South Korea: Recovery from recession will only come later in the year

Despite an anaemic start to 2023, we expect conditions to improve in the second half of the year as global demand begins to pick up and the deleveraging cycle comes to an end.

South Korea: At a glance

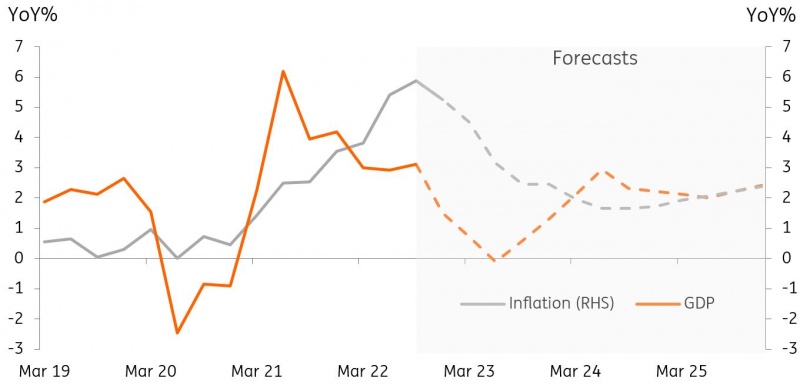

South Korea's economy has deteriorated considerably since the start of the fourth quarter of 2022, with exports, manufacturing and service activity tumbling sharply. Consequently, we believe that fourth-quarter GDP will contract. With such an anaemic start to 2023, we expect the annual growth rate for Korea to decelerate to only 0.6% year-on-year in 2023 from 2.6% in 2022. Both external and domestic demand is likely to weaken further, especially in the first half of 2023, and painful deleveraging is expected to hurt short-term growth given high levels of private sector debt.

Inflation has clearly peaked and inflation expectations have fallen to around 3% and are expected to decelerate further. The accumulated pressure to raise utility and public service fees will add upward inflationary pressures, but most of these are expected to be offset by falling housing prices, global oil prices, and a stronger Korean won. Due to asset price adjustment and the higher debt service burden, the Bank of Korea (BoK) is likely to respond with a rate cut in the second half of 2023.

GDP and inflation outlooks

Source: CEIC, ING estimates

Three calls for 2023

1. Deleveraging will be painful

House prices have already declined significantly in 2022, but we expect prices to fall by another 10% in 2023 and remain stagnant throughout the year. Given the sharp rise in unsold units in major cities, it may take a while for the recovery to take hold in the residential housing market. The government will continue to soften real estate measures and lending conditions, but higher interest rates will not enable home buyers to return to the housing market quickly. Historically it usually takes two to three years to complete a downcycle. Deleveraging for corporates is also likely, and construction and real estate developers will suffer the most. The financial crunch in the corporate debt market has now subsided due to the government's response, but it is expected to come back to the surface as corporate bond issuance increases at the beginning of the year and high interest rates continue.

2. Exports to lead a recovery in the second half of the year

Despite the poor export performance in the fourth quarter of 2022, annual exports grew 6.1% year-on-year in 2022. However, in 2023 we expect exports to decline by about -7.0%, given the weakness of global demand and unfavourable price effects. We believe the downcycle for semiconductors will continue until the third quarter of 2023 and China's reopening could add a negative impact on Korea's exports in the first half of 2023, with a surge of Covid-19 patients, the risk of new variants, and supply chain disruptions. However, we expect exports to rebound quite meaningfully in the latter part of the year with the US and EU's economy bottoming out and China's situation normalising, which should lead the overall GDP growth in the second half of 2023.

3. The Bank of Korea to turn dovish as inflation subsides

We expect the terminal interest rate to peak at 3.50% and the Bank of Korea to enter an easing cycle in the third quarter of 2023. Given that the current policy rate is at 3.25%, our call for an additional 25bp hike in February will be the final destination for the current tightening cycle. Despite a reduction in gasoline tax subsidies and higher public service charges, base effects will anchor headline CPI to around 4% in the first quarter of 2023. We expect the Bank of Korea to maintain its hawkish stance throughout the first half of 2023 as inflation is still likely to far exceed its 2% target, and uncertainties over utility bill hikes and the resulting secondary effects from these are still high. But, as the real economic activity contracts and deleveraging continues, the BoK's policy priority is expected to shift toward supporting growth.

South Korea forecast summary table

Source: CEIC, ING estimates

Read the original analysis: South Korea: Recovery from recession will only come later in the year

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.