience and growth potential around the “ US exceptionalism” narrative . As they navigate the intricate dance of international finance, investors are particularly keen on exploiting the promising opportunities the US markets continue to offer.

In parallel, Bitcoin dazzled, flirting with the elusive $100K mark, capturing the imagination of investors and speculators alike.

State side , economic vitality pulsed stronger, with November's S&P purchasing managers' indexes marking the most rapid expansion since April 2022, especially pronounced in the services sector.

Across the ocean, Europe presented a starkly different economic tableau. PMI surveys painted a picture of contraction and added credence to ECB President Christine Lagarde's cautions about escalating trade threats within the EU.

The dollar ascended to a near two-year zenith, thriving on the sell-off in the euro and British pound, while European government bonds rallied amidst the currency turmoil.

Treasury secretary

President elect Donald Trump has tapped Scott Bessent, a prominent hedge-fund manager and a staunch advocate of Trump's economic strategies, to head the Treasury Department. Recently rising as a pivotal economic adviser, Bessent has been a vocal defender of Trump’s economic initiatives, especially in circles of Wall Street skeptics concerned about potential trade wars and price hikes for American consumers stemming from Trump's tariff plans.

Pending Senate confirmation, Bessent's role will be crucial in transforming Trump’s campaign promises into actionable policies. He will play a key role in deciding how the president-elect’s boldest economic proposals, from abolishing taxes on tips to implementing broad tariffs on U.S. imports, will be executed. This appointment positions Bessent at the heart of the incoming administration's economic agenda, tasked with steering the U.S. economy through potentially transformative changes.

The appointment of Scott Bessent as Treasury Secretary has seemingly positioned Kevin Warsh, who was also a contender for the Treasury role, as the likely successor for the Federal Reserve Chairmanship when Jerome Powell's term concludes in 2026. This strategic placement hints at a future where Warsh could lead the Federal Reserve, shaping monetary policy at a critical juncture for the U.S. economy.

Silly season

Welcome to the annual "silly season" in financial markets, where investment houses unveil their grand predictions for the upcoming year, and I can't help but chuckle at their audacity. These forecasts are destined for countless revisions—indeed, firms are still tweaking their 2024 predictions as we speak.

Diving into the deluge of 2025 bank analyses flooding my inbox, it's apparent that expectations for the S&P 500 swing wildly, with estimates ranging from a bullish 7500 to a bearish 4500.

This leaves us sailing a vast ocean of boundless optimism and guarded pessimism, a vivid reminder of why these annual forecasts should be taken with a hearty grain of salt. The market rarely dances to the tune of neatly scripted projections.

My gaze for the coming year is intently focused on the Equity Risk Premium, under the looming shadow of rising 10-year bond yields that could soar to 5%, propelled not by any Trumpian economic wizardry but by the grim specter of escalating inflation.

The true terror for the markets lies in how swiftly these yields rise. A gradual increase might herald robust economic growth, but abrupt, inflation-driven spikes could ravage the equity landscape. A sudden surge in bond yields, particularly one that strays significantly in a brief span, could shatter the market’s current robustness.

But if If Michael Hartnett, known as Mr. 'Flow Show and a perennial bear,' is on the mark with his forecast that the S&P 500 is poised for "another big double-digit move" in 2025 due to falling bond yields—the "secret sauce" for continued equity gains and staving off drastic downturns—then rest assured, we'll be strategically positioned to capitalize on that movement as well.

Currently, the market may seem invincible, a bastion of strength, but this façade is at risk of fracturing under the strain of rapid inflationary pressures. When reality strikes, anticipate a harsh and swift correction that could relegate perceived market stability to just a fleeting episode in the annals of financial history.

Amidst this, we are also witnessing a high-stakes ballet between stock valuations and bond yields, reminiscent of a classic financial drama. Time-honored wisdom tells us that while rising bond yields might beckon with the allure of higher returns, especially in an environment with no rate cuts, they can dim the luster of overpriced stocks.

Furthermore, the brewing tech conflict threatens to deepen supply chain troubles well into the next year, escalating typical trade tensions to an intensity that could rival historical confrontations. This intricate scenario is poised to dramatically reshape market dynamics and economic strategies.

Despite the market's unpredictable tides over the next six months to a year, where abrupt changes could tip any short-term strategy, my long-range outlook remains resolutely bullish. This isn't merely about navigating the immediate waves—it's about charting a course toward distant horizons, always prepared to harness the transformative currents of change for enduring prosperity.

As a trader, navigating this dichotomy—balancing the need for short-term accuracy in trading with long-term investment strategies for familial stability( A mix of SPY EFT, gold,bonds and property) —requires a keen separation of immediate financial exigencies from generational wealth goals. In the trading arena, where keeping the lights on is paramount, there's no room for unwavering bullish or bearish stances; success hinges on making more right calls than wrong over the short term. Why to I think short term is the better way to go? ‘The long run is a misleading guide to current affairs. In the long run we are all dead,’ wrote John Maynard Keynes in his 1923 work, A Tract on Monetary Reform.

Nusse und bots

Straying away from my usual NUTS & BOLTS focus on US economy, this weekend is all about Europe.

Europe is currently ensnared in a whirlwind of crises that extend from its energy corridors to its financial markets. As the conflict in Ukraine intensifies, showcasing the grim new reality of ICBM deployments, the ripple effects are causing significant logistical nightmares for shipping across the strategic Black and Red Seas. Adding to the turbulence, the energy sector reels under pressure as LNG prices spike to a one-year high amidst a contentious dispute between Russia’s Gazprom and Austria, which threatens further disruptions. With the critical gas transit deal set to expire by the end of 2024, Europe braces for a potentially icy winter of uncertainty.

