Remember inflation? July CPI preview

Summary

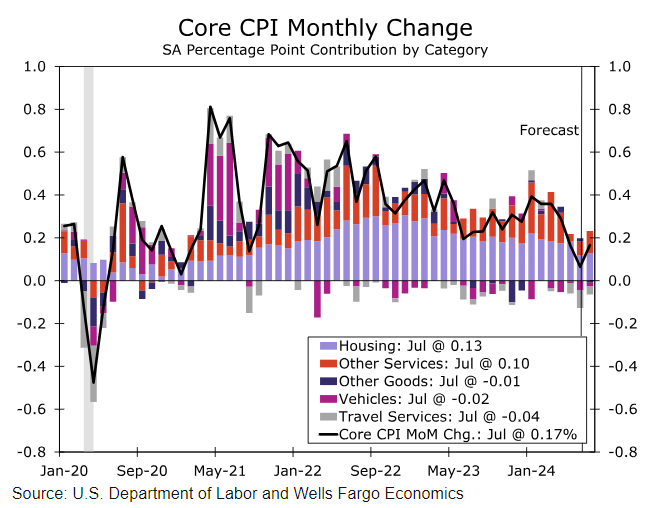

The July CPI report is likely to further the case that inflation is quieting down even if it has not yet returned all the way back to the Fed's target. We look for headline CPI to have advanced 0.2% in July, which would keep the year-over-year rate steady at more than a three-year low of 3.0%. The core CPI also looks set to advance 0.2% in July amid a rebound in some of the more volatile "super core" components. However, we expect the step-down in shelter inflation from the first five months of the year to be sustained and for prices among core goods to continue to decline outright. If realized, the 12-month change in the core CPI would fall to a fresh cycle low of 3.2%.

Looking beyond July, we expect inflation to continue to subside. Labor costs are no longer a meaningful threat to the Fed's 2% inflation target, as growth in the labor force has coincided with fading demand for workers. Meantime, downward pressure on price growth from weakening consumer demand is mounting and driving inflation for discretionary items back to its 2019 pace. While the year-over-year rate of core PCE inflation is likely to remain stuck around its current rate through the end of the year, the annualized pace of inflation looks set to ease back in-line with the FOMC's target. Amid increasingly worrisome conditions in the labor market, we expect the Fed to consider inflation is close enough to its target and embark on a rate cutting cycle at its next meeting.

July CPI poised for another tame increase

Weakening in the jobs market may have finally stolen the spotlight from inflation, but the extent to which the FOMC reacts to the dimming labor picture depends in part on how price data unfold from here. The past two months of inflation prints have shown that the downward trend in price growth is back on track after the first quarter's derailment. The July CPI report is likely to further the case that inflation is quieting down even if it has not yet returned to the Fed's target.

We estimate headline CPI rose 0.2% in July, which would keep the 12-month change steady at a more than a three-year low of 3.0%. Although gasoline prices rose a little over 1% during the month, grocery store prices were likely little changed amid more stable input prices and rising promotional activity.

Excluding food and energy, we also look for a tame 0.2% increase, even as that would mark a slight pickup relative to June (Figure 1). If realized, the year-over-year rate of core inflation would edge down to 3.2%, with the three-month annualized rate of 1.6% pointing to a further moderation in the 12-month change ahead. Goods prices are likely to decline another 0.1% in July. However, there are tentative signs that outside of autos, goods deflation is losing steam, with the year-over-year rate of "other" core goods starting to turn higher.

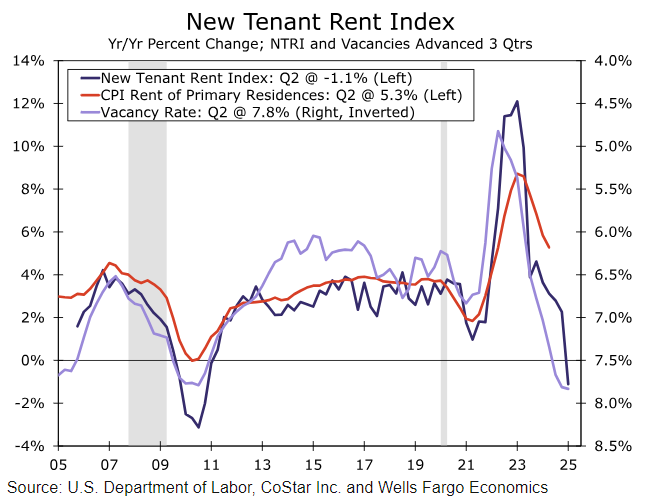

With core goods inflation already running below its pre-pandemic pace, more material cooling in services is needed to continue to drive core inflation lower. Core services prices look to have advanced more quickly in July relative to June, but the 0.25% increase we have penciled in would still be noticeably below the 0.40% average monthly increase over the first six months of the year. We anticipate July's monthly pickup to be driven by the “super core” after June's sharp drop in the volatile travel services category and a below-trend rise in medical care services. However, June's downshift in primary shelter looks to be sustainable based on the BLS's New Tenant Rent Index and private sector vacancies (Figure 2). We look for another 0.3% rise in July and for primary shelter to increase 0.25%–0.30% per month through the end of the year.

Author

Wells Fargo Research Team

Wells Fargo