The table has been set by Fed

The table has been set by Fed's Powell for higher and potentially faster rate hikes

In his semi-annual testimony before the Senate Banking Committee, Fed Chair Jerome Powell indicated that the Federal Reserve may need to raise interest rates more than originally anticipated due to recent strong economic data.

Powell stated that if incoming information suggests tougher measures are required to control inflation, the Fed is prepared to move in larger steps. He acknowledged that unexpected economic strength may be a sign that the Fed needs to do more to temper inflation, potentially returning to larger rate increases than the quarter-percentage-point steps previously planned. Powell's remarks virtually ensure that the Fed will project a higher endpoint for its benchmark interest rate at the upcoming March meeting.

The possibility of a half-percentage-point rate hike led to a quick repricing in bond markets, with investors boosting bets on such an outcome. Equity markets ended the day sharply lower, and the U.S. dollar rose, while yields on the 2-year Treasury climbed above 5% - the highest since 2007. Powell will testify again on Wednesday before the U.S. House of Representatives Financial Services Committee.

'Long way to go'

During the hearing and testimony of Jerome Powell, an issue was brought to the forefront which has become a major topic of discussion within the Federal Reserve. The officials are attempting to determine whether recent data is simply a temporary occurrence, or if it is indicative of a more persistent inflationary environment that requires a tougher response from the Fed.

Powell's testimony highlighted the fact that the impact of the central bank's monetary policy may still be in the pipeline, as the labour market is still sustaining a 3.4% unemployment rate, a level not seen since 1969, coupled with strong wage gains. While Powell believed that the Fed's 2% inflation target could still be achieved without a major blow to the U.S. labour market, he acknowledged that there would likely be some softening in labour market conditions.

