Strong finish to 2024 overstates strength in industrial production

Summary

The 0.9% pop in industrial production is partly due to a rebound in aircraft production and overstates the current state of the sector. In reality, 2024 was a boring year for manufacturing as high rates and uncertainty hit demand for capex. There's some optimism in the air for 2025.

Manufacturing constrained, but some signs of optimism

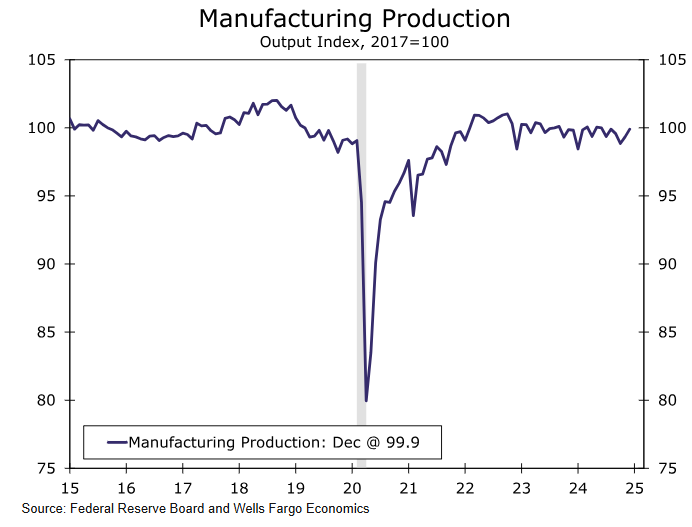

Industrial activity popped to end what was a pretty lackluster year for the sector. Overall production jumped 0.9% in December which marked the fastest monthly gain since February, but that leaves the index up just a half a percent compared to where it stood a year ago.

Production received a lift by all major components in December. Mining output rose 1.8% and utilities production jumped 2.1% on stronger natural gas production. Much of the overall gain can be traced to the largest component, manufacturing output, which rose 0.6% in December on the heels of upwardly revised data for November.

While there were some decent industry gains under the surface, a majority of the strength can be tied to a 6.3% gain in civilian aircraft production reflecting the end to a strike at Boeing. The reality is 2024 was a boring year for manufacturing. The overall manufacturing index finished the year at 99.3, which is precisely where it ended 2023 (chart).

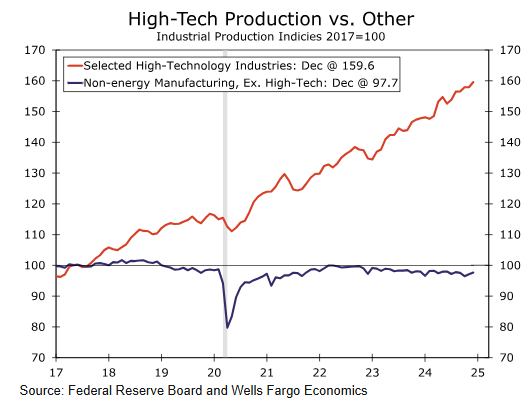

There have been some pockets of strength that have bucked the dull trend, namely in high-tech industries like computer & electronic products and electrical equipment & appliances (chart). A notable offset to broad-based weakness also came from the large chemical industry where production was up 5.4% over the past year.

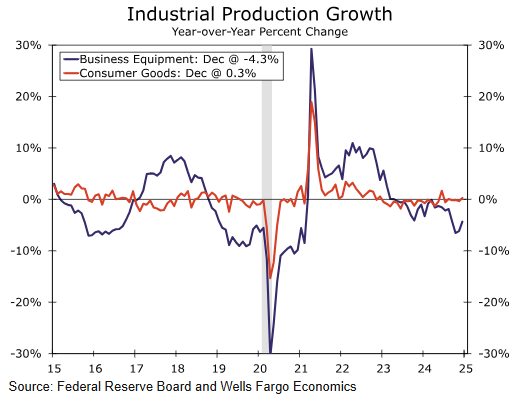

But most industries experienced flat-to-down growth in 2024 with capex demand sapped by less liquidity, high interest rates and most notably continued uncertainty. Although aircraft has pulled down broad business equipment output in recent months, the divergence between business and consumer goods output seen in the nearby chart speaks to current conditions where business investment has flagged despite continued consumer resilience.

Small business sentiment has shifted in the wake of the election amid optimism around deregulation and tax policy generally, but tariffs remain a big asterisk to the outlook. It remains to be seen which tariff policies come to pass and the lack of clarity keeps many businesses in a wait-and-see mode in approaching new capex. This is the sense we're getting from not only the hard data but also from recent ISM manufacturing surveys and from our client discussions, but it remains to be seen to what extent demand conditions pick up this year.

Author

Wells Fargo Research Team

Wells Fargo