Russia and Ukraine threaten the global recovery as central banks confront inflation

Ukraine and inflation are the twin poles of market concern. A Russian invasion of Ukraine would upend the world's economy, sending oil and commodities soaring, with a good chance of precipitating a recession. The Federal Reserve's aggressive inflation campaign and those of the Bank of England, the Bank of Canada, and perhaps the European Central Bank, require a benign political environment. Russia and Vladimir Putin have a de facto veto on Western monetary policy. Join FXStreet senior analysts, Yohay Elam, Eren Sengezer, and Joseph Trevisani for an examination of the policy linkage between Kyiv, Moscow, and Washington.

Joseph Trevisani: Yes, the CME FedWatch tool has been very skittish...on Tuesday it was 57.9% for a half-point hike... today it's 32.7%. That is a lot of indecision. Putin seems to be running the Ukraine show, with Europe and the US just responding.

Yohay Elam: On the one hand, the FOMC meeting minutes document a meeting that was held before the latest steaming-hot jobs, inflation, and retail sales figures, and that may explain their relative dovishness. On the other hand, the publication is edited until the last moment.

Joseph Trevisani: Exactly, though my guess is any decision on the hike is weeks away.

Yohay Elam: There is logic in raising rates relatively quickly and then taking a pause to see how markets react, if inflation eases, etc. That would be dollar bullish now, bearish later.

Eren Sengezer: Yields are lower due to risk aversion and that's why the CME Group's FedWatch Tool's 50 bps March rate hike probability is skittish as Joseph put it in my opinion.

Joseph Trevisani: I agree, US debt is the investment of choice. I don't think the Fed is concerned about growth, especially after Retail Sales and NFP, still the Atlanta Fed GDPNow current estimate is only 1.5% for Q1.

Yohay Elam: The dollar is the king of cash and US debt is the investment of choice.

Joseph Trevisani: And with the fast retreat of most Covid measures and remaining restrictions the economy should thrive.

Yohay Elam: The hard data show the US economy is on fire, NFP, retail sales, and unfortunately also inflation.

Eren Sengezer: The only obstacle before the US economy is inflation as it stands.

Yohay Elam: Yep, more room for growth in Q1.

Joseph Trevisani: Yes, Sales are not corrected for inflation so some portion of the 3.8% January increase is just higher prices.

Yohay Elam: Inflation hurts what shoppers say, low consumer sentiment, but not what they do, shopping en masse.

Eren Sengezer: Consumer spending does look healthy but rising prices seem to have played a part in January sales data beating estimates.

