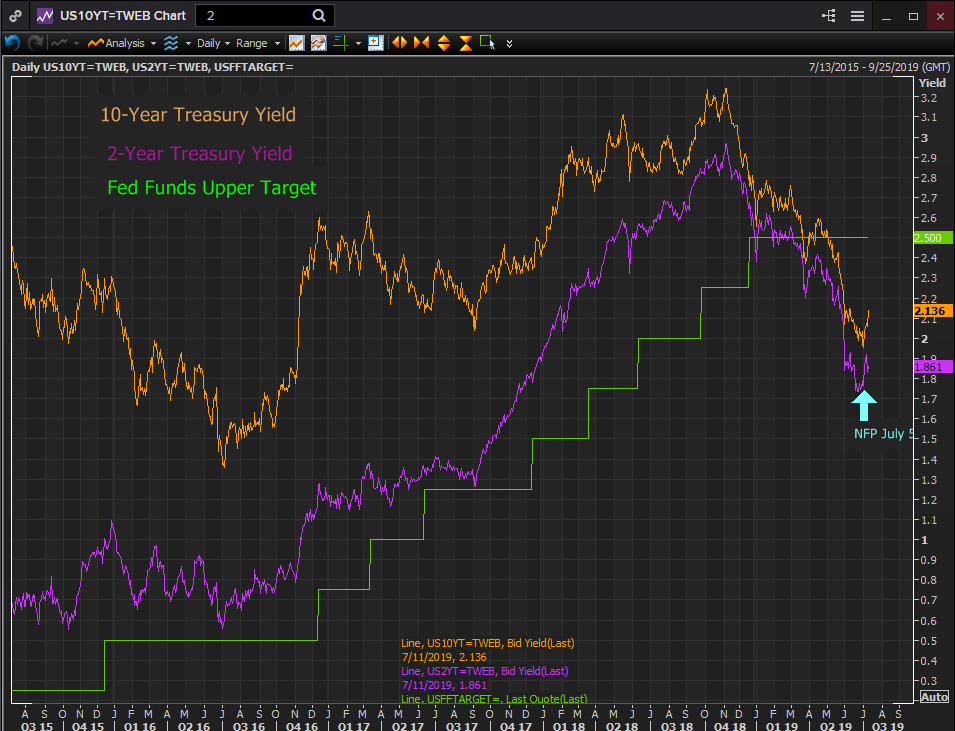

Treasury rates peaked and began falling five weeks before the Federal Reserve’s final rate hike on December 19th last year to 2.5%. By the evening before that FOMC meeting the 10-year Treasury had already lost 42 basis points from 3.24% on November 8th to 2.82%. The 2-year had shed 32 points, 2.97% to 2.65%.

Rates have once again turned. The 10-year has gained 18 point to a 2.13% close on July 11th. The 2-year has added 13 points to 1.86% also on the 11th. It traded as high as 1.92% on the 9th.

Reuters

It is far too early to tell if this is a reaction and profit taking on the eight month rise in bond prices or a hint that the odds of three or more cuts in the immediate future are waning in view of the June success at job creation. The sharp run higher in yields began on July 5th after the NFP report.

The Fed’s economic concerns from the beginning of the rate pause in January have been the US-China trade deal, Brexit and the slippage in global growth. Those remain today though Brexit seems to have wandered from immediate consideration. To them Chairman Powell has added the lack of sufficient wage gains to drive inflation.

Mr. Powell’s focus on wages and prices is less about inflation directly, though the Fed pays frequent homage to its Congressional price stability mandate, than to the wage component.

The Chairman noted several times in his two days of testimony that the long running expansion, recently a post-war record, had finally begun to deliver substantial wage gains to middle and lower class workers and that the very low level of unemployment had brought jobs to communities long outside of the general workforce. He stressed that keeping the economy in growth was one of the governors’ main considerations.

In response to a question in the House from Alexandria Ocasio-Cortez, the freshman Congresswoman from New York suggesting that the Phillips Curve, describing the relationship between unemployment, wages and inflation had largely broken down, he agreed.

That equation between the unemployment rate, wages and inflation holds that as the unemployment rate drops employers are forced to offer workers higher wages fueling inflation.

When the Philips Curve was first formulated in 1958, the global market was far more limited than it is now. The impact of trade on wages was minimal. National workers were not, by and large, competing with foreigners and so the domestic unemployment rate related to the wages employers had to pay to secure employees.

That is barely true now. The relationship has weakened as more and more production is or can be sourced overseas in cheaper wage environments. The Detroit auto worker or Pennsylvania steel hand is competing directly with workers in China and India and Vietnam. The labor market is global and it has effectively killed the national Phillips Curve. It has not yet been replaced, as it theoretically could be, by a global Phillips curve in a seamless world labor market.

Which brings us back to a Fed that is ready to cut rates on what would normally be considered tenuous economic grounds.

