Stocks to still extend upswing

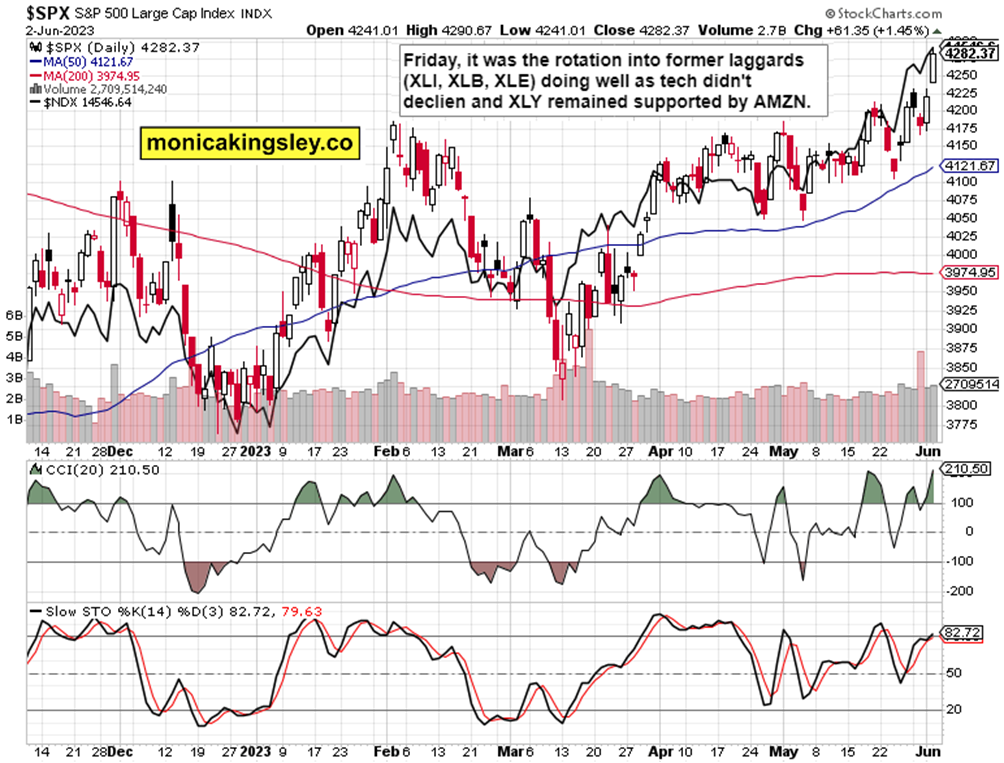

S&P 500 quickly dipped on NFPs, and was eagerly soon bought. Even 4,283 where I expected some resistance, didn‘t last too long. Best of all, it wasn‘t up to tech to do the heavy lifting – the rotations were strong on a daily basis, giving e.g. smallcaps best day in months. Industrials with materials and energy also played their part, making any Friday downswing impossible.

The beginning of next week though shouldn‘t be too easy. USD recovered after the debt ceiling bill relief, making for renewed daily rise in yields. The short end of the curve isn‘t indicating the Fed would cut any time soon (this disconnect in the bond market has to be worked on still, but the 6-m is acknowledging no rate cut as remotely near), and 10-y yield took NFPs as no questions asked proof of the real economy not doing so bad (ignore all prior revisions, incl. in hourly earnings).

Recession is though still coming – unrevised uneployment rose to 3.7% already, and earlier in the week manufacturing PMIs took another turn for the worse. The wealth of recession indicators agree, from M2, housing, forward earnings, bank lending, slowly deteriorating credit quality, but chiefly still declining LEIs and inverted yield curve. Thus far still, it looks to be a mild one, taking unemployment to high 4% values – unemployment or nominal wage pressures won‘t get as bad as during prior downturns.

Market breadth improved a lot on a daily basis, but the whole market remains selective, and in spite of the recent catch up by laggards, and driven by tech (the level of hype isn‘t that bad, but earnings have to play catch up to the elevated valuations, and also the post-debt ceiling deal rotation out of the sector didn‘t yet come even briefly – to be clear, I expect tech FOMO to last a bit longer still), consumer discretionaries (neither AMZN nor TSLA are badly overextended), and communications (META is the prime correction candidate rather than NFLX), and NVDA is in a FOMO and valuation category of its own.

Sure that Treasury replenishing its TGA is a negative, but much depends where that bid for fresh Treasuries comes from. If from retail buyers liquidating deposits, then it‘s 100% bearish impact – if from banks drawing down reverse repos, then it‘s neutral. All in all, the net effect is going to be negative over the nearest months, but not nearly as negative as feared – look at the Chicago Financial Conditions Index only slowly rising, and as complacent as VIX.

So, there is still more ES upside, and I don‘t want to call for shorts and be forced to hold them just because the overwhelming majority of technical signs favor that (such as extremely poor financials‘ performance) the way I had done with the latest unhappy medium-term short – regardless of the great number of daily bullish calls outnumbering the bearish ones for that trade‘s duration, or the reassessments before the debt ceiling deal or as a minimum hedge call right after its announcement.

