The States Are Strapped

For homeowners, garbage day is never pleasant. Getting the trash together takes some doing (and during the summer, nose plugs don’t hurt). There follows an argument among children over whose turn it is to take the bins out to the curb, which usually ends with a parent performing the chore to get it over with.

But it could be worse. In most areas, trucks arranged by local governments come through weekly to collect the detritus and take it to a dump. Imagine what the process would be like if pickup was provided only monthly, or not at all.

Yet this is the prospect faced by many U.S. communities for a range of public services. Poor fiscal health at the state and local levels clouds their economic futures, and ours; the situation promises to get worse as demographics march on. And if recession returns, some states may find themselves in very serious difficulty.

While major headlines often focus on the national economy and national debt, our state and local governments are prominent contributors to both. Combined, local governments employ more people and collect and spend more money than the federal government.

Sustaining public payrolls and expenditures requires money. Relative to the federal government, states and municipalities have limited sources of revenue:

But it could be worse. In most areas, trucks arranged by local governments come through weekly to collect the detritus and take it to a dump. Imagine what the process would be like if pickup was provided only monthly, or not at all.

Yet this is the prospect faced by many U.S. communities for a range of public services. Poor fiscal health at the state and local levels clouds their economic futures, and ours; the situation promises to get worse as demographics march on. And if recession returns, some states may find themselves in very serious difficulty.

While major headlines often focus on the national economy and national debt, our state and local governments are prominent contributors to both. Combined, local governments employ more people and collect and spend more money than the federal government.

Sustaining public payrolls and expenditures requires money. Relative to the federal government, states and municipalities have limited sources of revenue:

- Taxes.The majority of funding for state and local governments is through sales taxes, property taxes and income taxes. The rates and composition of these taxes vary by state. Seven states have no income tax, and four charge no sales tax. Income and sales taxes are especially susceptible to volatility during economic downturns: As consumers earn and spend less, local governments immediately feel the pain of lower tax receipts. Property tax receipts can also be cyclical, as we learned during the housing crisis ten years ago.

- Fees and fines. Some fees are routine, such as vehicle and business registrations. Fines, like traffic violations, are an unpleasant but reliable component of municipal income.

- Federal grants-in-aid. To support specific needs such as public health and education, the federal government provides funding to individual states. Infrastructure projects are often jointly funded by both federal and local taxing bodies. The amount of federal funding in state budgets varies from 17% in North Dakota to 41% in Mississippi.

From that base of income, states and municipalities provide a broad set of services. In healthcare, local governments manage Medicaid programs. Local governments provide education beginning with kindergarten and extending through public universities. They are therefore critical to the formation of human capital in the United States.

Under the best of circumstances, our local governments are stretched. They are now under even greater duress as the cost of healthcare rises and decades of pension obligations are coming due. Research by Morningstar found that 21 states had pension funding ratios worryingly below 70%.

State and local governments have mounting financial obligations and no reductions in demand for their services. How can they maintain solvency?

- Employer growth: New employers mean new jobs, additional tax revenue, more demand for housing and multiplier effects for local economies. States and cities have many motivations to offer incentives to attract employers. However, this can be a slippery slope. In the case of Wisconsin, the state’s incentives to attract the first U.S. factory for Foxconn Technology Group are approaching $4 billion—a generous package for a single facility promising 13,000 jobs. As states compete against each other to attract investment, they risk a winner’s curse of committing to public incentives greater than the value of the private investment.

- Tax increases and service reductions: A tax increase will immediately and directly raise revenue. Higher tax rates can deter new business investment and may give residents a reason to relocate—or, at minimum, a reason to be displeased with their elected leaders.

- Federal funding: While the federal government is an important source of state funding, the national deficit is growing, and the capacity for further support is limited.

Default is a growing concern. Until recently, government debt was considered very safe, with historians looking back to the Great Depression to find examples of insolvency in the public sector. However, the past decade has given us the default of Puerto Rico and bankruptcy declarations in Detroit, Michigan and Stockton, California. Municipal defaults remain rare but possible.

Overburdened state and local governments are a risk to both their residents and their investors. In the past year, Moody’s has issued debt downgrades from California to Connecticut, with Illinois teetering on the brink of a junk bond rating.

To avoid that fate, cost reductions are being stressed. There are some promising angles: neighboring cities or overlapping levels of government may merge in order to reduce administrative staff, such as the successful merger of Kansas City, Kansas, with Wyandotte County. On the other hand, many solutions designed to resolve issues of pension funding face immense political opposition. Cutting back on education seems short-sighted, as human capital is a key to economic success. The recent wave of teacher’s strikes is a clear sign of what’s ahead on this front.

Given the importance of state and local conditions to the national economic picture, failure to solve fiscal problems at this level would be damaging to the whole country. If the situation isn’t addressed soon, it will leave a mess for our children that will be almost impossible to clean up. Even if they all pitch in.

Carrying On

When a country has trade and budget deficits as large as those run by the United States, their currencies tend to come under pressure. To pay for excess imports, the local currency must be sold and converted to others, which lowers exchange rates. Devaluation can also entice otherwise hesitant foreign investors to purchase sovereign debt.

The U.S. dollar has yet to endure this fate. In fact, even as news about debt and deficits has worsened over the past several weeks, the dollar has unexpectedly gained strength. This turn of events has created challenges for other world markets (see next segment).