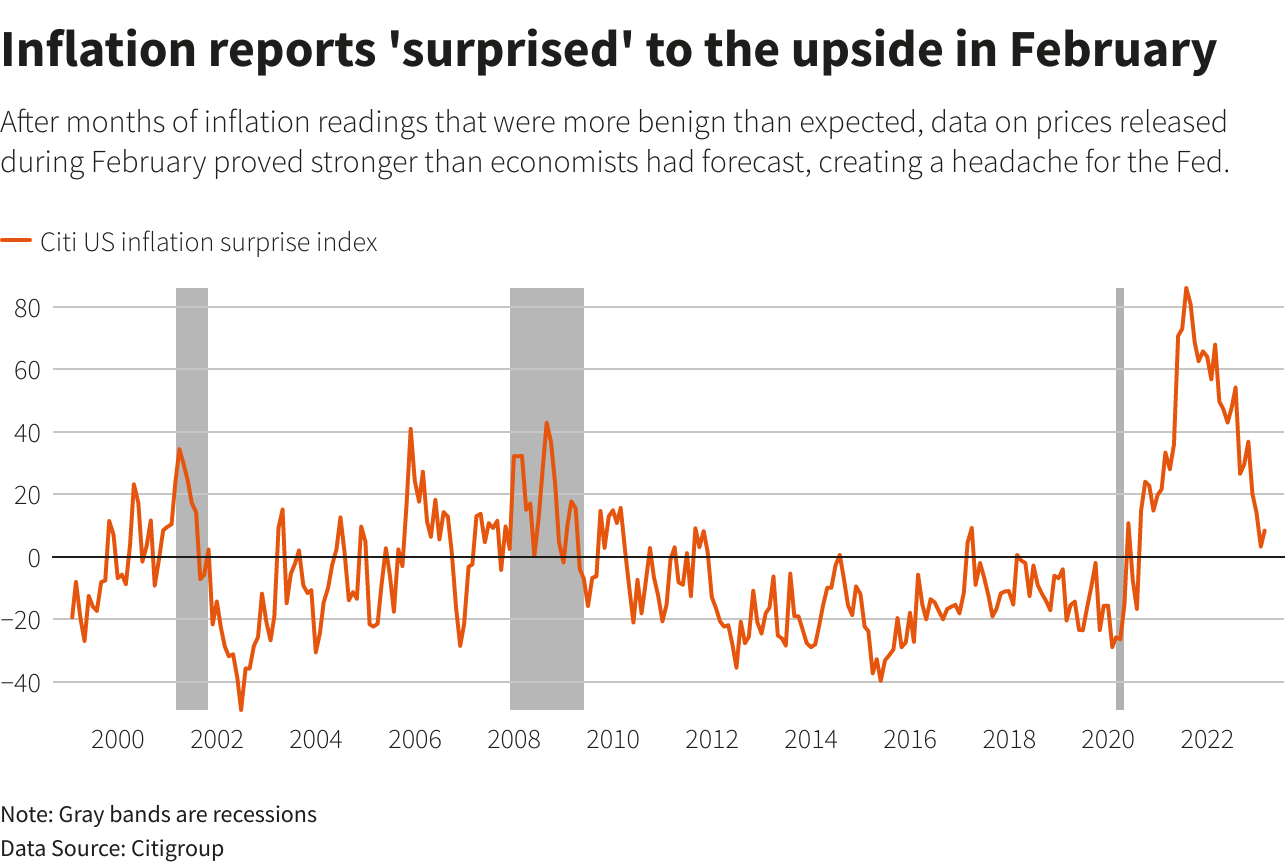

The extent of this softening, however, remains unclear, and Powell emphasized that the focus will be on how inflation behaves. Although inflation has decreased since Powell's last appearances before Congress, with the Consumer Price Index dropping to 6.4% in January from a peak of 9.1% in June, and the separate Personal Consumption Expenditures price index, which is used by the Fed as the basis for its 2% target, decreasing from 7% in June to 5.4% in January, Powell believes that it is still too high.

Powell stated that "the process of getting inflation back down to 2% has a long way to go and is likely to be bumpy," adding that "the social costs of failure are very, very high." Therefore, the Fed must remain vigilant in monitoring inflation and determining the appropriate response to ensure that it remains within its target range, while also maintaining a healthy labour market.

50bps rise seems more and more likely.