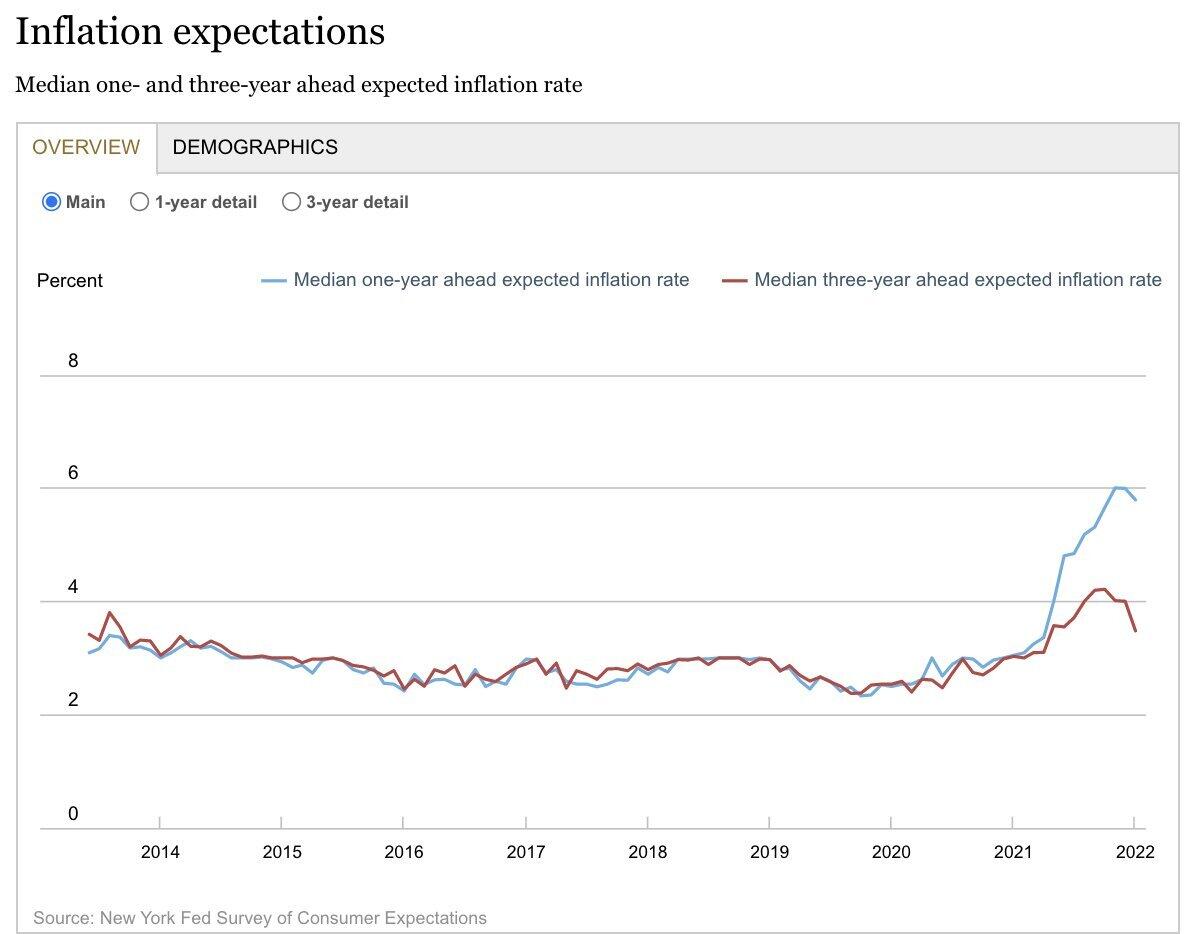

Joseph Trevisani: Yes but it skews purchases, if gasoline is $3.79 a gallon, which is what I paid yesterday, there is less money for optional purchases. It doesn't show up in Sales because the total is what we see. The NY Fed inflation expectations was 6% at one year. That is an uncomfortable place for the Fed.

Yohay Elam: The Control Group surged by 4.8%.

Joseph Trevisani: I think there is still a lot of spending catch-up to do. I know it is true in my family.

Yohay Elam: NY Fed inflation expectations show prices are set to rise this year and fall afterward. Momentum from the recovery continues, but it will fade later on. Less catch-up, less impact of stimulus.

Joseph Trevisani: Three year is 3.5%.

Yohay Elam: 3.5% is high, but not 6%, and falling from higher levels. Hopefully a downtrend.

Joseph Trevisani: The 1-year has dropped to 5.8% in January from 6% in December which is the first decline since June 2020.

Yohay Elam: I think Powell will un-retire the "T word" sometime in the summer.

Joseph Trevisani: He might, but with elections in full swing, he may be wary of entering that fray. Inflation is sure to be a major topic in the November elections.

Eren Sengezer: How many rate hikes do you think the Fed would have to do before the "T word"?

Yohay Elam: Yeah, Powell is under political pressure to fight inflation, and he will likely stick to "fulfilling our mandate" comments. I would say four hikes.

Joseph Trevisani: I agree I think four hikes. The March FOMC will issue updated projections.

Yohay Elam: It's going to be a big decision undoubtedly.

Eren Sengezer: I also think four rate hikes sounds plausible but I feel like the Fed will adopt a wait-and-see mode afterwards.

Yohay Elam: Where do you both see the dollar going?

Joseph Trevisani: To get the easiest prediction out of the way first, if Russia invades Ukraine, the dollar rises on safety.

