The week ahead: US election and central bank meetings to test investor stamina

There is a formidable amount of event risk coming up for markets in the next few days, which will test the stamina of investors. The US election, economic data, earnings and two key central bank meetings. So, let’s jump into what to look for, and what this means for markets.

The US election:

It looks like it will be a photo finish for this election. The RealClearPolitics poll average puts Kamala Harris ahead with 48.5% of the vote, while Donald Trump has 48.3%. The most recent New York Times/ Siena Survey shows that Harris is ahead in 5 of the 7 key swing states, however, her lead is still within the margin for error. Arizona is clearly leaning towards a Trump victory in this late stage of the campaign, while Wisconsin, Nevada and North Carolina look like they will swing to Harris. In Pennsylvania, the ‘tipping point state’, the polls for both candidates are neck and neck.

The final rallies for both candidates were held in the key battleground states over the weekend. Some political commentators noted a shift in tone from Donald Trump, with some suggesting that he could be gearing up to contest the election. Global stock markets sold off last week, and the S&P 500 finished lower by more than 1%, although they rose on Friday. The main US blue chip index is up 20% YTD, which does not suggest that the market is seriously pricing in the risk of civic violence after this election, which could rock financial markets and cause a global wave of risk aversion.

The risk of civic unrest

Aside from who wins, there are other key risks from this election result:

-

A delay to the results due to a tight race. Some political analysts fear that it could take up to two weeks to get the final result.

-

A delay in the result due to contested results, with legal challenges from both candidates possible, that could complicate the outcome of this election.

-

Civic unrest.

The Vix index, which measures volatility for the S&P 500, has been trending higher in recent months. It is above the 12-month average of 15.16, and is currently trading around 21.8. However, this index could soar if there is civic unrest or a protracted period where we do not know the outcome of this election. The longer it takes to declare a winner, the harder it is to assess what will drive markets and how asset prices will react.

Congressional race results are key for markets

It is not just the Presidential race that we need to prepare for. In the long term, the outcome of the Congressional elections will be more important for financial markets as they will determine policy. All seats in the House are up for re-election, and a third of Senate seats. From a bond market perspective, the biggest risk is a clean sweep for the Republicans, as it could lead to higher inflation and a major sell off in US and global bonds, pushing yields even higher.

The Congressional race is also too close to call at this late stage; however, it is worth noting that financial markets would prefer a divided White House and Congress, and a divided House and Senate. This is because it could lead to calmer markets as it limits the chances of major policy change.