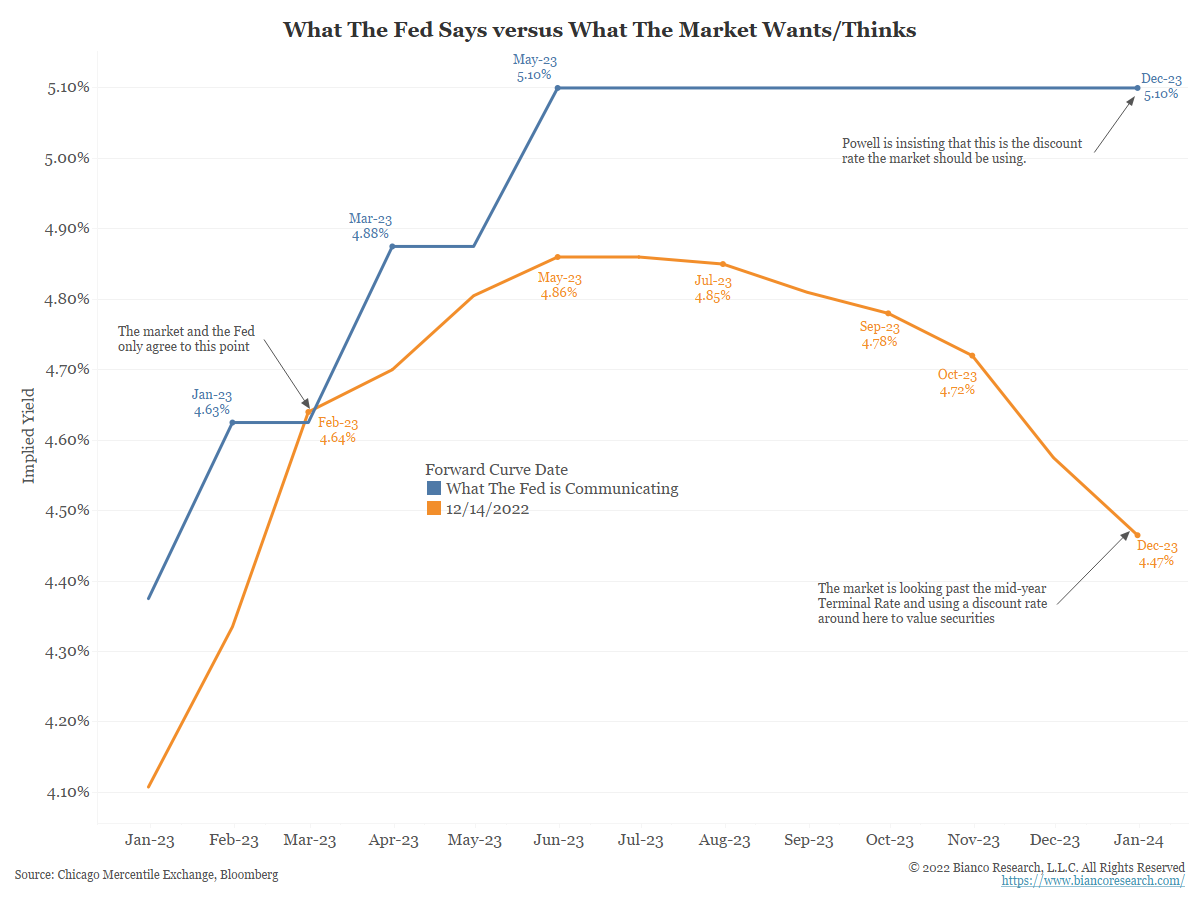

Where do short rates peak?

The chart below shows the divergence between what the Fed is communicating (blue) and what the market is pricing in (orange). The Fed is saying the terminal rate will be 5.00% – 5.25%. The market thinks it is closer to 4.86%.

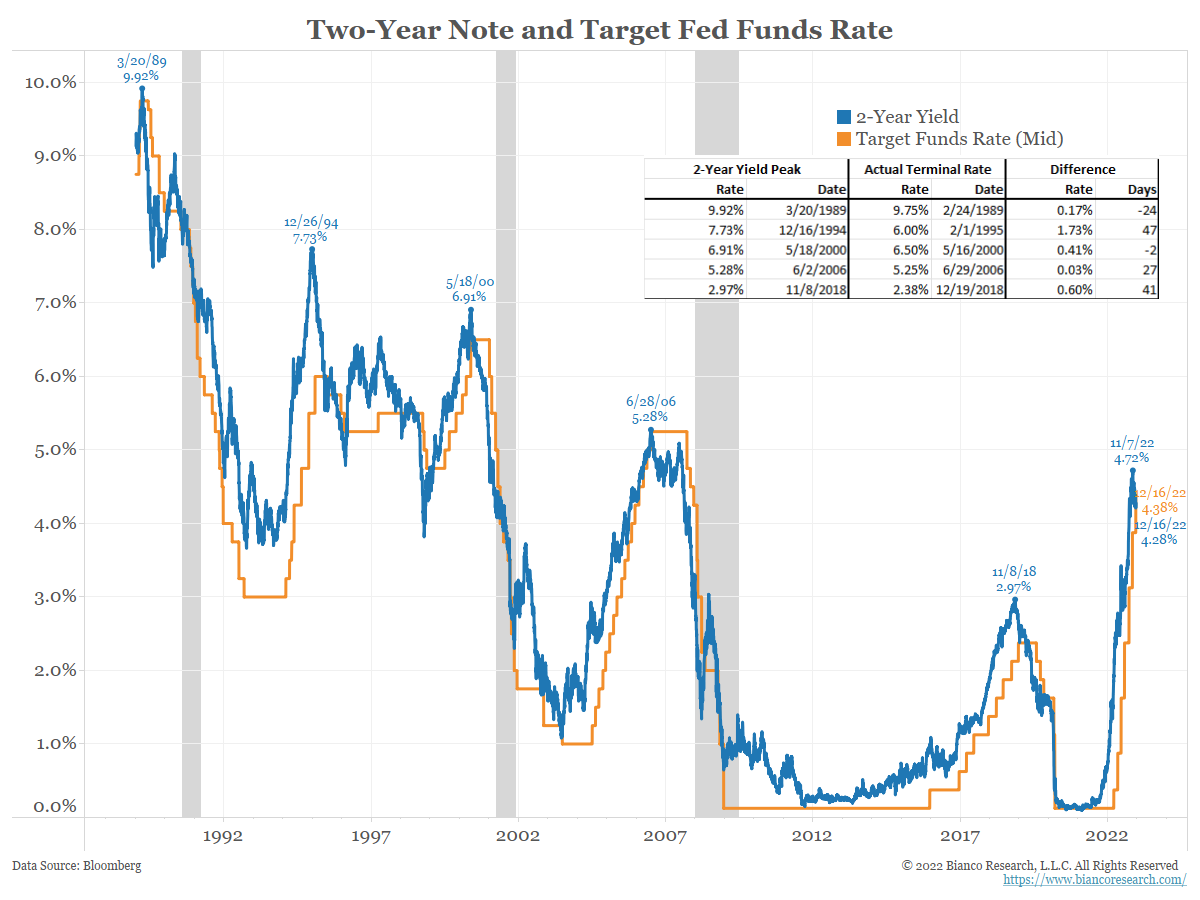

If the Fed is right and they are going to a 5.00% – 5.25% terminal rate, what does that mean for market-based interest rates such as the 2-year note?

