Rates spark: Markets relieved by consensus US CPI

The US core CPI number came in at 0.3% MoM, which on an annualised basis still looks too high for Powell. However, markets reacted with relief, causing US rates to move lower. Euro rates are still considering the likelihood of a 50bp cut in December, currently estimated at 20%. Based on OIS spreads, the Bund swap spread may stabilise close to current levels.

Some relief from consensus US CPI reading, but still too high

The market was clearly concerned that the US CPI numbers might have been worse, as evidenced by the drop in yields following a broadly consensus outcome (though slightly different from the whisper number).

Nonetheless, the 3.3% year-on-year core CPI remains an ongoing discussion point, as it is still too high. Federal Reserve Chair Jerome Powell referenced this at last week’s press conference. Despite this, the front end of the curve moved lower as markets perceived more room for potential Fed rate cuts if deemed necessary.

We want to be a tad bullish on USTs due to the Trump-induced backup in rates, which is now significant. But we need a catalyst first. Yesterday's number was a relief as it could have been worse. Historically, we’ve never seen a rate-cutting cycle where the 10-year yield consistently rose after the first cut. Some increase is expected, but not a persistent one like we’re seeing now. We understand the reasons behind this, but it still feels like yields could move back down for a while.

The front end in particular looks to have value. We struggle to understand why it’s persistently drifting higher unless the market is pricing in rate hikes in 2026. Not impossible of course. But quite a leap to discount that now.

Euro rates looking at US and ECB speakers for direction

Euro rates changed slightly on the day but found some relief in the consensus US CPI numbers. With little eurozone macro data to work with and Trump-related risks moving to the background for now, we expect the correlation with US rates to remain strong.

Perhaps European Central Bank speakers can give some direction by sharing insights on the chances of a 50bp cut in the near future. For now markets price in a 20% chance of a 50bp cut in December, which seems reasonable given the rising growth risks. Having said that, more signs of economic weakness are needed to move that needle towards a higher probability.

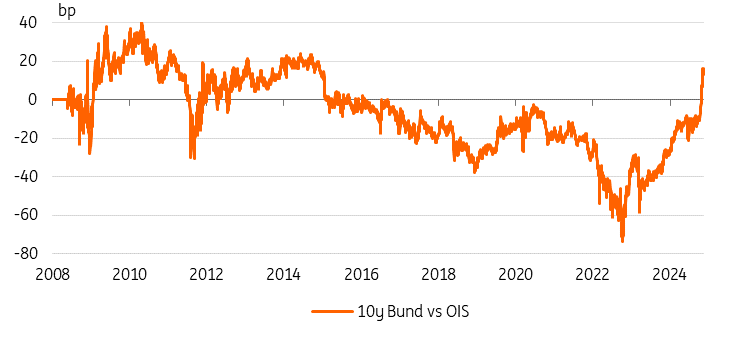

Bund spreads over swaps remain in a precarious situations

Wednesday saw another day of noticeable Bund underperformance relative to swaps. The 10y yield rose to 4bp above swaps but retreated from the 5bp level it briefly reached last week. Last week, we suggested that some stabilisation might be possible based on historical levels versus OIS. We are now largely back to pre-QE levels, which were around 20bp above OIS in 2014 (on an ESTR-adjusted basis), compared to the 17.5bp peak seen in recent days. However, it is important to emphasise that, overall, we see few reasons for Bunds to outperform swaps again.

One issue that markets will have to weigh is how any new government in Germany will handle the debt brake, and for now there are good cases to be made for more spending to tackle Germany’s investment backlog and structural issues. In the end, Germany may well be one of the countries that can afford such spending. Stabilising at around current levels looks possible, but in terms of market sentiment and other structural as well as cyclical factors playing into the Bund spread, the risks of more underperformance versus swaps seem more obvious than those for outperformance.

10y Bund spreads versus OIS are back to pre-QE territory

Source: Refinitiv, ING

Read the original analysis: Rates spark: Markets relieved by consensus US CPI

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.