Some early signs of stabilization in September Durable Goods

Summary

Once you cut through the aircraft-related volatility in durable goods, the environment reveals demand conditions may be beginning to stabilize. With the direction in rates now clearly lower and the U.S. presidential election soon behind us, businesses may soon have the certainty they need to support capital investment.

Clear the air

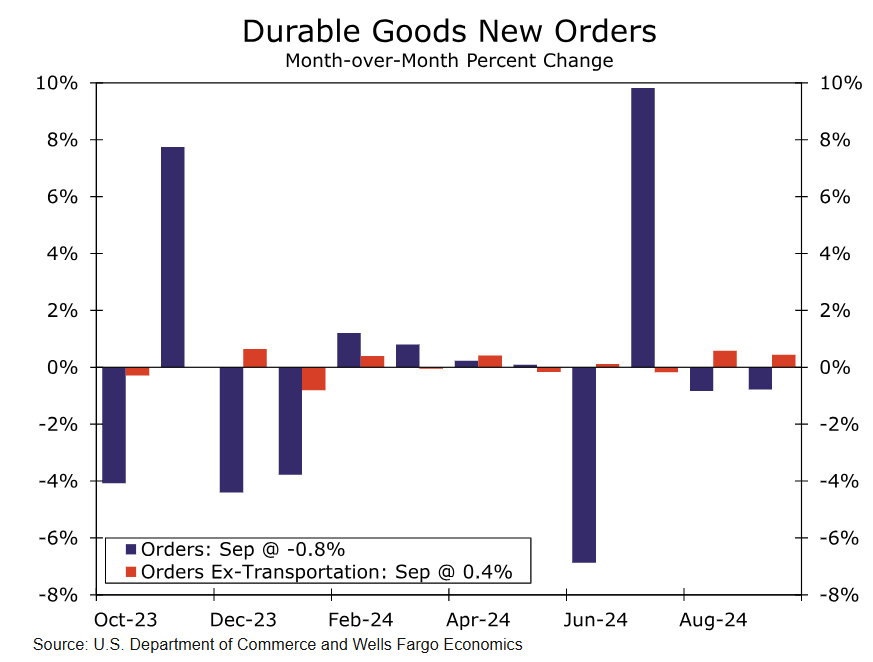

Demand for durable goods remains weak. That's at least the first takeaway from the September data. New orders for durables dropped 0.8% in September and downward revisions to past data turned a flat August reading negative to match the September decline (chart). Yet the only thing more true than constrained capex-demand is the data remain as volatile as ever.

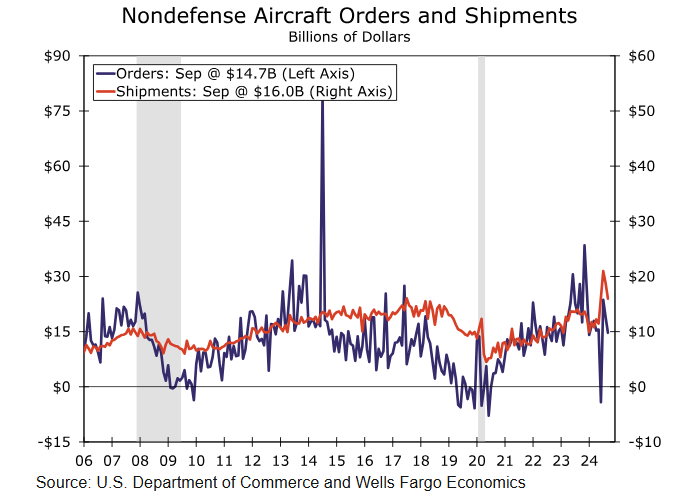

Consider the past two drops come after a 9.8% surge in new orders in July and 6.9% plunge in June. And who, you may ask, is the culprit for all of this volatility? Aircraft (chart). Nondefense aircraft orders are notoriously volatile, and once we strip the broad transportation sector from the data, orders have been more steady in recent months. In fact, orders excluding transportation have risen the past two months.

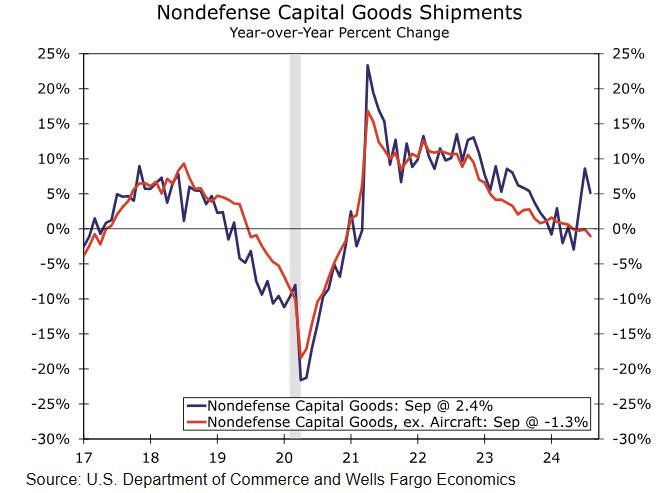

Stripping aircraft orders from the estimates reveals a slightly more steady environment for durables activity in recent months, a positive sign for budding demand. But when we think of the broad capex spending, aircraft matters. Nondefense capital goods shipments, a proxy for broad business investment, slipped 3.6% in September, and is up 2.5% over the past year (chart). That suggests some modest downside risk to our estimate for real equipment investment to rise north of an 11% annualized pace in Q3. But, a solid end to Q2 and start to the third quarter still positions for a decent pace of equipment investment during the quarter. We'll get the Q3 GDP report on Thursday.

The worker strike at Boeing that started mid-month and the hurricanes that hit the country in September could also be negatively impacting the data. But in looking beyond the volatility, the more steady outturn in orders when stripping out transportation is a good sign that demand conditions may be beginning to stabilize.

With interest rates finally coming down, we expect to see capital spending budgets favor durables spending as some equipment is in need of new investment. Durable goods last for many years, but they do not last forever. While monetary policy acts with a lag, the direction of rates is now clearly lower and with the U.S. presidential election soon behind us, businesses may soon walk into a clearer environment more supportive of capex investment.

Author

Wells Fargo Research Team

Wells Fargo