The curious case of languishing Silver prices

Silver has languished despite its persistent structural deficit between silver’s supply versus demand.

The metal is increasingly difficult to find and produce, while demand continues to rise. None of this has seemingly been reflected in the price.

The "paper" silver markets, where the price is set, have been stuck in a range since early 2020.

Supply and demand are economic laws that can only be circumvented temporarily.

Nevertheless, the law still applies.

The forces involved at present point to higher prices for silver.

The Silver Institute reports the all-in sustaining cost (AISC) for producing silver jumped by 57% year over year. The industry average is now estimated at $17/oz for 2023, although some data suggest the attributable cost of producing byproduct silver from (copper, zinc, and lead mines) is much lower.

Many firms, including one of the world’s largest primary silver producers, have costs much higher than the average. Pan American Silver reported AISC at $26.55/oz in Q4 of last year. That was more than $4/oz above the average price they received.

Nearly all miners saw margins take a beating in 2023. While costs surged, the average silver price was essentially flat year over year.

Silver mining stocks have been decimated. The Global X Silver Miners ETF has fallen from a high of $49.65 in August 2020 to $23.33 at Friday’s close.

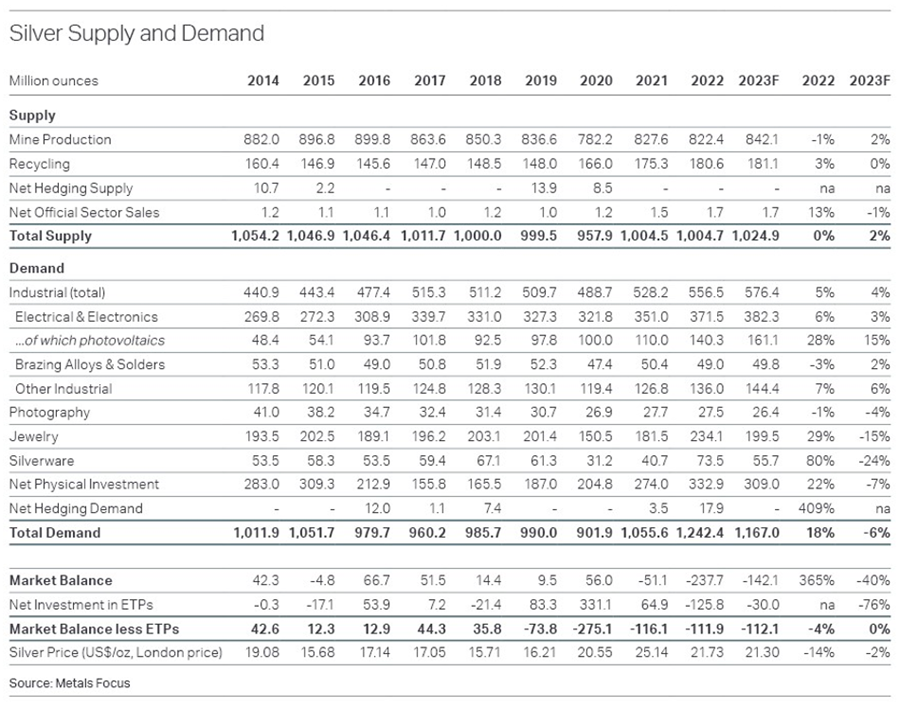

Given the challenging environment for miners, it is no surprise that silver mine production keeps falling. The Silver Institute estimates that mine output fell by 17.1 million ounces in 2023.

Meanwhile, demand has moved significantly higher since 2020. The chart below tells the story.

The deficit between supply and demand was 140 million ounces in 2023. When you add the deficits in 2021 and 2022, the total is 474 million ounces. That 3-year deficit is significant. It averages roughly 15% of the total annual production of just over 1 billion ounces.

And the Institute estimates the deficit will be 180 million ounces this year.

The gap between annual supply and demand has to be filled by existing above ground stocks – of which there are reportedly several billion ounces, including ounces that are outside of exchange warehouses and other stockpiles making tracking more difficult.

The steady decline in COMEX vault inventories has been well covered here among other places. The reported COMEX stockpiles of silver have fallen from a peak of about 400 million ounces in 2021, to about 281 million ounces currently.

There are some questions as to the accuracy of publicly available silver inventory statistics. For example, some argue that JPMorgan Chase, who acts as both the custodian of the 100+ million ounces held by the I-shares Silver Trust (SLV) and about 130 million ounces of COMEX silver, is reporting some silver bars in both places.

Most would assume these inventories are different.

Investors who hold shares of SLV might be interested to know whether the silver owned by the trust is also shown as “eligible” in the bullion bank’s daily report of COMEX stocks.

While that question should be easy for regulators to answer, analyst Ted Butler has been waiting months for a reply. The delay is not encouraging.

Should the deficit between output and consumption persist, it is hard to see how the silver price won’t move higher to draw out new supply and/or curb demand.

To receive free commentary and analysis on the gold and silver markets, click here to be added to the Money Metals news service.

Author

Clint Siegner

Money Metals Exchange

Clint Siegner is a Director at Money Metals Exchange, the national precious metals company named 2015 "Dealer of the Year" in the United States by an independent global ratings group.