Eren Sengezer: I think the dollar is likely to hold its ground or even gather some strength in the first half of the year. It's likely to continue to find demand as safe-haven as Joseph mentioned and I also think that the Fed still could turn more hawkish than markets are currently expecting. Having said that, it could reverse its gains in the second half of the year in case the Fed takes a step back ahead of the mid-term elections and to see how things evolve before deciding on what to do next.

Joseph Trevisani: A good portion of the Fed's current hawkishness is priced in. this is the Dollar Index from last March.

Eren Sengezer: Do you think the Fed could turn even more hawkish?

Joseph Trevisani: The Canadian and UK central banks will be hiking along with the Fed. The ECB perhaps. Since mid-November, we have been range trading, with some good volatility. Markets are wary.

Yohay Elam: Maybe a hawkish Fed is already well in the price, which suggests a "buy the rumor, sell the fact" response if the Fed's March dot-plot is not extremely hawkish.

Joseph Trevisani: I don't think the Fed goes beyond 4 hikes. That is every other meeting beginning in March.

Yohay Elam: And some commercial banks suggest a hike every meeting. So, markets have gotten ahead of themselves?

Joseph Trevisani: The Treasury market is not fully capturing the potential because of Ukraine.

Yohay Elam: Yeah, it's been a week or more that geopolitics overshadow the Fed.

Joseph Trevisani: On Ukraine, I think Putin is playing an astute game setting up a trade of military de-escalation, which he created, for a substantive concession from Europe and the US.

Yohay Elam: So far, NATO is holding up, but economic interests vary across the continent. In March, the ground melts and it would be harder for Russia to roll into Ukraine with tanks. Also, European demand for gas wanes.

Joseph Trevisani: Germany gets I think 30% of here energy from Russia. The elimination of her nuclear plants is looking rather short-sighted.

Yohay Elam: Yeah, that was a huge mistake by Merkel in 2011. Germany eventually burned more coal and increased its dependency on Russian gas.

Joseph Trevisani: Macron has said France, which has always been given to nuclear, will expand its capacity. Exactly!

Yohay Elam: Yeah, Germany and France are not Italy nor Japan, nor California – they are less prone to earthquakes.

Joseph Trevisani: Markets are not showing a large reaction to Ukraine, then again nothing has really happened.

Eren Sengezer: Gold seems to have recaptured its safe-haven status.

Yohay Elam: I think reactions in gold are indirectly related to safe-haven flows but rather to the rush into bonds and the drop in yields.

Eren Sengezer: Yields and gold have a strong inverse correlation in times like these, I agree. It's difficult to assess whether there is causation though in my opinion.

Joseph Trevisani: Gold has been stronger since the end of January but there has been no real trend, just several spikes, reversed when the catalyst fades.

Eren Sengezer: I still think a Russian invasion could lift gold above $1,900 and allow it to stay there. A de-escalation of the situation is likely to trigger a deep correction alongside recovering yields.

Joseph Trevisani: Agreed. Will Russia invade? I doubt it.

Eren Sengezer: It's difficult to say really.

Joseph Trevisani: Military actions rarely end as expected and it is far harder to extricate once begun.

Yohay Elam: They want a compliant regime like in Belarus.

Joseph Trevisani: Russia's neighbors want to belong to NATO for an obvious reason, history.

Yohay Elam: Ukraine and Russia had a rough 20th century.

Joseph Trevisani: An understatement. But then Europe had a lousy century. Markets are not really showing great alarm at the current pass in Ukraine.

Joseph Trevisani: Let's assume Ukraine peters out in a series of agreements. If so, absent a new pandemic, the global recovery should rev up.

Eren Sengezer: What's the other scenario? Can a prolonged conflict between Russia and Ukraine derail the global economy?

Joseph Trevisani: I think it would precipitate a global recession. Where would crude land if Russia invades? $120 $140? I think markets are clearly betting on a negotiated settlement.

Eren Sengezer: I agree markets are downplaying the possibility of an invasion, and they may be right. If oil price

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

FXStreet Team

FXStreet