Reality check: QE isn't working as planned

Reality check: QE isn't working as planned

The path forward comes down to the actions taken by the banks, not the Federal Reserve. This runs contrary to the prevailing narrative we hear today, with pundits presuming the almighty Fed’s actions are indeed central to money creation and inflationary forces in the financial economy. In reality, the Fed is a reactionary entity and therefore can only guide the banking system by incentivizing certain behaviors after recognizing concerns. The Fed may have only thus far only helped create a reflation, falling short of real inflation compared to the pre-pandemic economy.

The Fed can only promote their desire to see rising inflation by incentivizing financial entities to lend more. The Fed only ends up creating inflation if its balance sheet expansion is indeed robust enough to stimulate lending in the banking system. However, it remains a fact that the banks need to act to create inflation. This banks the banks (especially larger primary dealer banks) more central to the banking system and inflation dynamics than the central bank and Treasury officials.

No matter what the Fed does, banks will act in the best interest of their clients and shareholders. No matter how much repo market activity or Treasury issuance is financed via the expansion of the Fed balance sheet, inflation will only rise if the amount of new credit creation in the banking system exceeds the volume of credit destruction taking place. Banks stand committed to holding highly liquid short-term assets, and this becomes clear after analyzing charts included in this report and by the fact that rates remain very low. The Fed and government likely need to do more if they hope to incentivize bank lending and therefore rising inflation and elevated asset prices.

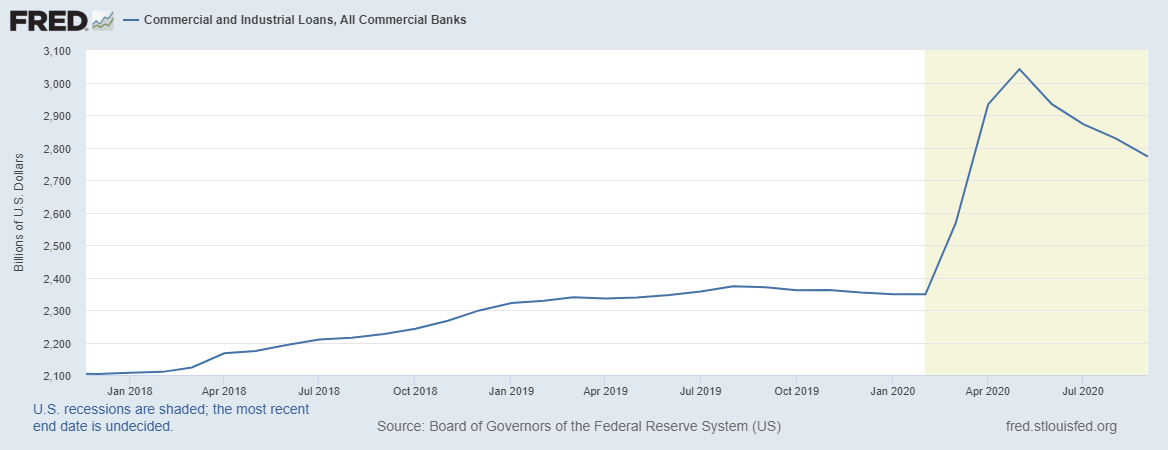

The chart below shows us that commercial banks don’t seem to believe the immediate path forward is one of healthy economic growth and inflation. The number of asset purchases and balance sheet expansion coming out of the Fed is not enough to get the banks committed to their cause.

If the Fed’s actions were stimulative and indeed inflationary thus far in 2020, we would need to see this chart reverse very soon. After peaking in early May, it’s clear banks have been reluctant to lend more as the Fed wishes. The banks have been electing to simply warehouse much of their newly obtained collateral from the Fed instead of using it to keep expanding their loan books.

We can logically infer that the banks on aggregate don’t see the broad economy as being as strong as financial asset prices, mainstream pundits and central planners might want us to believe. Perhaps investors have gotten carried away with the inflation narrative rather than understanding there has only been attempt number one made at a “reflation.”

Remember, the banks are also dealing with a record amount of risky debt on their balance sheets due to the pandemic and resulting economic shutdowns globally. For the Fed to achieve its desired result here, one of two thighs will need to happen. Either they need to further expand their balance sheet, increasing bank reserves and bolstering the already considerable liquidity backstop, or the economy needs to strengthen in real terms. We are still a ways away from meaningful inflation kicking in, and we’ve likely seen asset prices continue to rise in a truly bubbly fashion due to expectations of future inflation.