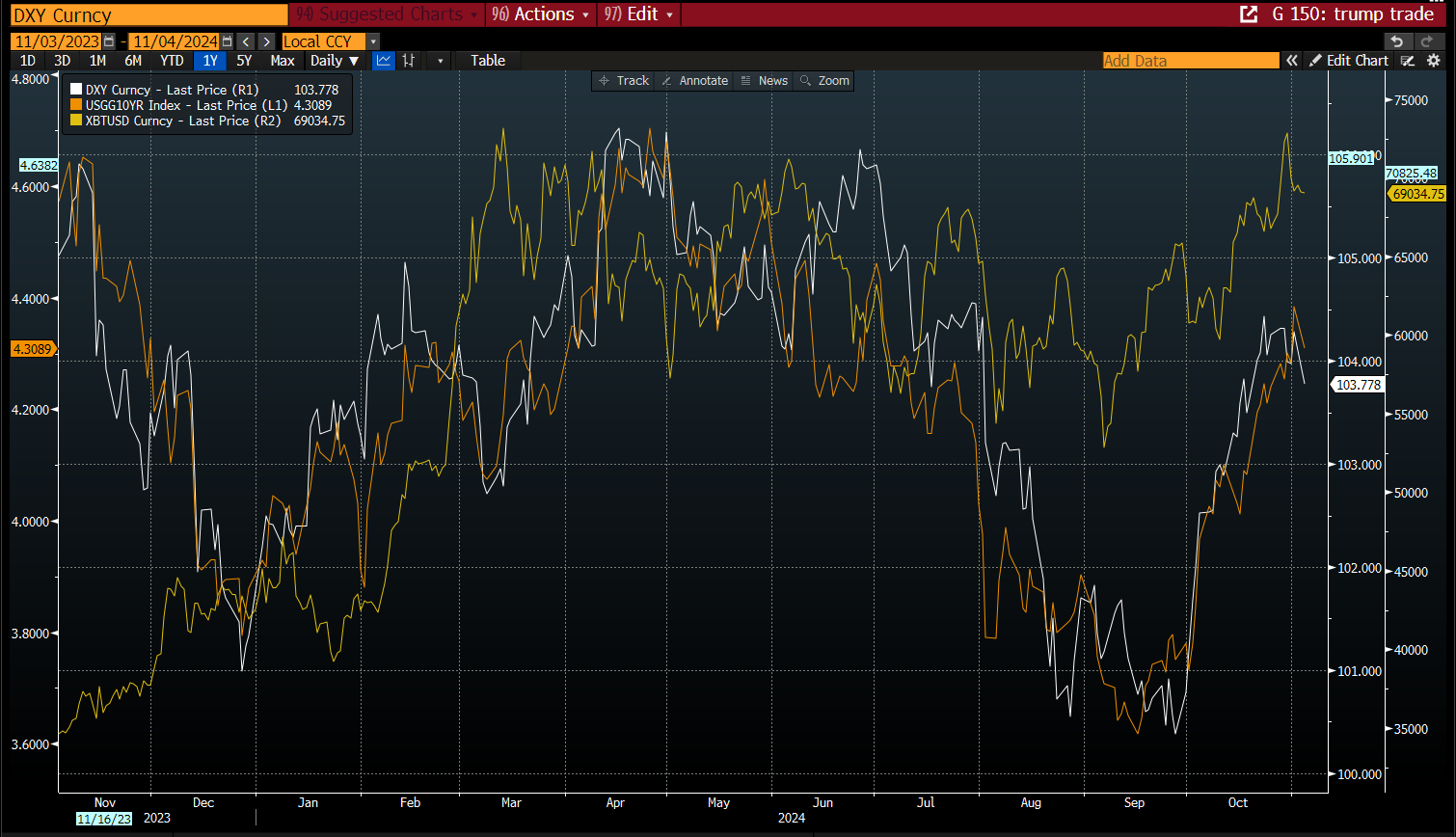

Harris win could unravel the Trump trade

An interesting development leading up to this election is that financial markets expect Trump to win, and the Trump trade has performed well in recent weeks, as you can see in the chart below. The Trump trade is a stronger dollar, weaker bonds/ higher bond yields and stronger crypto. With one day left of this campaign, the dollar is falling, and the dollar index is at a 2-week low. Thus, if Harris does win on Tuesday we could see a rapid unwinding of this trade, a sharp weakening of the dollar and intense volatility in the FX and bond market.

The Trump trade

Source: XTB and Bloomberg

If Trump wins the election and gets a second term of being president, the impact on the dollar could depend on the outcome of the Congressional elections. A Trump Presidency and a Republican Congress could lead to a surge in the dollar and a sharp sell off in EM currencies, the euro and the pound, as markets rush to price in the effects of new tariffs, trade and foreign policies for the US.

It's now a waiting game until the election event of the year. We expect Monday and Tuesday to be quiet for markets, however, once we get the first drip feed of results on Tuesday night and Wednesday morning, expect fireworks.

FOMC meeting: Less suspense as rate cut fully expected

At the last FOMC meeting in September, we were all on tenterhooks waiting to see if the FOMC would cut interest rates by 50bps or 25bps. There is no such surprise element this month. The Fed won’t cut rates by 50bps, instead a 25bp rate cut is on the cards. The CME’s Fedwatch tool is predicting a 98% probability of a 25bp rate cut on Thursday, and we expect the Fed to deliver. The Fed’s rate decision is at 1900 GMT, followed by a press conference with Jerome Powell. There will be no updated Dot Plot or summary of economic projections at this meeting, instead we will have to wait for December for those.