The orange line below shows the target funds rate. The blue line shows the 2-year yield.

As the table shows, the last five rate hike cycles ended with the 2-year yield above the terminal fed funds rate. So, if the Fed’s projection of a 5% funds rate is correct, then history suggests the 2-year yield should be higher than this terminal rate, or at least 5.25%.

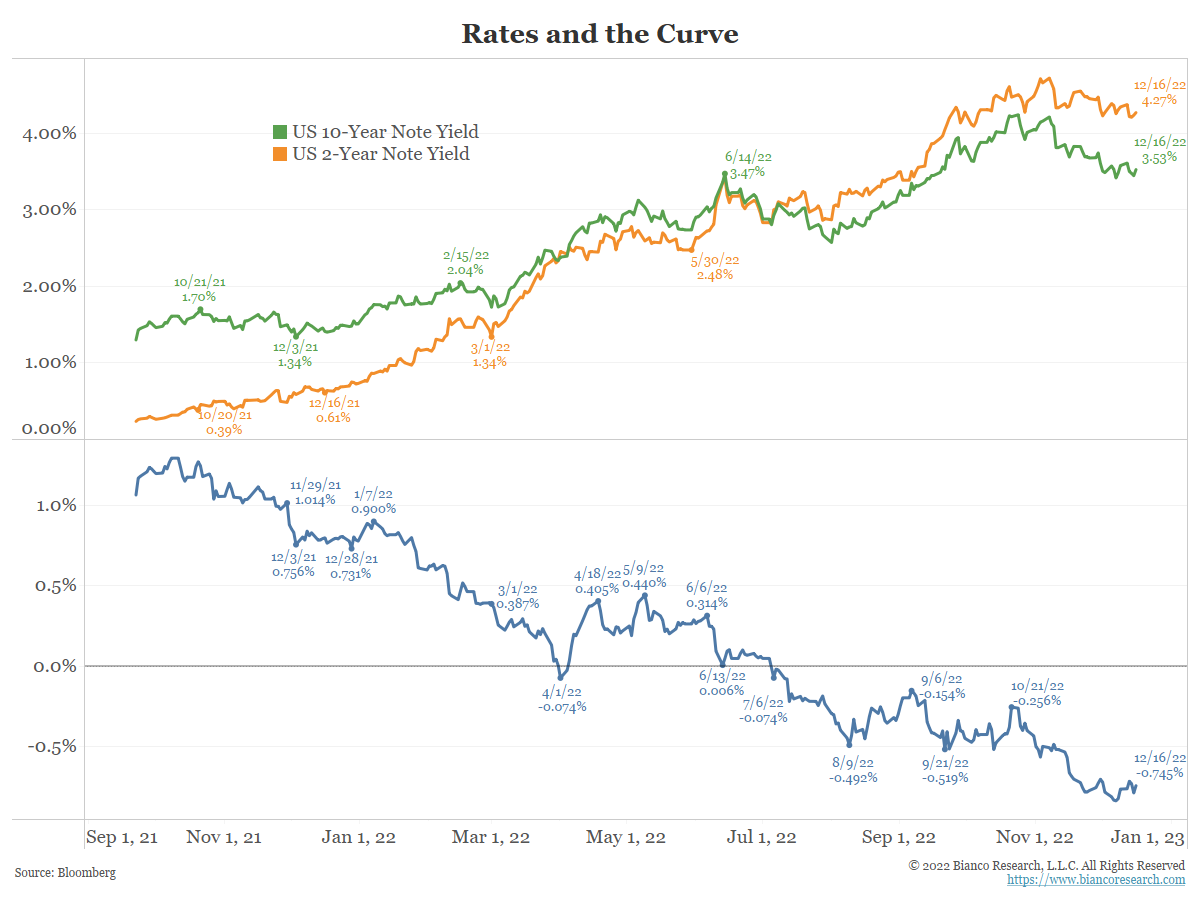

What does this mean for long rates?

Should the 2-year yield (orange below) keep climbing above 5.25%, we believe it will drag the 10-year yield higher (green). The yield curve (blue bottom panel), already at a 41-year extreme inversion, should not go much beyond -100 basis points, if it even gets that extreme.

So we look for long and short rates shift higher in parallel as the Fed continues to hike to their 5.00% – 5.25% terminal rate. If one is looking for a target, 2-year yields should reach 5.50% and 10-year yields should hit 4.50% by spring.