The economic landscape, particularly in Germany, once the bastion of European industrial prowess, is showing cracks. The powerhouse has been battered by soaring energy costs in 2022, a tepid shift towards electric vehicles, and heavy reliance on Chinese imports amid rising trade tensions. This perfect storm has hit Volkswagen hard, forcing Germany’s industrial giant to contemplate unprecedented factory shutdowns and massive layoffs, signaling a seismic shift in the country's manufacturing sector. This crisis is cascading through the auto supply chain, with firms like Schaeffler AG downsizing and shedding jobs across Europe.

The tech sector isn't immune either. Ambitious plans to cement Europe’s position in the semiconductor race are faltering, with major players like Intel and Wolfspeed halting their German expansion plans, casting shadows over the EU’s goal to command a significant share of the global semiconductor market by 2030.

In this backdrop of industrial and economic turmoil, long-term strategic frameworks like Mario Draghi’s “The Future of European Competitiveness” appear more like wishful thinking. Immediate economic indicators are grim, with the Euro Area's composite PMI plunging to a 10-month low, signaling a contraction that’s pulling Germany down with it.

Politically, Germany is at a crossroads, distracted by upcoming confidence votes and potential elections. Yet, there’s a silver lining as political discourse suggests potential flexibility in the stringent debt brake rules, offering a ray of hope for fiscal maneuverability.

Amid these tumultuous times, Europe stands at a critical juncture, challenged to navigate through immediate crises while steering towards a sustainable economic revival. The continent’s ability to adapt and innovate under pressure will undoubtedly shape its path forward in an increasingly unpredictable global landscape.

Chart of the week

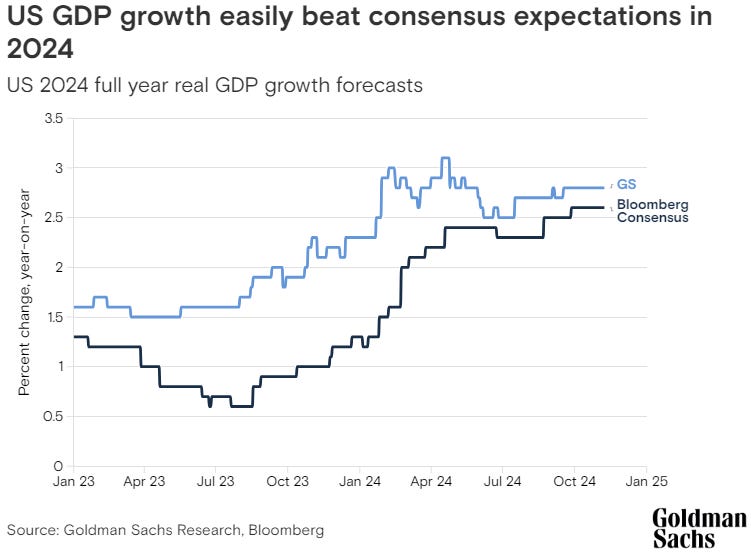

US GDP is forecast to outperform expectations in 2025

The U.S. economy is poised for a stronger performance than many analysts predict, according to Goldman Sachs Research. They project that U.S. GDP will grow by 2.5% in 2025, outpacing the Bloomberg-surveyed economists' consensus of a 1.9% expansion.

David Mericle, Goldman Sachs' chief U.S. economist, highlighted this in the firm's "2025 US Economic Outlook: New Policies, Similar Path" report. According to Mericle, the factors bolstering this outlook include diminished recession fears, inflation returning towards the 2% target, and a robust yet rebalanced labor market.

Following the recent Republican victories in Washington, three significant policy shifts are expected to influence economic dynamics:

-

Tariff Adjustments: Proposed increases on imports from China and autos could elevate the effective tariff rate by 3 to 4 percentage points, potentially impacting trade dynamics and prices.

-

Immigration Policy Tightening: Policies may reduce net immigration to 750,000 per year, slightly below the pre-pandemic average of one million, which could influence labor market conditions.

-

Tax Policy Continuation: The extension of the 2017 tax cuts, which were set to expire, alongside modest new tax reductions, could stimulate economic activity.

Despite these anticipated policy changes, Mericle believes they will not drastically shift the economy's or monetary policy's course. Goldman Sachs Research expects the Federal Reserve to continue reducing the federal funds rate to a terminal range of 3.25-3.5%, down from the current 4.5-4.75%. This forecast suggests a cautiously optimistic scenario where policy adjustments support sustained economic growth without necessitating drastic shifts in monetary strategies.

Running update

Ahead of this mornings local "unofficial" half marathon at Somdet Phra Srinakarin Park, my week was supposed to be light, but a minor bout of Thailand Tummy threw a wrench in the works—even after five years here, it still catches me off guard. Thankfully, I recovered quickly in time to tackle my first intense "house of pain" run in months. Aerobically, I'm in top form, but I'm just beginning the grind of building up my skeletal and muscle endurance for long runs, so jumping back into a substantial long run after six months was quite challenging.

Adding to the pain, I switched to a low-carb runner's diet three days ago, which meant I had to forego my usual boost juice gels packed with sugar. Those gels are counterproductive when you're trying to shift your body’s energy source from carbs to ketones ( fat) . Despite these hurdles, I recently hit my one-year endurance peak, although I anticipate I might lose some ground over the coming weeks. My training focus is shifting: from 7 km threshold runs to a regimen that includes thrice-weekly 10-12 km runs at zone 2, a weekly recovery run, and a long run between 16-20 km every Saturday.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.