Sticky UK services inflation to come lower in 2025

Services inflation is stuck at 5% and will stay around there for the next few months. But further progress, helped by more benign annual rises in index-linked prices in April, should see ‘core services’ inflation fall materially in the spring. We think that will be the catalyst for the Bank of England to cut rates a little faster than markets now expect.

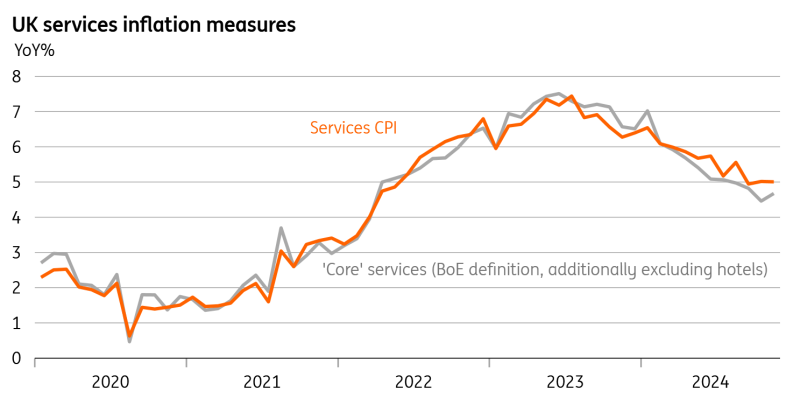

UK services inflation is stuck. That’s the main takeaway from the latest UK data, even if it was a tad better than most had expected.

Services CPI stayed at 5.0% for the second consecutive month, though only because of a particularly steep fall in air fares. Once we strip that and other volatile categories out, our measures of so-called “core services” inflation ticked higher.

Indeed our favoured measure, which strips out rents and hotel prices amongst other things, ticked up from 4.5% to 4.7%, having generally been performing better than the headline numbers over recent months.

All of this is really just noise. And in fact, services inflation was still a tad higher than the Bank of England’s most recent forecast, even if it was below everyone else's. Bigger picture, we expect it to bounce around 5% for the next four months or so.

Again though, most of that projected stickiness is likely to be concentrated in categories that the Bank of England has told us it is inclined to pay less attention to. Our core services measure described earlier is likely to get pretty close to 3% next spring.

'Core services' is set to fall close in on 3% in the spring

Source: Macrobond, ING calculations

A lot of the services basket is affected by one-off annual changes in index-linked prices – think of things like phone and internet bills. These are often tied to past rates of headline inflation which, through 2024, has been pretty benign. Those annual price hikes for various services should therefore be less aggressive next April than we saw earlier this year.

If we’re right about that, it should also help overall core inflation to fall materially below 3% in the spring (from 3.5% today). Headline CPI is set to stay a little stickier at 2.6-2.7% in the near-term, thanks to less favourable energy base effects.

If 'core services' inflation does look steadily better, then that would provide some ammunition for the Bank of England to move a little faster on rate cuts than markets are now pricing. Our base case is for back-to-back to rate cuts from February onwards, with Bank Rate falling to 3.25% later in the year.

For the time being though, today’s data means the Bank will stay the course at this week’s meeting. It’ll keep rates on hold and offer no major hints on what’ll come next, beyond re-affirming its commitment to gradual cuts.

Read the original analysis: Sticky UK services inflation to come lower in 2025

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.