The fluctuation and trend of RMB exchange rate

Since the beginning of October, the fluctuation of the RMB exchange rate has increased significantly, and the trend of its appreciation has further accelerated. On October 21, the central parity rate of RMB has risen above the 6.7 mark to 6.6781; both onshore and offshore RMB exchange rateshit new highs in more than two years, while the offshore RMB exchange rate briefly rose above the 6.63 mark to 6.6289 against the U.S. dollar, its highest level since July 2018. The onshore RMB exchange rate rose above 6.65 against the U.S. dollar. Along with the growing strength of the RMB exchange rate, the market is also currently forming widespread doubts about whether the RMB exchange rate has entered an appreciation channel.

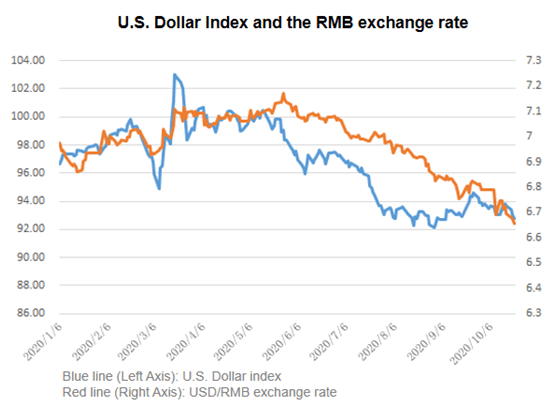

Since the beginning of this year, the RMB has shown a trend of continuous depreciation amid the impact of the COVID-19 pandemic, global financial market volatility, dollar liquidity strain, and strategic friction between China and the United States. By the end of May, the RMB exchange rate reached its lowest point of 7.16. Since then, the RMB began to appreciate, with the rate of appreciation accelerating from August onwards. So far, the RMB has risen nearly 7% against the U.S. dollar from its May low. From the perspective of China itself, many analysts believe that the continued appreciation of the RMB against the U.S. dollar is related to factors such as the containment of the pandemic in China, the sound economic recovery, the acceleration of capital market opening, and the relative stability of U.S.-China relations. Fundamentally, the RMB exchange rate still has room to continue appreciating in the short term.

In terms of changes in the international market, the rapid appreciation of the RMB is actually the result of changes in the U.S. dollar, which cannot be separated from the influence of the Fed's monetary policies. In fact, after the global financial markets emerged from the crisis caused by the outbreak, as researchers at ANBOUND have pointed out, the long-term consequences of the Fed's ultra-loose monetary policies began to be felt, sending the dollar into a depreciation trend. From a high of 102.99 in mid-March to a low of 92.34 at the end of August, the U.S. Dollar Index is still hovering around 93, losing nearly 10% of its value. The USD/EUR exchange rate has fallen from 1.0695 in March to the current 1.1852, a depreciation of 11%. Therefore, in terms of changes in the dollar, the RMB exchange rate has not been fully synchronized, meaning that the RMB has not fully appreciated relative to other major currencies. In terms of the new cycle of RMB appreciation, Guan Tao, chief economist at BOC Securities, said the current trend is not a typical RMB appreciation, but a two-way flow of bullish and bearish conditions. Even if the RMB has been rising recently, it is fundamentally different from the appreciation during the 2008 financial crisis.

In the short run, of course, the dollar will be in a downward trend as the pandemic continues, economic activities are constrained, a new round of stimulus policies and elections take place. Therefore, the RMB and other currencies will have a short-term appreciation trend. In the long run, under the current situation, ANBOUND had expected that the room for a sustained depreciation of the dollar was limited, and the short-term market fluctuations do not represent the medium- and long-term trend. From the perspective of the market, on the one hand, under the influence of the stimulus policy, the strong expectation of the U.S. economy could drive international capital back to the U.S.; on the other hand, if inflation picks up in the U.S. and the Fed enters an early rate hike cycle, the dollar will also be boosted. Therefore, the trend of the RMB exchange rate is still greatly influenced by U.S.-China relations and the U.S. economy, and it will not be excessively appreciated.

The impact of the fluctuation of the RMB is also multifaceted. On the one hand, exchange rate appreciation leads to the inflow of capital, and the increase of both direct investment and financial investment is beneficial to China's internal capital circulation. However, the excessive appreciation of RMB will bring great pressure to the export. Peng Wensheng, the chief economist of CICC, said that the appreciation of the exchange rate will affect the macroeconomy through two channels, one is the trade channel, and the other is the financial channel. On the whole, because the exchange rate has limited side effects in the trade channel, while the financial channel is favorable for real estate and credit expansion, the RMB appreciation will have limited negative effects or even beneficial to China's economic growth before the pandemic is effectively controlled or subsides. However, a rapid appreciation of the RMB would also bring about a bubble in the market, which would not be conducive to structural adjustment and endogenous growth in the long run.

At present, from the perspective of the policy direction of the central bank, although the central bank prevents excessive fluctuations of the RMB exchange rate by adjusting the risk reserves of foreign exchange transactions and issuing the dollar-denominated bond, its main idea is still to adopt indirect means to avoid market turbulence. In addition, there is no excessive intervention to reverse the trend of the market in the change of supply and demand of the RMB.

From the perspective of geopolitics and historical development, the change of the RMB exchange rate is mainly affected by the trend of geopolitical development and change. At present, the U.S. dollar is the dominant currency in the international market. The dominant power of the RMB exchange rate is not in China and it remains subject to changes in the dollar and the Fed's policies. Under the fluctuating trend of the dollar, RMB, as a geopolitical currency, can take advantage of this trend to adjust and promote the process of capital market opening and RMB internationalization. That being said, it is still necessary for China to grasp the trend of the dollar.

Final Analysis Conclusion

The fluctuations and changes in the exchange rate of the RMB against the U.S. dollar are, in fact, mainly influenced by the changes in the U.S. dollar and the Fed's policies. That means the RMB will not be excessively appreciated. This influence actually depends on the pattern and changes of geopolitical currency and it is a long-term trend.

Author

ANBOUND Team

ANBOUND Research Center Sdn Bhd