The economy is not breaking

The yield curve will stay range-bound precisely because the economy is not breaking, despite Wall Street’s near insistence that it will/should.

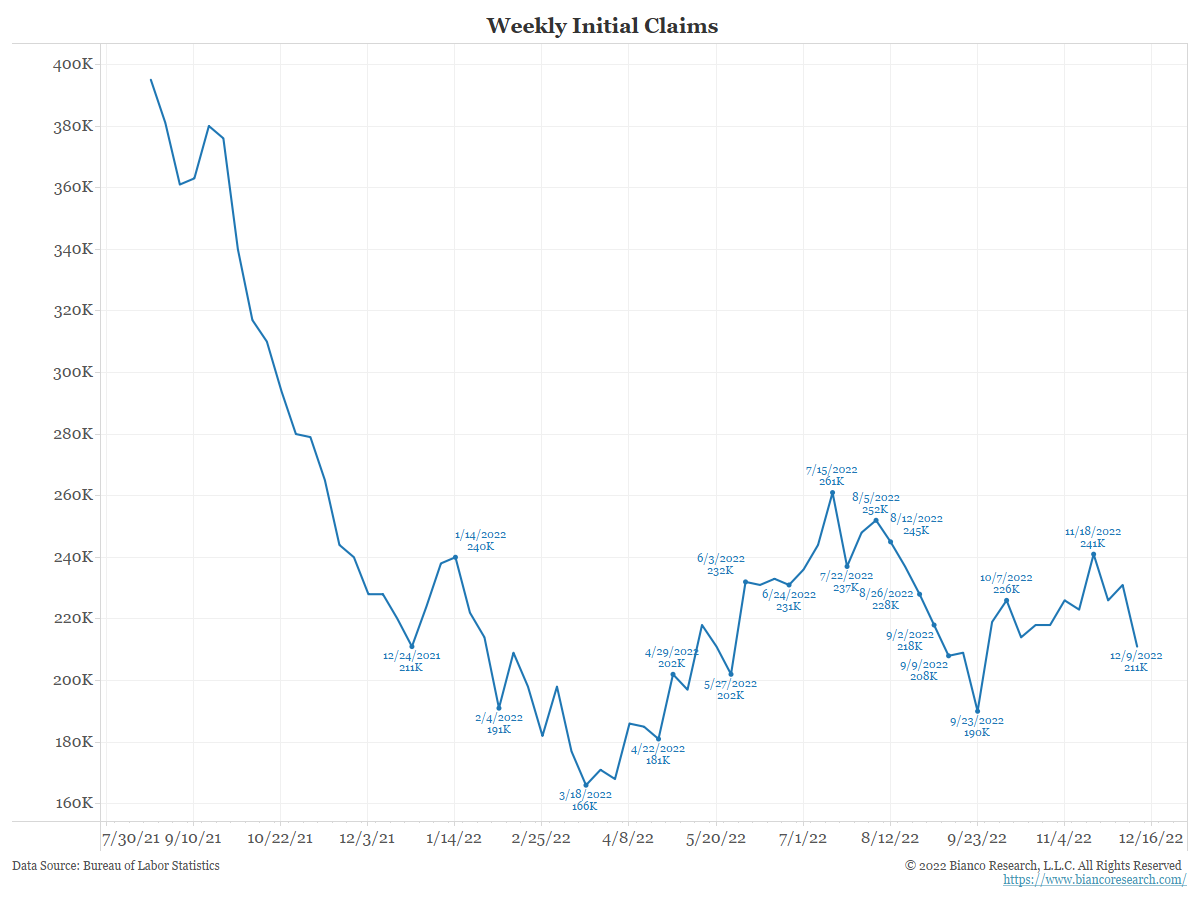

Consider the following chart of weekly initial unemployment claims. They are still not showing any sign of a weakening labour market.

