That slow grind

S&P 500 continued extending gains no matter the sectoral non-confirmations – the momentum from bonds had been enough as telegraphed both in yesterday‘s analysis and intraday updates (pointing to increasingly thin air up there in this liquidity based rally). The appropriate view is to compare the underperforming stock market rally meeting deteriorating earnings first, against outsized gains in precious metals and commodities.

Before the core PCE report, we got plenty of chop indeed. The eurozone headline vs. core inflation data have been favorable to the bearish stocks thesis (explained in the linked to thread). The figure came in slightly below expectations, by a miserable 0.1% year on year, which is hardly enough to dissuade the Fed from tightening. No real fireworks – today or Monday.

Crude oil is to lead today higher, followed by silver. Not expecting daily miracles from copper, and gold would continue treading at $2,000 still, all of which has risk-off undertones. Undertones – it‘s not enough to send stocks into daily decline. The daily outlook continues being ever so slightly but still bullish.

Keep enjoying the lively Twitter feed via keeping my tab open at all times – on top of getting the key daily analytics right into your mailbox. Combine with Telegram that never misses sending you notification whenever I tweet anything substantial, but the analyses (whether short or long format, depending on market action) over email are the bedrock. So, make sure you‘re signed up for the free newsletter and that you have my Twitter profile open in a separate tab with notifications on so as to benefit from extra intraday calls.

Let‘s move right into the charts.

S&P 500 and Nasdaq outlook

4,039 won‘t again come into jeopardy (and neither will 4,015 as the going won‘t get really tough in the core PCE aftermath either). Liquidity is still lifting this boat for now. It doesn‘t matter when exactly 4,115 target would be reached, but on what kind of non-confirmations (if reached at all – it‘s hard to time when tech starts gasping for breath).

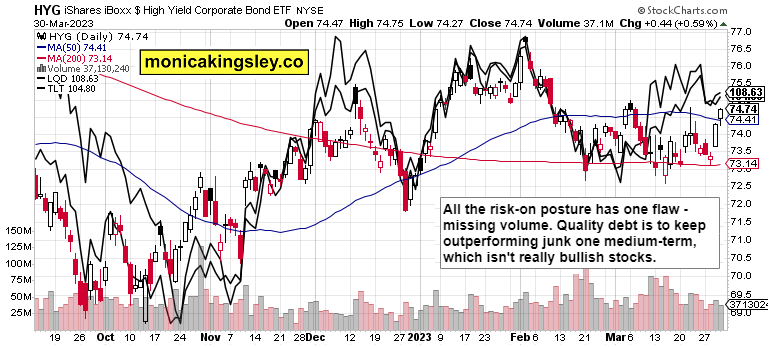

Credit markets

Bonds aren‘t to turn risk-off today, and would pose no obstacle to the stock market bulls. The short end of the curve should act reserved about today‘s data, and long end would continue drifting very slowly higher.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.