The Fed is expected to say that future rate cuts are necessary as inflation is retreating to the target 2% rate. However, the macroeconomic backdrop to this meeting has been mixed, and the economic data has been volatile. GDP growth was strong in Q3, retail sales are solid and consumer confidence has recovered. However, the labour market is showing signs of strain. Although the 12,000 reading for NFPs last month was mostly down to hurricanes and strikes, there were some details in the household survey of employment that are worrying. The number of long term unemployed is creeping higher, and now stands at 22.9% of all unemployed people. Added to this, business and professional services saw a 49,000 drop in temporary service jobs. This can be a sign of cyclical weakness in white collar jobs, which does not bode well for future labour market growth, even taking account of strikes and hurricanes.

Since the last FOMC meeting, there has been a large recalibration in the market’s expectations for future rate cuts. In September, the market expected more than 175bps of cuts through to December 2025. This has shrunk to less than 125bps of cuts today. Unless the Federal Reserve is super dovish about the prospects for the labour market, we do not expect a return to level of cuts priced in back in September. However, we think that the Fed will remain tight lipped about the future prospect for interest rates. While further rate cuts are expected, the big debate is about the neutral rate, and where US interest rates will settle. This is the next stage in the Fed’s monetary policy debate, although we think they will argue that it is too early to target a specific level for the neutral rate at this meeting.

Although the Fed are apolitical, future economic policy in Washington will shape the direction of Fed policy. Thus, since this meeting is so soon after the US election, and we may not even have a clear winner, it makes future Fed action harder than usual to determine.

BOE: Updated forecasts in focus

The pound is climbing at the start of this week, and GBP/USD is hovering just below $1.30, a level full of option strikes, which increases the chance of a breakout above this level at some point this week. The Bank of England is expected to cut interest rates on Thursday, and there is a near 95% chance of a cut priced in by the market. Last week saw major volatility in the bond market in the aftermath of the Budget. Higher OBR forecasts for UK inflation also triggered a recalibration in interest rate expectations for the UK, with 23 basis points of cuts being priced out by September 2025.

The 10-year UK Gilt yield rose by 26bps last week, although yields backed away from their highs above 4.53% on Friday. The two-year yield rose 30 basis points last week. UK bond yields may have recovered on Friday, however, they were still major underperformers relative to French, German and US yields, as you can see in the chart below. The bond vigilantes have sent a warning shot to the UK government. We think that the £30bn of extra government borrowing each year will lead to a permanent premium being added to UK bond yields on the back of this Budget.

UK bonds underperform their peers, as yields rise

Source: XTB and Bloomberg

The BOE forecasts for growth and CPI that will be included in their Monetary Policy Report, will be scrutinized to see if higher bond yields and the prospect of fewer interest rate cuts will dent the BOE’s growth forecasts, which had been expected to be revised higher. Also, we expect that the Budget will have boosted the BOE CPI forecasts for the long term.

The pound was volatile last week, 1-week volatility for GBP/USD surged from 8% before the Budget to 13% this week. The increase in volatility is also due to US election risks. However, even though the Budget’s cold reception from UK bond investors hurt the pound last week, the future outlook for GBP depends on who wins the US Presidential election. If Trump wins on Tuesday and the Republicans get a a clean sweep, then it could weigh on UK economic prospects, which is pound negative.

The BOE is independent, so we do not expect Andrew Bailey to directly address the detail of the Chancellor’s controversial tax and spend plans. However, it will be interesting to see if the BOE, like the OBR, revise down their medium-term forecasts for UK GDP, as fears about the public sector crowding out the private sector gain traction.

Oil price watch

The oil price is rising at the start of the week, and Brent crude is up by 1.7%. Opec+ announced at the weekend that it would delay its planned production cut for a month. Production was expected to ramp up by 180,000 barrels per day in December, but this will now be delayed until January. This is the second delay, and it suggests that Opec + is trying to shore up the price of oil. Brent crude fell 3.88% last week and is down 8% in the past three months. It is currently trading above $74.00 per barrel, however, the oil price is too low to allow production to ramp up anytime soon. After all, Saudi Arabia has new cities to build, and Russia is waging a costly war with Ukraine. Thus, we could see the proverbial oil production can get kicked down the road for some time to come.

Author

Kathleen Brooks

XTB UK

Kathleen has nearly 15 years’ experience working with some of the leading retail trading and investment companies in the City of London.