Tariff tantrum: Trump’s auto salvo shatters market calm in a risk-off rout

US markets

Three days of relative market calm just got obliterated. With the tariff fog rolling in fast and thick, markets have flipped hard into risk-off mode, shattering the fragile rebound that had been taking shape. The opening salvo of a trade-policy storm has officially blown the tentative recovery off course. Investors are scrambling—ducking for cover, dusting off their trade war playbooks, and reaching for their metaphorical helmets. But let’s be clear: some were clearly caught off guard when "Tariff Man" flexed hard with Wednesday’s warning shot. “We’re going to go with the tariffs on cars,” Trump declared, just hours ahead of the formal Oval Office rollout.

Sure, traders have a love-hate relationship with tariff uncertainty—but when it comes to autos, that anxiety hits a whole different gear. The auto sector is the epicentre of the economic fallout from trade wars, with its globally integrated supply chains, slim margins, and massive cross-border employment footprint.

Target autos with tariffs, and you're not just bruising one sector—you're disrupting consumer sentiment, choking off corporate investment, and sending shockwaves through global trade flows. Tariffs on widgets are background noise. Tariffs on cars? That’s the headline risk with teeth.

It’s a stark reminder: Trump’s not bluffing—or at least he’s doing a damn good job pretending he’s not. And if he goes full throttle with this round of tariffs—especially the reciprocal measures slated for April 2—markets are staring down the barrel of the worst-case macro cocktail: faster inflation, slower growth, and a fresh wave of volatility.

Soft landing? Meet hard reality

A wave of broad risk reduction—led by heavy selling in tech—is dragging major benchmarks lower. The real question is how much of this tariff drama will bleed into the real economy, especially as inflation concerns re-emerge, fueling the fire. With the inflation dragon breathing down Chair Powell's neck just as global trade tensions escalate, risk appetite has taken a hit from both sides of the nasty spectrum.

This isn't just headline anxiety anymore—the tape is breaking, and markets are starting to price in real-world consequences. Welcome to the early innings of the trade war tape bomb era

Today served as a sharp reminder that despite the recent bounce in equities, the coast is far from clear. Sure, some corners of the market were enamoured by whispers that the upcoming White House tariff package will be narrower and more “calibrated” than Trump’s earlier hardline chest-thumping—but let’s not kid ourselves: we haven’t seen the full playbook yet.

The scope, scale, and sequencing of these tariffs remain a moving target, and with no concrete details locked in, markets are still navigating blindfolded. But what’s becoming more apparent on traders’ radar is that next week’s tariff announcement won’t be the final word—it’ll be the opening move in what’s shaping up to be a protracted negotiation slugfest.

Traders are beginning to accept that this won’t be a straightforward binary one-and-done event. The road ahead will be fraught with headline whiplash and macro potholes.

Oil markets

To make matters worse on the inflation front, oil prices pushed higher on Wednesday, fueled by a double shot of bullish catalysts: a larger-than-expected drawdown in U.S. crude and fuel inventories and mounting geopolitical tension as the U.S. threatens to impose tariffs on countries importing Venezuelan crude.

As an oil bear, I’ve got to admit—cheap crude clearly isn’t a priority for the Trump administration right now. We’re now waist-deep in secondary tariff fog, with new layers targeting oil importers from countries Trump has geopolitical scores to settle with—Venezuela imports being the latest in the crosshairs. Sure, Venezuelan barrels don’t dominate global supply, but this move has traders nervously hedging, asking the all-important question: who’s next or what’s next?

Whether that crude is quietly rerouted through backchannels or outright removed from the market will depend on the granularity of implementation. But one thing’s crystal clear: when you stack Venezuela and Iran pressure on top of existing Canadian crude tariffs, you're left with a tightening global oil picture that pulls prices higher by default.

Can OPEC+ reserve releases help ease the squeeze? A bit—but don’t expect a flood, especially while U.S. shale producers continue to sit on their hands, hyper-focused on price discipline over patriotism. This isn't 2018; most shale players have investor mandates, not flags, driving their drilling decisions.

