The European Union’s energy transition: Roping up is needed to climb this Everest

In order to achieve its climate targets, the European Union will not only have to green its electricity production, but also increase it. This is a daunting industrial and financial challenge, echoed in the “Draghi” report on the future of European competitiveness, as well as the new Green Deal proposed by the re-elected President of the European Commission, Ursula Von Der Leyen.

It is said that, more often than not, the European Union (EU) makes progress when its back is against the wall. Everything that could have divided it to date, such as the financial crisis, the sovereign debt crisis, Brexit, the COVID-19 pandemic and the war in Ukraine, has, conversely, made it stronger. Stability and settlement mechanisms have been set up, while the principle of risk sharing, originally excluded, has gained ground both mindsets and actions. The launch of the Next Generation EU plan in December 2020 was a turning point for this, with the twenty-seven member states opting to tie their fate to a large and common debt issuance rather than facing one of the worst health disasters in history alone.

Common debt is once again a focus in the “Draghi” report1 on the future of European competitiveness, but on a completely different scale. In order to counteract the effects of its ageing population and boost its productivity, the EU should, according to the Commission, invest between 750 and 800 billion euros more each year, the equivalent of five GDP points and at least two Marshall Plans. While, thankfully, it is no longer dealing with rebuilding a continent, but the task ahead is no less extraordinary, not least because of the climate challenge that it has to overcome.

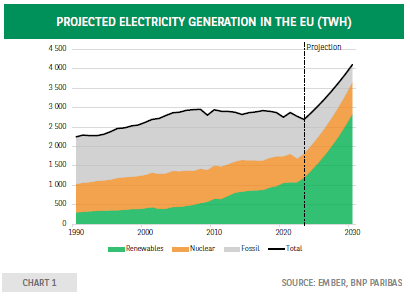

Under an ambitious “Green Deal” (which is by the way evolving, see box), the twenty-seven member states have set themselves the target of achieving carbon neutrality (net zero emissions) by 2050, mainly through the deployment of renewable energies. This requires not only to green electricity production but also increase it shortly, in order to drive the transformation of usages (such as the gradual phasing out of internal combustion engine vehicles, the replacement of oil and gas boilers with heat pumps and the conversion of industrial sites). Based on assessments by the EMBER research institute2, in order for the EU to meet its climate targets, it will have to ramp up its electricity production by at least 50% by 2030, following years of stagnation. At the same time, the very nature of this production must change, so that the EU can mainly rely on (55%, compared to the current level of 27%) the two primary sources: solar and wind power (chart).

Depending on the growth scenario retained, wind and solar farm capacities should be increased by a factor of 2.5 to 3 by 2030, which de facto underlie significant investments. It is therefore no coincidence that the call for a general mobilization in the Draghi report targets the energy transition, which, beyond being an existential challenge, is now a competitive arena between major economies, firstly China and the United States. In order to ensure that “greening” does not go hand in hand with “declining”, the EU will have raise resources that States alone cannot provide, due to budgetary constraints. The mobilisation of private savings, which is abundant but still too siloed in absence of capital markets union, is one of the solutions. Relaunching a common debt funding on a massive scale could be another.

Green deal: What developments can we expect with the new Von Der Leyen commission?

In its initial version in 2019, the European Green Deal structured the fight against climate change around two strands, i.e. environmental preservation on the one hand (such as restoring damaged ecosystems, expanding protected natural areas and preserving biodiversity) and the decarbonisation of usages on the other hand (such as the transition of industry and services to clean energy and the thermal insulation of buildings). The new European Commission, in line with the campaign messaging of its re-elected president, Ms Ursula Von Der Leyen, is clearly focussing on the latter of these two strands. The Green Deal is evolving into a more pragmatic “new Clean Industrial Deal”, recognising competitiveness issues, which was a point also highlighted by the “Draghi” report.

An example of this change is the creation of a Commissioner for Energy and Housing, with Mr Dan Jorgensen (S&D, Denmark) appointed to the role. Other European decarbonisation players, such as Spanish Commissioner Teresa Ribera (S&D, who will oversee the “clean, just and competitive transition”), or French Industry Commissioner Stéphane Séjourné (Renew), will have to work with Jorgensen on these issues. Another noteworthy appointment is Mr Wopke Hoekstra (PPE) as the Commissioner for Climate Action, as, in his former role as Minister of Foreign Affairs and Deputy Prime Minister of the Netherlands, he had expressed his opposition to the Nature Restoration Law, which was finally adopted in June 2024.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.