RBA will hike 25bp in March

Australia Rates Insights - RBA set to deliver another 25bp hike on 7 March, but guidance could have a less-hawkish tilt.

March meeting preview

-

I remain confident the RBA will deliver another 25bp hike on 7 March, despite weaker data this week.

-

However, I think these data could result in policy guidance tilting back in a less hawkish direction.

-

The divergence of economic performances, and in associated policy paths chosen by respective central banks, appears to be growing, with rate hikes biting more sharply in Australia.

RBA board meeting preview (7 March)

I expect the RBA governor’s press release to: i) announce a 25bp hike; ii) contain mixed macro comments; and iii) provide less hawkish forward guidance.

On the macro side, the key recent developments, in my opinion, include stronger-than-anticipated growth and inflation data in Europe and the US. However, the local data (AUS) indicates a growing loss of momentum and shows evidence that inflation pressures have peaked.

I expect comments on the global side to be more upbeat. I believe the RBA may note that recent data suggests brighter outlooks for Europe, the US, and China. The IMF has made similar observations, and I think the RBA pays close attention to IMF forecasts. Although encouraging, this also raises the possibility that the ECB and FOMC rate hikes are biting less than expected, paving the way for further rate hikes by these banks.

I had thought that this signal could keep me on a quite-hawkish path. However, recent local data provides clear evidence of divergence, such that my local macro comments will likely tilt in a more cautious direction. The Q4 GDP data revealed a further slowing of domestic demand and evidence of less intense wage and price pressures. Moreover, the latest monthly CPI inflation data (for January) strongly suggest inflation pressures have peaked, and building approval and housing finance data last week suggest a sharp downturn in dwelling construction ahead.

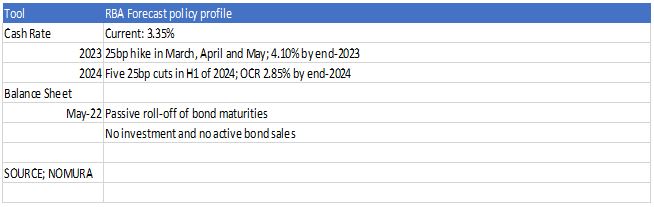

Despite all of this softer data, I still expect a 25bp hike this Tuesday at 14:30 Sydney Time (as 22bp priced already) with follow-up, and final, 25bp hikes in April and May, taking the cash rate to a peak of 4.10%. This reflects an issue of "levels versus change". From the RBA's perspective, while growth and inflation data have lost momentum, the economy is still operating beyond full employment, and the level of inflation remains well above the target band.

Nevertheless, given the local data, I think the RBA's forward guidance will likely tilt back in a less hawkish direction. It appears that the RBA was stung by the sharp rise in trimmed mean CPI inflation in Q4, with data details suggesting no moderation in goods prices, as has been evident elsewhere. The minutes from the last meeting revealed that the board considered whether to hike by 25bp or by a larger 50bp in February before settling on a 25bp move. Its post-meeting press release indicated that the board expected further increases (plural) in the cash rate and over the coming months (implying a greater sense of urgency). I think this statement could be toned down in some way. For example, the governor could simply return to his December guidance, that the board expects to increase interest rates further (singular or multiple) but is not on a pre-set course (allowing more flexibility and suggesting greater data dependence). If he repeats February’s guidance – that multiple hikes are (still) likely over the coming months – I would expect a sharp negative reaction in rates markets.

Author

ACY Securities Team

ACY Securities

ACY Securities is one of Australia's fastest growing multi-asset online trading providers, offering ultra-low-cost trading, rock-solid execution, technologically superior account management and premium market analysis. The key pi