Bottom line: inflation’s getting no favors from the oil complex—tariff threats are doing the heavy lifting, and for now, energy bulls are back in the driver’s seat.

Forex markets

As expected, we’ve seen another wave of long USD capitulation, only to watch the greenback claw back with a classic safe-haven bid, fueled by a market starting to recalibrate inflation and rate cut expectations. With the Fed showing zero inclination to blink and inflation proving stickier than a Fed press conference Q&A, rate-cut wagers are rapidly getting marked-to-reality, and the dollar is flexing its muscles once again.

In USD/JPY, the action is all about the tariff-yield feedback loop. If Trump unleashes a muscle-flexing reciprocal tariff barrage, expect UST yields—especially out the curve—to spike, mechanically hoisting USD/JPY via widening rate differentials and algo-driven flow. The BoJ, still slow-walking policy normalization like it’s 1998, offers little resistance, making USD/JPY an easy candidate for a momentum-driven grind higher.

Over in EUR/USD, the bulls are getting a dose of cold reality. A Washington tariff onslaught, paired with chronic eurozone underperformance, threatens to derail any hope of a near-term bounce. But there’s a twist—fiscal stimulus is finally growing legs, with Berlin leading the charge and others lining up behind. That could help absorb some of the downside shock, keeping EUR/USD supported around the 1.0550–1.0650 zone. Still, don’t forget the ECB wildcard—if Lagarde & Co. pause on rate cuts in April, EUR/USD might just claw its way back toward the 1.09 handle, though it’ll be a choppy, headline-sensitive grind.

Meanwhile, USD/CNY is trading like a coiled spring. The upside risk remains tariff escalation—if Trump turns up the heat on China’s so-called tax distortions and non-tariff hurdles, expect the pair to rip higher in a hurry. But don’t count out the yuan just yet. China’s stimulus machine is humming, and with AI-fueled industrial upgrades and targeted consumption boosts in the pipeline, USD/CNY could stay more resilient than the market is pricing. Watch the real economy prints like a hawk—they’ll be the tipping point between a clean topside breakout or a sharp snapback.

Liquidity drian

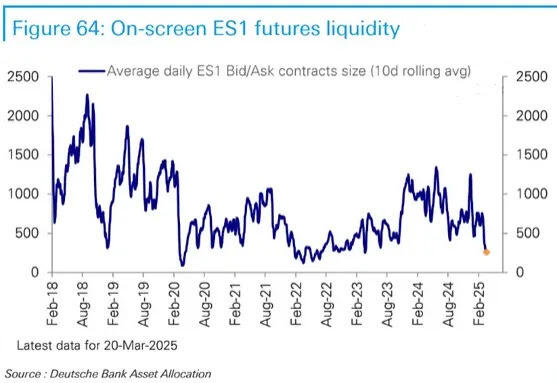

Whether it’s tied to quarter-end flows—which neatly overlap with Japan’s fiscal year-end—or simply a case of risk managers tapping shoulders upstairs, we’re clearly seeing a market that’s getting leaner on risk as trade war anxiety picks up. And nowhere is this more apparent than in US equity liquidity, which has become the canary in the coal mine for how fragile this environment is getting.

Liquidity in S&P 500 index futures, the most actively traded contract, has dropped to a two-year low, according to Deutsche Bank data.

That’s not just academic—it’s the kind of deterioration that changes how every desk approaches execution and risk.

Here’s the first problem: thin books exaggerate price action. A typical institutional-sized order that would normally get absorbed without much fuss is now leaving a footprint. That means even modest selling pressure can create outsized downside tape moves, especially on days like today where the stack was clearly skewed to the sell side.

The second issue? Hedging costs are creeping up. As bid-offer spreads widen, high-frequency market makers are pulling back, and that spells trouble. These players are often the first line of liquidity defense, so when they go into capital preservation mode, transaction costs spike and slippage risk increases.

Bottom line: liquidity is drying up at the worst possible moment, and if tariffs hit harder than expected, we could see air pockets across risk assets, especially in U.S. equities where microstructure fragility is starting to matter again.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.