The French labour market: Outlook for 2021

After a stand-out performance in 2019, the French labour market’s performance was even more remarkable in 2020 given the massive recessionary shock that swept the French economy. In part 1 of this article, we conducted a review of this very peculiar year in which the Covid-19 crisis had a much smaller impact on the French labour market than on GDP growth.

What should we expect in 2021? Will the labour market continue to surprise on the upside? Although we cannot rule out this possibility, for now, prospects seem to be more mixed. Payroll employment is expected to rebound, but the unemployment rate is also expected to pick up. And the size of these moves is highly uncertain. To be more precise, the balance of risks leans towards a mild increase in employment and a big rise in the jobless rate. This article will review he support factors and headwinds currently at work.

Payroll employment is set to rebound, but by how much?

Concerning the outlook for employment, there can be little doubt but that the situation is poised for a rebound in 2021. The big question is by how much? We can reasonably expect the year-onyear increase to be positive by the end of 2021. But will employment rebound sufficiently over the course of the year to return to pre-crisis levels by year-end 2021? Will the annual average growth rate swing back into positive territory? This would already be a significant improvement. Will it be strong enough to close the gap with job destructions in 2020 (when payroll job destructions averaged 328k)? Although we can answer the first two questions in the affirmative, the third hypothesis seems highly unlikely.

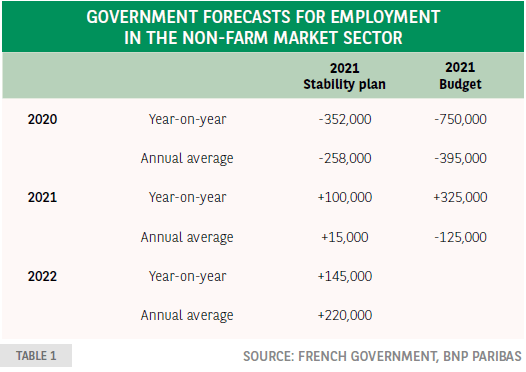

Government forecasts clearly illustrate the different messages circulating with these figures, depending on whether they are presented yearon- year or as the annual average. In 2021, the most positive signal is from the year-on-year change in employment, whereas in 2022 it is the annual average increase. The government’s forecasts are summarised in Table 1: the most recent figures are from the April 2021 edition of the Stability Programme, while the others are part of the 2021 budget, published in October 2020. This table also illustrates how employment surprised favourably in 2020: year-omarket than on GDP growth2.n-year job losses were a little over half the size previously expected. The more limited employment fall in 2020 translates into a more limited rebound in 2021 on a year-on-year basis, in the most recent forecasts for the Stability Programme. Since the negative carry-over was smaller, however, the 2021 annual average increase swung into positive territory, albeit slightly.

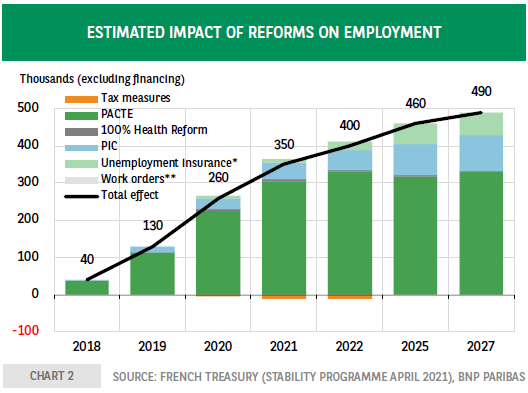

The reason why we expect to see a mild rebound in employment in 2021 is because there will be fewer and less strong tailwinds than headwinds. Among the support factors, there is of course the expected rebound in growth. There are also the specific positive effects of the youth employment plan, and more globally, of the France Relance recovery plan (+240,000 jobs by 2022 and +120,000 in the long term, according to government estimates presented in the Economic, Social and Financial Report as part of the 2021 budget). There is also the impact of the reforms already underway (see chart 2). Yet caution is still needed given the high uncertainty over the vigour of the recovery, the impact of support measures and the job-rich content of the recovery. However, Pôle emploi’s 2021 survey on companies’ labour need, released early May, sends an encouraging signal, with 2.72 million hiring plans, or 30,000 more than in 2019.

Author

_XtraSmall.jpg)

Hélène Baudchon

BNP Paribas