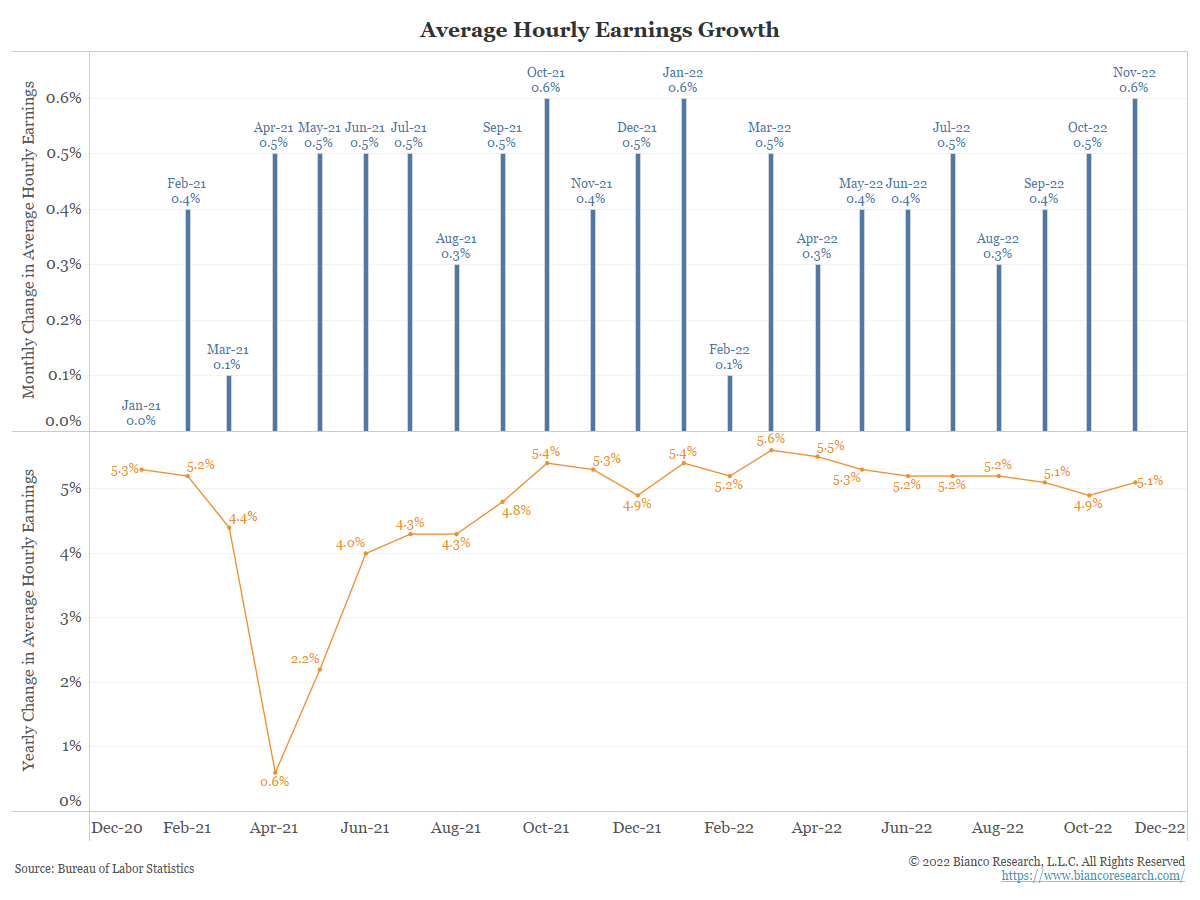

And without a weakening labor market, falling wage inflation is not materializing. As the bottom panel of the following chart shows, average hourly earnings are holding around 5%.

If everyone is getting 5% wage hikes, they can handle 5% inflation.

(Source: Bianco Research)

We believe rates have not peaked and will not peak until we see evidence of weakening wage growth. Until then, rates across the curve will shift higher in tandem as the Fed continues to hike rates into 2023.

Conclusion

After Federal Reserve Chair Jerome Powell suggested that strong inflation data might require more stringent measures, traders who deal in futures linked to the Fed's policy rate indicated that they were pricing in a half-percentage-point increase in interest rates at the central bank's policy meeting on March 21-22. The implied yields on fed funds futures contracts fell, indicating a 48% likelihood that the benchmark overnight interest rate would rise to the 5.00%-5.25% range from the current 4.50%-4.75% range on March 22. This probability was higher than the 30% chance that was observed prior to Powell's testimony before the Senate Banking Committee. The futures contracts also showed expectations of an increase in the policy rate to the 5.25%-5.50% range by June. However, this would depend on factors such as payrolls not slowing down and CPI numbers not showing disinflation progress. Scott Ladner, the CIO at Horizon Investments, suggested that the February employment report and the upcoming inflation report would be crucial in determining the pace of future rate increases. Powell's testimony on Tuesday indicated that the "disinflationary process" he spoke of on February 1 may not proceed as smoothly as he had anticipated.

Author

ACY Securities Team

ACY Securities

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis. The key pi