Rates spark: Ranges are holding for now

Despite the continued hawkish push, yields have backed down from the top of the post-Silicon Valley Bank ranges. After all, both central bankers and markets are watching the same data. The latest signals have been mixed and the extent of the banking turmoil impact will reveal itself only over time.

Range-bound trading with no clear pointers yet from the data

Rates markets were finding some support as sentiment faltered yesterday. Mind you nothing extraordinary, but together with 10Y yields having failed to push above post-SVB highs it speaks to more range-bound trading in the current environment until markets get more compelling evidence to the degree that the banking turmoil has impacted the economy. Despite some signs that tensions are easing or at least stabilising, one is also aware that some of the downstream effects can come with considerable lags.

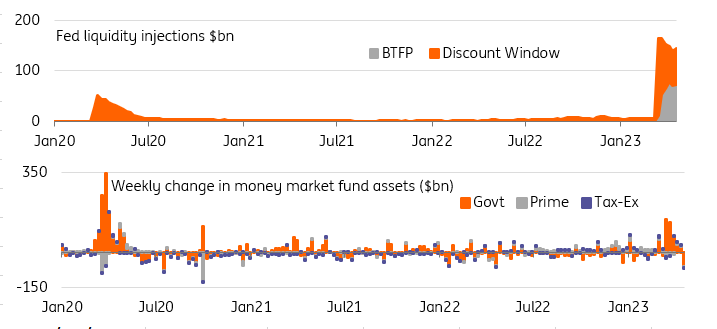

Usage of Fed emergency lending facilities increased

As to the more contemporaneous data more immediately concerning the banking system the Fed reported a small increase in the usage of its emergency lending facilities. It was a small US$4.4bn increase, equally spread over the primary credit and the Bank Term Funding Program, but nonetheless still the first increase after the gradual declines from the initial surge in early March.

Money market funds saw sizeable outflows for the first time since the turmoil with government funds losing more than US$60bn over the last week, reversing the previous two weeks' worth of inflow. This outflow is probably more related to tax payment dates than money market funds losing their safe-haven appeal. Though going forward, one should also be wary of the effects that the looming debt ceiling can have on their perceived safety as the sovereign default probability increases.

Usage of Fed liquidity facilities ticked up this week, and money market funds saw outflows

Source: Refinitiv, ING

Central bank officials remain hawkish on inflation ahead of the upcoming meetings

Most Fed officials have refocussed their sights on the inflation issue now that the acute banking turmoil seems to fade in the rear view mirror. They are trying to gear market expectations towards a higher-for-longer scenario before the quiet period ahead of the May policy meeting begins tomorrow. But Fed officials and markets are largely watching the same data and officials have not been able to offer any new angle in their latest remarks.

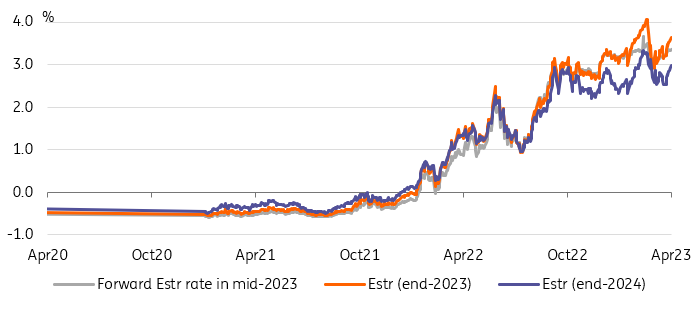

Inflation still ranked at the top of the ECB’s concerns

Relatively speaking EUR rates should have more upside given the European Central Bank's lagging progress in achieving its inflation goals. The ECB did refrain from explicitly stating that rates could further rise at the March meeting in light of the banking turmoil, but from the minutes of said meeting which were released yesterday we now know that inflation still ranked at the top of the ECB’s concerns. And the ECB’s own forecasts have again received criticism with “a number of members seeing risks as tilted to the upside over the entire horizon”. This also explains why we have seen quite a few hawkish comments since then, trying to set the record straight with regards to ECB’s commitment towards reining in inflation. Isabel Schnabel reiterated yesterday that energy aside many other components to inflation are still on the rise.

ECB hike expectations are on the rise as officials voice their inflation concerns

Source: Refinitiv, ING

Data remains key in the weeks ahead

We might well start with today’s PMIs, which should provide some more sense of direction for an economy that is still struggling with high inflation, but also experiencing some tailwinds now that supply chain problems have faded and energy prices have moderated. But the ECB also watches them for evidence of asymmetric pass-through of now declining energy prices. In the minutes it was remarked that PMI survey data pointed to a much slower decline in output prices than in input prices.

Next week: individual country inflation data from Germany, France and Spain ...

Looking into next week, ECB officials will still have a few days to communicate their policy stance ahead of the pre-meeting quiet period. Key data points that officials have highlighted are the next bank lending survey and April inflation data, which will both come in early May ahead just of the ECB meeting. However, already at the end of next week, we will get first individual country inflation data from Germany, France and Spain, which should already provide a good sense of where the aggregate is headed. On the same day we will get a first reading of first quarter GDP.

... PCE inflation and ECI from the US

The Fed will already be in its quiet period by tomorrow, putting even more focus on the data. The key data point to highlight next week is the PCE inflation, which remains the Fed’s preferred measure of inflation, and alongside the emplyoment cost index (ECI) for the first quarter. We will also get a first estimate of first quarter GDP.

Read the original analysis: Rates spark: Ranges are holding for now

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.