Sense of reality

S&P 500 finished Friday on a weak note – gloomy string of tightening news from around the world, disappointing the markets and dialing back risk sentiment considerably. Coupled with the real economy hits – retreating LEIs, retail sales starting in my view a subdued period, manufacturing and housing in full retreat mode, and layoffs rising.

There have been even reports from Philadelphia Fed to the effect of NFPs data projecting a false picture of strength – yes, the differential between Establishment and Household surveys continues to widen, now standing at 2.7 million jobs (Nov 2022), be it thanks to full time, part time or multiple job holders, or the birth-death model. For all the labor market tightness, and the categories seeing gains (sectorally not representing a picture of strength, but rather teetering on the brink of recession), the Fed is in my view relying on a deceptive picture of strength in the job market when the opposite is slowly becoming the truth,

You can liken it to the tightening effects, where I come in the 12 months time frame to see them play out rather than 6 only. And if you look at where the 2-year yield is, and where the Fed funds rate is, the message is clear – things are starting to break in the real economy, and the Fed would better wait and see here.

Instead, we‘re likely to get 25bp Jan and Mar hikes, taking the Fed funds rate to 5.00% - and the Fed thinks about a restrictive territory of 5.50% later in 2023, provided that (household) inflation expectations are cooperating. The focus is to avoid the 1970s mistake of letting inflation expectations become unanchored... while looking at the lagging indicator of CPI and its core as well.

And so are thinking other key central banks – ECB, BoE and SNB – not just hiking rates, but continuing shrinking the balance sheet. All done at the same time when the Treasury needs to step up debt issuance in Q1 2023, contributing to mopping up liquidity from the system. Are banks likely to withdraw reserves held at the Fed and deploy in the real economy (credit multiplier aka making money go round through the fractional reserve system multiplier) when the evidence of slowdown as kicking in (NBER has already ruled that those two negative quarters earlier in 2022, aren‘t a recession, and the Q3 figure was indeed good), dragging down earnings estimates and outlook?

Who‘s going to buy the fresh debt when reliable foreigners are withdrawing the bid, too? Squeezed profit margins are to reflect on P/E multiples – and we‘re back at the many disconnects in the labor market.

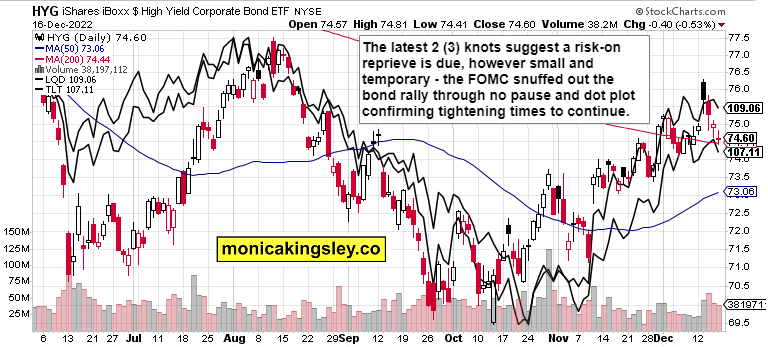

Even credit markets tell the same story – and the rally or at least stabilization in bonds would have been a necessary ingredient of this Q4 bear market rally as much as that of the summer one – the U.S. was leading the world for German bonds or UK guilts haven‘t rallied as far as Treasuries did. The march to higher yields, is on, that‘s the big picture view.

The key questions now are the shape of the U.S. consumer in Q1 2023 – if retail sales show the latest reading was only a blip, there needn‘t be a significant Q1 S&P 500 correction. Stocks would instead decline thereafter. Or the tightening (including $90bn a month in balance sheet shrinking) forces some shoe to drop in 1H 2023 – watch for Fed swaps and credit default swaps to reveal the stress.

I‘ll be discussing the individual market effects within the chart section.

In all likelihood, this is my last extensive daily analysis of 2022 – unfortunately I‘ll have to limit analytical coverage and Twitter activities will over the coming two days, and these will be absent in the following week. Very much looking forward for returning to the usual frequency, scope and presence as of Jan 02, 2023! Thank you for your patience, and have blessed days ahead!

Keep enjoying the lively Twitter feed serving you all already in, which comes on top of getting the key daily analytics right into your mailbox. Plenty gets addressed there, but the analyses (whether short or long format, depending on market action) over email are the bedrock. So, make sure you‘re signed up for the free newsletter and that you have my Twitter profile open with notifications on so as not to miss a thing, and to benefit from extra intraday calls.

Let‘s move right into the charts.

S&P 500 and Nasdaq outlook

The higher volume can be chalked down to options expiry, and doesn‘t necessarily represent an upcoming (strong) rebound, even though we‘re likely to reflexively move up today. Even prints below 3,905-3,910 will probably provide resistance today, before to the surprise of many – we can have a relatively good part of Jan as I‘m not looking for the Santa Claus rally to come anymore.

Credit markets

TLT is hanging in there, but needs time to drif lower, while HYG can surprise in the short term. I‘m looking for these moves to determine the stock market direction next week, together with the dollar (not on a relief rally yet).

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.