Rates Spark: Reflections on the new phase of this cycle

We’re not sure the 'post-pivot’ phase of this cycle will see greater appetite to buy bonds, at least not this side of year-end. Meanwhile, a surge in supply this week should see yields jump further.

Last ditch supply meets cautious investors

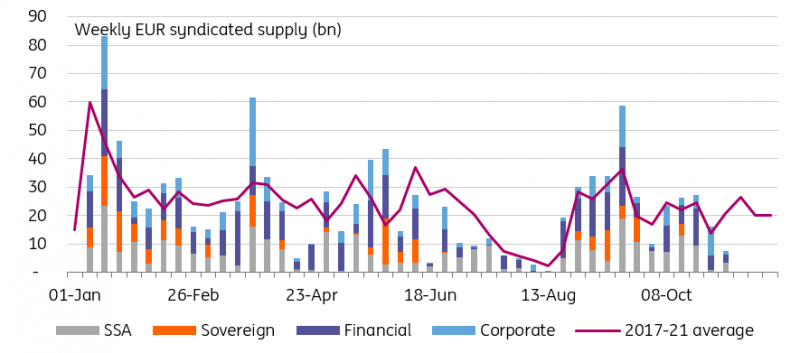

Issuers will probably see today’s relatively light event calendar as an opportunity to return to primary markets after two tumultuous, central-bank dominated, weeks. Thursday’s US CPI report is the next flashpoint, and it will coincide with the sale of $21bn worth of 30Y T-bonds by the Treasury. November is relatively late in the year for borrowers to complete their 2022 funding programmes, but we’d expect that given turbulences earlier this year some will welcome the opportunity to secure some funding. This comes on top of any opportunistic 2023 pre-funding due to a very uncertain outlook.

That’s from the borrowers’ point of view, but what about investors? The past two weeks has been a bruising one with disappointed dovish hopes for the Fed, but with signs that other central banks may take greater notice of looming recession risks. For government bonds, erstwhile described as safe havens, these are mixed messages, but we think caution is likely to be the dominant view. Firstly, because hopes of a shift in central bank rhetoric have been repeatedly quashed by high inflation. Secondly because, as year-end approaches, we expect risk appetite to progressively diminish.

We think the combination of greater supply and still cautious investors means issuance will result in higher yields still. Ultimately, bond direction very much depends on whether data allows for the much hoped-for turn in central banks tightening intention, but we think risks are skewed upwards for yields this week.

The last few weeks of 2022 should see supply impact rates price action

Source: Refinitiv, ING

Slower hikes could mean higher rates for longer

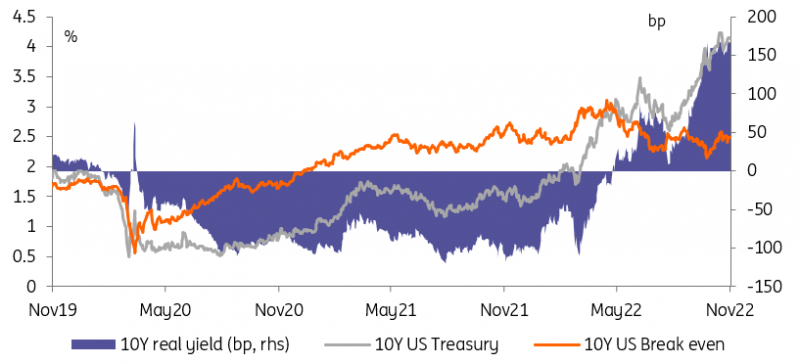

It is also worth reflecting on the implication of the new phase in the fight against inflation. What was widely described as a ‘pivot’ was in fact a signal that what we would describe as the ‘catching up’ phase of this cycle is near its end. During the ‘catching up’ phase, central banks were pretty much on autopilot, hiking in large (up to 75bp) increments as they exited years, or even decades in the case of the European Central Bank, of very loose policy. The new phase promises slower hikes, and more attention being paid to the side effects of tightening. As Fed Chair Powell was at pains to stress, this doesn’t necessarily mean a lower terminal rate.

In fact, it just so happened that news on the inflation front on balance worsened in the run up to last week's Fed meeting, making its message an apparent contradiction. In reality, there is no contradiction. The Fed, and other central banks, can remain hawkish for even longer in the new phase of this tightening cycle if data fails to fall quickly enough. The result, compared to a counterfactual where hikes proceed at a faster 75bp pace, means less risk of an economic, or financial, accident, but it also implies a more protracted hiking cycle. As a result, the ‘area under the curve’, for those with calculus class PTSD, may well end up being greater, meaning rates (on average) higher for longer.

We would challenge the narrative that this should result in higher inflation expectations. In our view, this new phase also reduces the risk of a too early end to this cycle, and so of inflation resurgence. The upshot is, higher real rates, and for longer. This needs not be negative for risk sentiment, if tail risks reduce as a result. A protracted hiking cycle could bring lower inflation expectations, and higher real rates

Source: Refinitiv, ING

Read the original analysis: Rates Spark: Reflections on the new phase of this cycle

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.