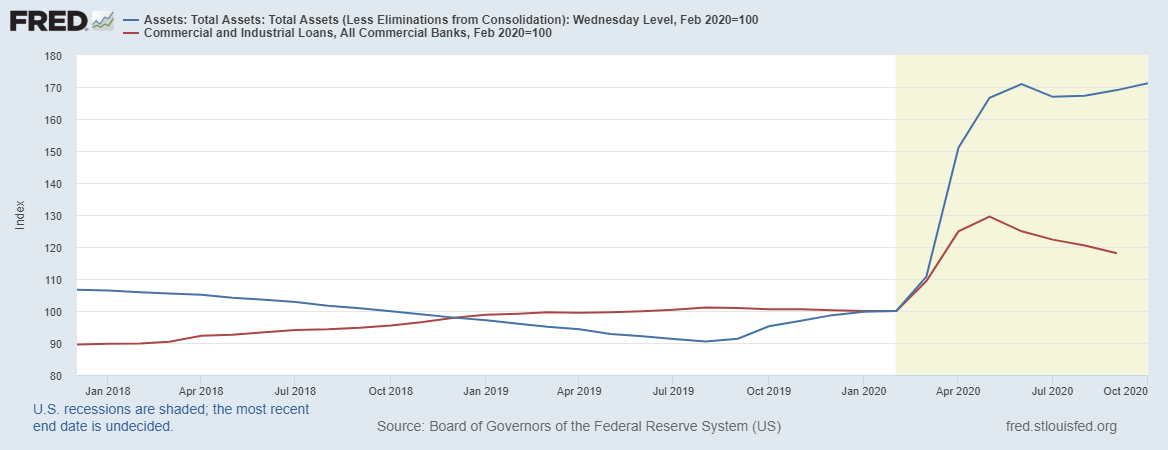

For further evidence that banks aren’t going along with the Fed’s narrative, we can note that the Fed has indeed expanded its balance sheet by half a trillion dollars since the banks began to shy away from their peak loan creation levels in early May. Below, compare the same commercial loan chart from earlier (now in red) to the Fed’s balance sheet expansion (blue).

By indexing the two data sets to February 1st (before the Fed intervened and before the market panicked), it’s clear the Fed’s balance sheet expansion of 501.55 billion dollars since May has resulted in a considerable pullback in bank lending since. We will need to watch and see whether the two values will diverge from here, or if the banks will go along with the Fed’s program like they did back in March and April. For now, it looks like the banks believe markets are ahead of themselves after trying to front-run the Fed.

We can use a simple thought experiment to examine this further. Imagine a scenario where the US economy is strong or has at least recovered to pre-pandemic levels. Financial entities would be quick to grow their loan books in response to a Fed balance sheet expansion and therefore bank reserve increases. Banks would see an opportunity to add productive assets to their balance sheet, supporting an outcome with rising inflation.

Now, contrast that imaginary narrative and confront the reality we face in 2020: loan losses are rising, there are fewer creditworthy households and firms due to a pandemic and economic shutdown. A backdrop of high unemployment and high debt levels is forcing banks into a natural balance sheet preservation mode. This means that since May, banks have been setting up for a deflationary backdrop by holding more liquid assets as opposed to creating new loans in the broad economy and thus stimulating inflation.

Thus far, the Fed has grown its balance sheet by around 3 trillion dollars in 2020 but it is still not enough to stimulate the financial sector and fill the void left behind by the financial crisis. Limited money supply growth via banking sector loan creation is a sign that the Fed is not accomplishing the goals it promised to. Now, ask the question: If the Fed were indeed central to the banking system, would this be the case?

This implies that the necessary conditions to force another deflationary event or mass liquidation remain. The banking sector is not ready to move past this economic recession and pandemic-induced instability quite yet. Remember, gravity has been proven to exist in the past, and we have never proven the Fed can levitate markets forever without the cooperation of the banks, the real agencies central to monetary expansion and economic stability, or lack thereof.

Author

Miles Ruttan

Bytown Capital

Miles' focus at the firm is to oversee our macro analysis, with the emphasis being placed on global credit and liquidity flows.