September flashlight for the FOMC blackout period – Let the easing begin

Summary

Data released since the last FOMC meeting on July 31 make a compelling case for the Committee to begin easing the stance of monetary policy at its upcoming meeting on September 18. Inflation remains a bit above the Fed's target of 2%, but momentum in consumer prices clearly is slowing. Meanwhile, the labor market, the other half of the Fed's dual mandate, has softened.

As stated by Fed Chair Jerome Powell, "the time has come for policy to adjust." The only question is the magnitude of the rate cut on September 18. Will the FOMC cut rates by 25 bps or sanction a 50 bps reduction?

We expect the Committee will cut rates by 25 bps at the September 18 meeting based on recent remarks from Fed officials indicating that most favor a go-slow approach at this juncture. That said, some notable Fed officials, including FOMC Chair Powell and Vice Chair Williams, have refrained from commenting on how large a reduction may be warranted in the near term, keeping the door open to a larger cut in September. Therefore, we would not be totally surprised if the FOMC opted for a 50 bps rate cut instead.

We look for the median dot in the dot plot to shift down by 50 bps to 4.625% for year-end 2024, indicating the median participant thinks another 50 bps of rate cuts after the September meeting will be appropriate by the end of the year. For 2025, we expect the median dot to fall to 3.375%, implying 125 bps of additional easing next year.

We think that the run of 17 consecutive FOMC meetings without a dissent may be broken at this meeting. If, as we expect, the FOMC cuts rates by 25 bps, then we can envision more dovish voting members of the Committee potentially dissenting in favor of a larger reduction. Conversely, if the FOMC opts for a 50 bps rate cut, then hawkish voting members could dissent, preferring a 25 bps rate reduction instead.

"The time has come for policy to adjust"

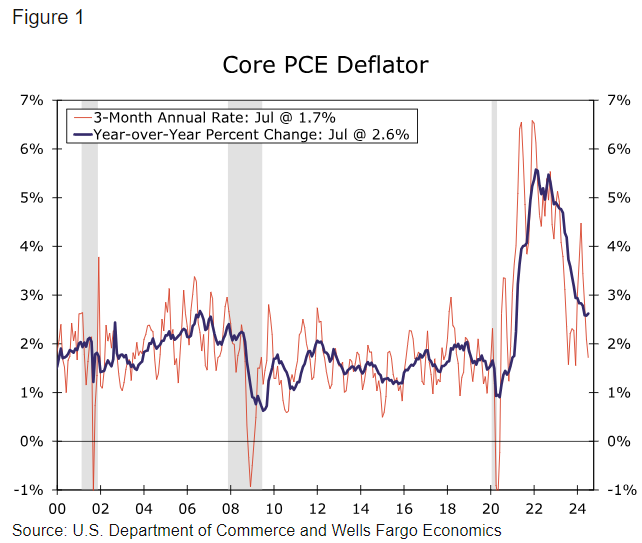

Data released since the last FOMC meeting on July 31 make a compelling case for the Committee to begin cutting the federal funds rate at its upcoming meeting on September 18. For starters, inflationary pressures continue to subside. Although the year-over-year change in the core PCE price index, which Fed policymakers believe is the best measure of the underlying rate of consumer price inflation, remains above the central bank's target of 2%, momentum in consumer prices is slowing. The index rose at an annualized rate of only 1.7% between April and July, down sharply from the 4.5% annualized rate of change that was registered between December and March (Figure 1). In short, the FOMC has made additional progress recently in fulfilling the "stable prices" component of its dual mandate.

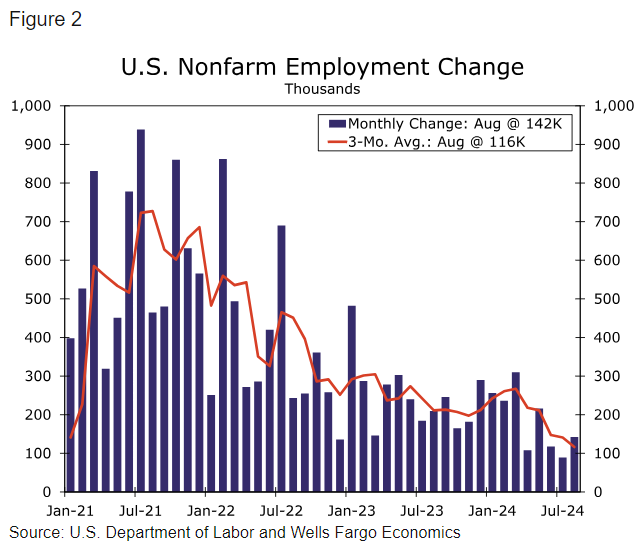

Turning to the other side of the dual mandate, the risks to "maximum employment" are rising. Although payrolls rebounded in August with a 142K monthly gain, up from only 89K in July, the underlying pace of job creation clearly has downshifted. Whereas payrolls rose at an average monthly pace of 207K in the first half of the year, the economy created only 116K jobs per month on average between June and August (Figure 2). Furthermore, the unemployment rate has trended up from 3.7% at the turn of the year to 4.2% in August. Softening in labor market conditions should help to put downward pressure on wage gains, thereby leading to further price growth moderation in coming months. In that regard, average hourly earnings were up 3.8% on a year-ago basis in August, which represents a significant slowing from the 5.9% increase that was registered in March 2022.

Author

Wells Fargo Research Team

Wells Fargo