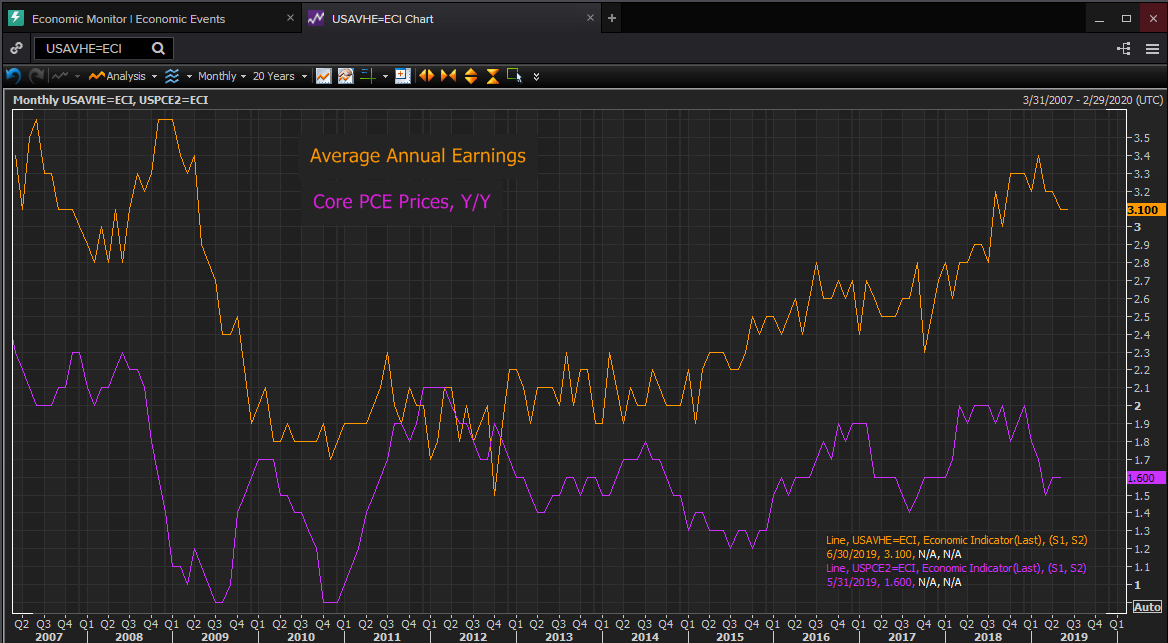

The economy is growing moderately, 2.25% in the first half if the Atlanta Fed GDPNow 1.4% second quarter projection is accurate. The bank’s final first quarter estimate of 2.7% was slightly under the final BLS measurement of 3.1%. Inflation is between 2.1%, core CPI and 1.5%, PCE price index, the labor market is healthy and wages are rising. Jobless claims and the unemployment rate are at levels that the 65% of the population under 50 have never witnessed.

If the expansion grinds to a halt or slips into a recession even if it is not a serious or prolonged downturn all the slowly accumulated pressures on wages would be lost. As wage increases are strongest in the last stages of an expansion it might take several years into the next recovery for unemployment to drop far enough to produce salary benefits, or it might never happen.

Wages did not start to open an appreciable gap over inflation until the second half of 2016. That edge which translates into disposable income continued to improve to its widest in a decade when, in August 2018 annual wages gains vaulted over 3%, where they have remained. The last eleven months have seen the best sustained wage increases since the recession.

Reuters

It is these wages accruing to all groups in society, but particularly to the most marginal and previously unemployed workers that Chairman Powell and the Fed governors are striving to retain and enhance.

Given the barely discernable impact of monetary policy, quantitative easing and seven years of zero rates on US prices, the demise of the Phillips Curve is just additional collateral when the Fed takes out its wage insurance policy on the 31st.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended Content

Editors’ Picks

EUR/USD holds gains near 1.0900 amid weaker US Dollar

EUR/USD defends gains below 1.0900 in the European session on Monday. The US Dollar weakens, as risk sentiment improves, supporting the pair. The focus remains on the US political updates and mid-tier US data for fresh trading impetus.

GBP/USD trades sideways above 1.2900 despite risk recovery

GBP/USD is keeping its range play intact above 1.2900 in the European session on Monday. The pair fails to take advantage of the recovery in risk sentiment and broad US Dollar weakness, as traders stay cautious ahead of key US event risks later this week.

Gold price remains on edge on firm prospects of Trump’s victory

Gold price exhibits uncertainty near key support of $2,400 in Monday’s European session. The precious metal remains on tenterhooks amid growing speculation that Donald Trump-led-Republicans will win the US presidential elections in November.

Solana could cross $200 if these three conditions are met

Solana corrects lower at around $180 and halts its rally towards the psychologically important $200 level early on Monday. The Ethereum competitor has noted a consistent increase in the number of active and new addresses in its network throughout July.

Election volatility and tech earnings take centre stage

/stock-market-graph-gm532464153-55981218_XtraSmall.jpg)

The US Dollar managed to end the week higher as Trump Trades ensued. Safe-havens CHF and JPY were also higher while activity currencies such as NOK and NZD underperformed.