The ECB meets and is universally expected to cut rates again on Thursday

Today we get the final PMI’s from Japan, Australia, the UK, US and eurozone, plus the ISM manufacturing and construction spending in the US. The big data-drivers will be ADP private sector jobs on Wednesday and nonfarm payrolls on Friday. Before that, the ECB meets and is universally expected to cut rates again on Thursday.

US inflation has already been pushed off the stage by political showboating but let us not forget that Friday’s data, while sort of okay to most, is not. WolfStreet points out that if you annualized the monthly PCE of 0.33%, it’s 4.0%, the worst month-to-month increase since March 2024. The 3-month PCE price index rose to 2.94% annualized, the worst since April 2024. Here’s a kicker: “The low point of the three-month index was in July (+1.6% annualized), and it has been accelerating ever since.”

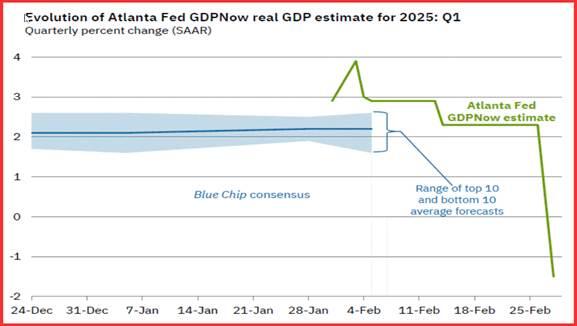

And the Atlanta Fed uses the drop in consumer spending as a key input to its latest GDPNow, out last Friday. The model for Q1 crashed from 2.3 on Feb 19 to a horrendous -1.5%, led by the crash in net exports and consumption spending, which fell from 2.3% to 1.3%.

This chart is one of the most dramatic we can remember ever seeing since Greenspan was in office.

ING went whole-hog negative on Friday after the PCE numbers came out. The essay points to the Trump policies cutting down consumer confidence and prodding importers to front run. It’s really important that consumer spending fell 0.5% on the month. Even gains in Feb and Mar will leave Q1 at a lousy 1.6% annualized, the worst since Q2 2023.

Personal income rose 0.9% but Social Security gets most of the credit. Wages and salaries rose only 0.4% and tellingly, household savings rose from 3.5% to 4.6%.

The Trump positives (deregulation tax cuts) are still among the missing, while the negatives (tariffs, general meanness) abound. And the trade gap continues to widen, likely due to that preemptive importer buying.

“The upshot of all this is that the market is seemingly starting to put more emphasis on the growth story over the inflation story, with Fed funds futures contracts now pricing in 61bp of Fed rate cuts for this year versus the 28bp priced just over two weeks ago. That looked too low to us and for now we are sticking with our two 25bp rate cut call for 2025 (September and December) with a third cut coming next March.” Note that the CME FedWAtch tool is sticking with June for the first cut. ING has September. Eeek.

But Europe has quite a mess, too. Reuters’ Dolan focuses on that today, pointing out that the ECB can hardly be expected to navigate well the oddly messy economic and political situations. The ECB will be issuing new long-term forecasts but knowing full well they will be discarded. “Uncertainty about potential U.S. tariffs, the identity of the new German government, the fate of Ukraine and a likely new public spending boost to re-arm the continent are all fogging up ECB eyeglasses considerably.

“As [the ECB] would probably admit itself, staff forecasts at this juncture are little more than a finger in the wind. Further complicating things is the fact that several critical macroeconomic inputs used to assess the ECB's inflation outlook have been swinging back and forth wildly this year. Take European natural gas prices. From the middle of January, they rocketed about 30% higher, only to reverse all that by the middle of last month.”

That’s just for starters. Bottom line, the ECB faces perhaps rushing stimulus before inflation is really in hand.

What a hodgepodge of factors! You’d think the tariffs becoming real tomorrow would drive the dollar up, as tariff terror has done before. But not this time. Maybe it has been overwhelmed by US growth concerns becoming red-hot.

Forecast

We wrote Friday that “Logic dictates relative yields will rule.” But logic fails when sentiment is hit over the head with something shiny, like tariffs. They have a tremendous information effect even as we do not know the true economic consequences down the road. But the recent gain in US yields is being matched by yields everywhere (except Chile). See the table from Trading Economics.

We are mired in a swamp of tariff terror (dollar up) and growth grinding down (lower yields and lower dollar). We tend to think of the tariff factor as short-lived, if repeating, while the slow-growth/low yields is the real deal and more long-lasting. If so, it implies the dollar rally will be short-lived. You’d think the recent revival of the 10-year yield erases that argument, if it persists, except everybody else has rising yields, too, and it’s the relative differential change that counts, not the actual number.

The dollar is prevailing against some, but not all. We have a convincing sell signal in the CAD and AUD/NZD, with the euro and pound close behind. Our morning work is deliberately very slow from a serious risk aversion but it’s possible we could reverse signals sometime soon, unless the dollar retreat persists. Again, beware turnaround Tuesday.

The only forecast we can make with any confidence is the CAD and the peso—although we could get a “buy on the news” effect—we already know the worst.

Tidbit: Reporter Fareed Zakaria had a wonderful riff on the Bill Maher show last Friday. Instead of assuming he was dealing with a sane and reasonable president, Zelensky should have invented a first-ever civilian award for excellence and bravery to give Trump, flattering him to the skies as unique and splendid in all history, and with the thanks of the Ukrainian people. This would have been several steps above the King Charles invitation for a royal visit but we agree it would have worked.

Separately, a Reader wrote to say since the Nobel peace prize Trump so longs for is awarded by a Norwegian committee of five (one of whom is named Gry), he can easily “award” no tariffs to Norway on US imports of oil and gas. Also fish and nickel, the top three exports to the US. Statistica points out Norway also exports arms to the US.

There is a website for US-Norway trade, too. It’s surprisingly interesting. The trade US deficit is $2 billion. “U.S. total goods trade with Norway were an estimated $11.2 billion in 2024. U.S. goods exports to Norway in 2024 were $4.6 billion, down 8.6 percent ($429.6 million) from 2023. U.S. goods imports from Norway totaled $6.6 billion in 2024, up 7.7 percent ($469.0 million) from 2023. The U.S. goods trade deficit with Norway was $2.0 billion in 2024, an 82.2 percent increase ($898.6 million) over 2023.”

Gee, a Nobel peace prize has to be worth $2 billion, especially since it wouldn’t be Trump himself paying for it. All the same, the Nobel committee knows full well its name would be blackened for generations if it awarded anything to Trump. Norway is all too familiar with how the Russians behave when they have free rein. And it was Crown Princess Märtha of Norway who talked Pres Roosevelt into Lend-Lease, or so one version of history has it. Trump does not know any history and would have no respect for it if he did. That doesn’t mean he won’t try.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat