The February Grab-Bag Preview: Personal Income, Spending, Core PCE Prices and GDP

- Personal Income expected to plunge 7.3% in February as stimulus fades.

- Personal Spending to fall 0.7% after increasing 2.4% in January.

- Core PCE prices forecast to be stable at 1.5% on the year in February.

- Fourth quarter GDP to be unchanged at 4.1% annualized in final revision.

- February statistics provide no new economic information or market directives.

The expected crash of Personal Income in February as the stimulus is withdrawn will be remembered as just a statistical oddity if the latest pandemic payments restore the labor market and the US economy to health.

Personal income, a category that includes all sources, is forecast to drop 7.3% in February after soaring 10% in January on the second stimulus relief bill passed by Congress and signed by President Trump in December.

Personal Spending is predicted to slip 0.7% in February following a 2.4% increase in January.

The Core Personal Consumption Expenditure Price Index is projected to be unchanged at 1.5% on the year in February.

Fourth quarter US economic growth will be 4.1% annualized after the final revision to GDP from the Bureau of Economic Analysis, a division of the US Commerce Department.

Income, Retail Sales and Spending

February will end being a pause between the stimulus driven income and spending boom of January and the stimulus and job creation recovery of March and the entire second quarter.

The modest $600 individual grants that arrived in January facilitated the largest one month gain in financial resources, excepting the lockdown recovery, in over two decades. Personal Income jumped 10% on the month.

The pandemic grants also spurred the largest spurt in Retail Sales, again barring the rebound of May and June, in almost two decades. All three categories of Sales saw large initial gains that were revised even higher two weeks later.

Personal Spending, which includes all purchases of goods and services by a household, jumped 2.4% in January, second only to the 8.7% and 6.5% increases in May and June.

In its first release January Retail Sales rose 5.3%, that jumped to 7.6% after adjustment, Sales ex Autos added 5.9% revised to 8.3%, and the Control Group, which mimics the consumption component of GDP, originally 6% became 8.7% after adjustment.

Retail Sales

The revisions, 2.3% for Sales, 2.4% for ex Autos and 2.7% for Control, reversed most of the February losses in the three groups, respectively, 3%, 2.7% and 3.5%. The February Sales results will themselves be revised by the US Census Bureau at the end of March.

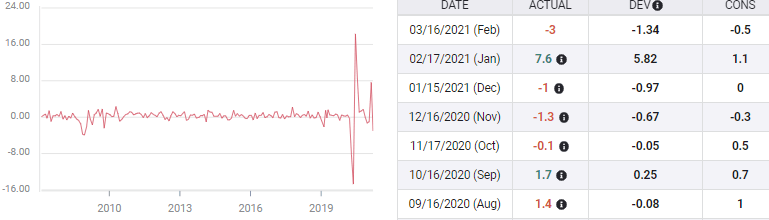

Core PCE Prices

Inflation has not rebounded to its 2019 levels. The Core PCE Price Index, the Fed's elected measure of consumer price changes, has not been at the bank's 2% target since December 2019. For the year it averaged 1.7%. It was 1.9% in February 2020 before the collapse in consumer spending drove it to 0.9% in April and 1% in May. The January rate of 1.5% has been the post-lockdown high.

Low performance is not the only impediment to inflation-pressured Fed rate increases. The bank's six-month old inflation averaging policy, which assumes a period of above standard inflation to balance the weak rates of the past decade will, and is designed, to preclude any fed funds increase speculation based on rising prices. The Fed's own predictions do not see any increase until after 2023.

Core PCE Prices

Conclusion

Personal Income and Spending restate economic information already available from other sources. Core PCE Inflation is a modernized version of the Consumer Price Index and also offers no special insights to price dynamics. Its main attribute is that its reformulation produces a lower, and when adopted central bank pleasing, inflation rate. The third and final revision of GDP rarely results in any changes to the growth rate.

These four statistics provide a more detailed view of the US economy. They do not contain new information, nor will they leave any mark on the markets.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.