The Trade Week Ahead – Why the USD is everything [Video]

![The Trade Week Ahead – Why the USD is everything [Video]](https://editorial.fxstreet.com/images/Markets/Currencies/Majors/DollarIndex/macroeconomics-1775959_XtraLarge.jpg)

I continue to watch these short term spikes in EUR, AUD, GBP and the like and sit there and ask; am I wrong? Is this as good as it gets for the USD? It has rallied hard in 2018 in the main but then I see what was released from the Federal Reserve and look at the forecasts for the non-farm payrolls this week and I remember that my justification for backing in the USD is sound.

Take last week’s Fed outcomes.

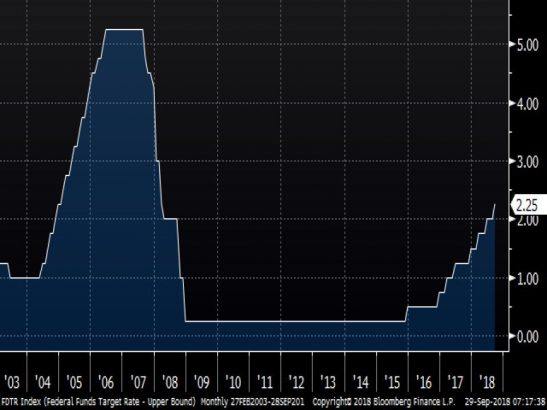

Market reactions were subdued initially as the Fed jacked up the Federal Funds rate for the eighth time in 2.5 years.

There were some moves that suggest the market is finally catching on to the idea the Fed is moving ahead of pricing. US bank securities fell on the prospect of increased funding costs over the coming years, yet UST 10 yields fell 5 bps to 3.05% and the USD moved lower – this is what made me question my longer term view on the USD.

However, that move was made mainly due to the fact ‘accommodative’ was removed from the statement. The suggestion being that this was a dovish change and that the Board could be backing away from its gradual rate rises.

Chairman Powell crushed that idea in his press conference by stating that policy was no longer ‘accommodative’ and that the FOMC’s rate course has not changed and will: ‘gradual(ly) return to the [federal funds rate] to its neutral cash rate’ – USD long term view confirmed.

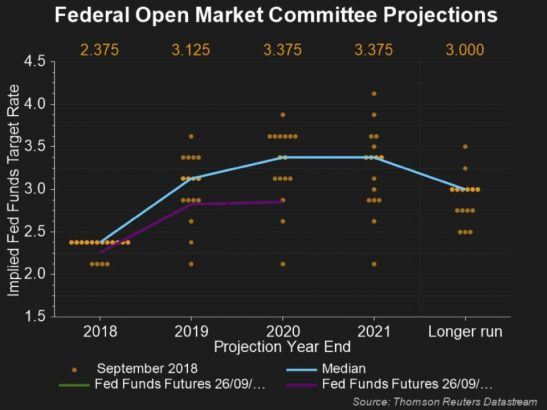

The new dot pots also confirm my USD bias – the Board has a consensus for the December meeting – meaning come December we will see another 25 basis point rate rise the 9th of this current cycle with plenty more to come. 2019 is slight different there is now a perfectly even split between a possible 2, 3 or 4 25bp hikes. However all plots moved slightly higher and that is why, my opinion has always been that 4 is the most likely outcome. We also got the first view of the Board’s projections for 2021, and saw an increase in the ‘longer run estimate’ – again a hawkish view and a USD strength view.

US economic strength as also been a core focus of my USD view and the moves in forecasts from the FOMC were, in the main, to the upside: the median GDP growth estimate for 2018 increase to 3.1% from 2.8% and up to 2.5% from 2.4% in 2019 while 2020 unchanged at 2 percent. Median estimates of PCE, core PCE inflation were unchanged.

The President remains furious with the Fed’s current course and has made no secret that if it was up to him rates would be lower. This push-pull between fiscal policy and monetary policy is moving to a new level as its clear that as monetary policy tightens fiscal policy will loosen – fiscal stimulus is more an economic driver than a USD weakener – my view holds.

Therefore I remain steadfast in the my view – all flows lead to the US and to do that, all flows look to the USD.

Author

Evan Lucas

FP Markets

Evan has over a decade experience in finance and financial markets and has worked in Amsterdam, Singapore and Australia. Evan's core passion is using macro economics for thematic trading.