S&P Global Manufacturing and Services PMI: Inflation behind the veil

- Manufacturing and Service sectors expected to maintain expansion.

- US economy continues to grow despite inflation headwinds.

- GDP forecast to drop sharply in the first quarter.

- Markets monitoring PMI for signs of economic weakness.

Business attitudes have remained upbeat in the US even as inflation takes an ever bigger bite of consumer income and economic growth is expected to plummet in the first quarter.

The S&P Global Manufacturing Purchasing Managers Index (PMI) may dip to 58.2 in March from 58.8 and the Services Index should be unchanged at 58.0. The Global Composite PMI is forecast to edge up to 58.1 in March from 57.7 prior. Readings over 50 denote expansion.

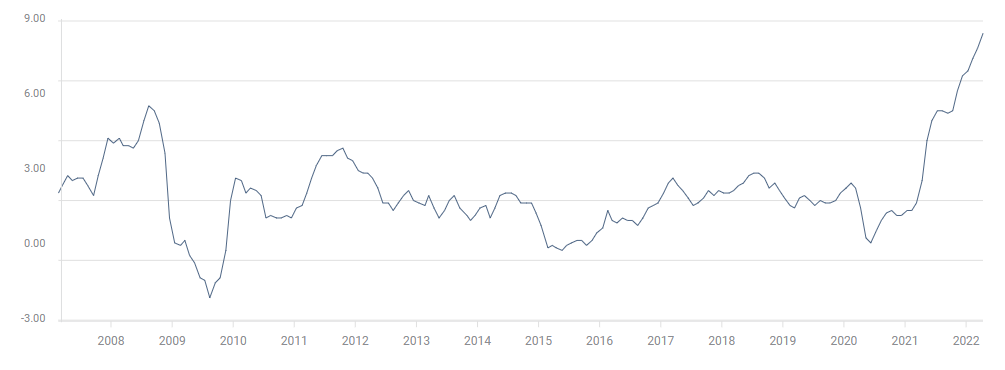

Consumer inflation in the US reached a four-decade high at 8.5% in March, far outstripping income gains and reducing purchasing power by 2.7% over the previous year. Real wages, compensation minus inflation, have fallen for 12 straight months as the Consumer Price Index has more than tripled from 2.6% last March.

CPI

The US economy expanded at a 6.9% annualized rate in the final three months of last year. Gross Domestic Product (GDP) averaged 5.6% in 2021, a vast improvement over the lockdown ravaged 0.5% in 2020. That rapid expansion may have come to a shuddering halt in the first quarter with growth forecast to be near 1%. The Atlanta Fed GDPNow Model predicts 1.3%, the Reuters poll of economists posits 1.0%. First quarter GDP figures will be released on April 28.

Purchasing managers' indexes and the business attitudes they chart have been strong over the last six months, supported by good though volatile economic statistics.

Positive US data

The labor market has reported excellent results over the past six months. Nonfarm Payrolls have averaged 600,000 new positions a month for the last half-year and the Job Opening and Labor Turnover Survey (JOLTS) has sustained more than 11 million offered jobs for the same period, a record. Four weeks of Initial Jobless Claims averaged 172,250 on April 8, just shy of the all-time low of 170,250 the week before.

JOLTS

Retail Sales have increased 0.95% a month since September. The holiday season, October, November and December was disappointing with sales falling 0.5% each month but January’s 4.9% surge restored the balance, followed by 0.8% in February and 0.5% in March.

Finally, New Order PMIs from the Institute for Supply Management have averaged 62.9 for the service sector and 59.4 in manufacturing for six months. Orders have weakened appreciably over the period with manufacturing’s 53.8 reading in March, the lowest since May 2020.

Manufacturing New Orders PMI

FXStreet

Negative US data

Inflation and its prospective drag on consumer spending is the chief concern. As noted above real wages have been declining for a year. Consumption has not fallen because families are drawing on savings to make up the difference, this cannot continue indefinitely.

Overall CPI, 8.5% in March, has set a new 40-year high for each of the last four months. This will probably accelerate in the second quarter as business price increases have reached double digits, with the Producer Price Index (PPI) soaring an all-time record 11.2% on the year in March. In the current product and labor scarce economy, manufacturers and businesses will not hesitate to pass cost increases on to their customers.

CPI

FXStreet

Federal Reserve rate policy is another building impediment to business expansion. The Fed’s own March estimates have the fed funds rate at 1.9% at the end of the year, 150 basis points higher than its current 0.5%. Treasury futures rate the odds of a 3.0% fed funds rate after the December 14 FOMC meeting at just over 50%. The commercially relevant 10-year Treasury yield has jumped 133 basis points this year to 2.834% and is now at the high end of its 10-year range.

10-year Treasury yield

CNBC

Markets conclusion

Despite the gathering inflation threat to consumption and its 70% contribution to US economic activity, American consumers have not, as yet, pulled back on spending. That reality is reflected in the relatively robust PMI readings. Orders are still flowing into firms in healthy, if somewhat reduced volumes and as long as that continues, the business outlook will remain optimistic.

The PMI scores are normally seen as one of the earliest indicators of economic direction. If the March levels are weaker than expected, especially if they approach or cross the 50 mark, markets will notice. Treasury rates and the dollar will fall and equities will begin to worry about an economic slowdown. If PMI results are at or better than expected, it will just put off the economic worries until another day. Inflation will be the bugbear for many a day to come.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.