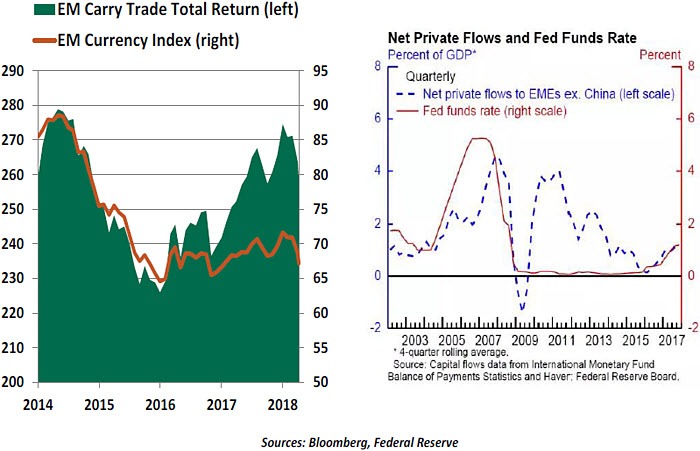

One of the subtle translation mechanisms involved in the contagion is the “carry trade,” in which investors borrow U.S. dollars and use the funds to purchase assets in markets with higher interest rates. For example, borrowing short-term in the U.S. costs just over 2% today; the dollars can then be used to purchase Argentine pesos and invest in Argentine 10-year bonds yielding 18%.

The combination is not without risks: if interest rates change, or if the value of the dollar increases, returns are diminished. Under these circumstances, capital can depart just as quickly as it arrived, leaving the recipient short. This has been an especially powerful force recently.

The dollar’s ability to defy economic gravity is due in no small part to its role as the world’s sole reserve currency, which (for now) remains unquestioned. Analysts still expect the dollar to lose a little of its edge as the year progresses. But for now, carry traders and the markets they use are in retreat.

Problems Re-Emerge

Emerging Markets (EMs) entered the year riding the waves of healthy global growth, improving commodity prices and a weak U.S. dollar. As discussed above, however, recent market conditions have put several EM currencies, stock indices and credit markets under pressure. This has brought back memories of the five-year-old “taper tantrum” and may prompt an end to the cycle of cutting interest rates in some EMs.

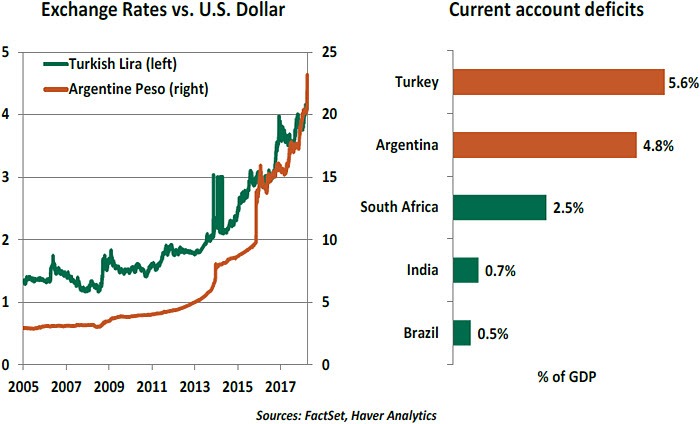

Both Argentina and Turkey have slipped at a worrying rate from being investors’ darlings to high-risk markets. In a little over a month, the Argentine peso (ARS) has depreciated by 15% and the Turkish lira (TRY) by 9.3%. Both are near their historical lows against the U.S. dollar.

Both the Argentine and Turkish central banks have moved to shore up their currencies. In a swift response to a rout in the peso, the Banco Central de la República Argentina (BCRA) increased its policy interest rates by an unprecedented 1,275 basis points to 40% in just eight days. Argentine president Mauricio Macri also approached the International Monetary Fund this week to seek a “financial line of support.”

Compared to Argentina, the response from Turkish policymakers has been relatively modest. The Central Bank of the Republic of Turkey (CBRT) raised interest rates by only 75 basis points in a single hike even as the TRY hit record lows against the dollar. With an election upcoming, the government is reluctant to take steps that might diminish its standing in the polls. Too many economic decisions around the world are scored using political points, not basis points.

Though the current volatility in these two countries is due largely to external factors, it has brought lingering domestic problems to the fore. Soaring inflation (24.6% in Argentina and 11.1% in Turkey last year), out-of-control government finances and heavy reliance on foreign capital are common concerns. These conditions make nations vulnerable to shifts in investor sentiment during periods of rising borrowing costs and currency movements.

Beyond economic mismanagement, both the BCRA and the CBRT have been criticized for insufficient independence from their governments. Recent examples of these include the efforts of Turkish President Erdogan to keep credit cheap ahead of June’s snap elections, and the BCRA’s decision to loosen its inflation target. International investors place special value on the ability of monetary authorities in emerging markets to remain distant from politics. When this distance closes, the risk of capital flight increases.

The markets do not appear to have taken comfort from the drastic policy measures by the BCRA and relatively milder action by the CBRT last week. Though central bank intervention will remain an important tool to limit the damage, it is time for the respective governments to urgently address the issues of high inflation and twin deficits through reforms. Argentina and Turkey, after a year of offering high returns to investors, are at risk of becoming victims of their past follies.

Author

Northern Trust Economic Research Department

Northern Trust

More from Northern Trust Economic Research Department