While this created a rare situation of my swing trades not having the latest one as a truly swing one, I‘ve reflected the situation of not all of you heeding / being practically able to take advantage of all the good calls given in the daily articles and Twitter / Telegram – I‘ll solve this by adding Monica‘s Intraday Ssignals to the existing line-up of services, which would focus on intraday ES trade calls with much real-time commentary. It‘ll be about tight trade parameters with focus on high confidence setups, giving 2-4 entry - stop-loss - take profit signals (day orders) per week on average on top of commentary powering your own decisions - delivered via Telegram (closed group). Current premium clients and those who left me during this long short, can get free subscription upon mailing me, if interested – details are both on my site and on my Patreon site. All future subscribers to premium daily analyses will get intraday signals on extra advantageous terms. You can tell me already now what you think – I‘ll be grateful for that, my purpose is to serve you better. Let‘s make up for whatever we all lost – and if you were following the daily calls / tweaking them to your ends, let‘s broaden our arsenal!

Keep enjoying the lively Twitter feed via keeping my tab open at all times (notifications on aren't enough) – combine with Telegram that always delivers my extra intraday calls (head off to Twitter to talk to me there), but getting the key daily analytics right into your mailbox is the bedrock.

So, make sure you‘re signed up for the free newsletter and make use of both Twitter and Telegram - benefit and find out why I'm the most blocked market analyst and trader on Twitter.

Let‘s move right into the charts – today‘s full scale article contains 6 of them.

S&P 500 and Nasdaq outlook

Time for decreasing momentum and consolidation of Friday‘s sharp gains – not yet a turnaround lower, but 4,283 test before heading for the 4,305 resistance (looking for increasingly active sellers there), with 4,335 being the ultimate test of this long advance off Oct lows on overall troubled breadth.

Gold, Silver and miners

Gold and silver acted weaker than they should on Friday, but I‘m still not looking for breach of gold $1,930 – $1,950 , or silver $23.15 (I had to update the silver zone of $23.15 - $23.40 to its lower border only thanks to copper weakness).

Crude Oil

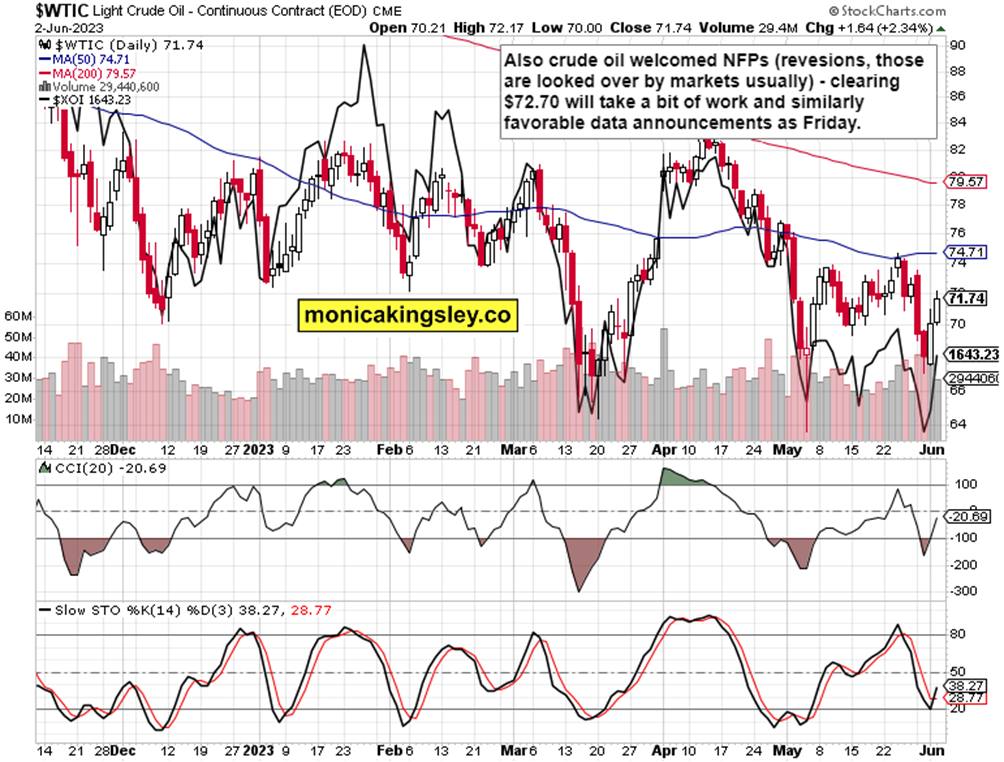

Crude recovery needs to continue, taking it above $72.70 decisively – it won‘t be easy as the upside momentum could have been stronger following NFPs lifting up everything in sight.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.