Rates spark: Italian jitters ill-timed for the ECB

The discount for a 100bp rate hike from the Fed has faded considerably, and we fully agree with that move. We continue to argue that 75bp is enough, based on what we know to date, and based on signals we see in the bond market. Widening Italy/Bund spreads put the spotlight on the ECB's anticipated reveal of its anti-fragmentation tool next week .

US pipeline inflation pressure hits 11%, but expectations and core are easing

We got an 11% handle on US PPI headline inflation yesterday, but core inflation is down, as was in fact the case for core CPI on the previous day. The market reaction was for inflation expectations to ease further down. The 2yr breakeven is now approaching 2.9%. That was 4.5% a month ago! The 10yr breakeven is approaching 2.3%, and also down slightly post PPI. Most of this argues in favour of the Fed sticking with a 75bp hike, and not caving with 100bp.

The curve structure is also showing a separation from a 100bp hike. The inversion on the 2/5yr segment intensified post the CPI yesterday, suggesting that longer tenor market rates are not getting bullied higher by this; which makes sense as inflation expectations have been falling.

The 2/5yr inversion is also holding at post the PPI number, as is the evolution of outright 5yr richness to the curve (albeit mild). No fireworks after this number so far. But there is a separation between the money market discount edging towards a 100bp hike versus the bond market discount out the curve that argues more for a steady 75bp hike.

Either way all of this price action continues to argue that the peak for market rates is in, with inversion (especially on the 2/5yr) suggesting that an acceleration in hikes is in fact not the way to go.

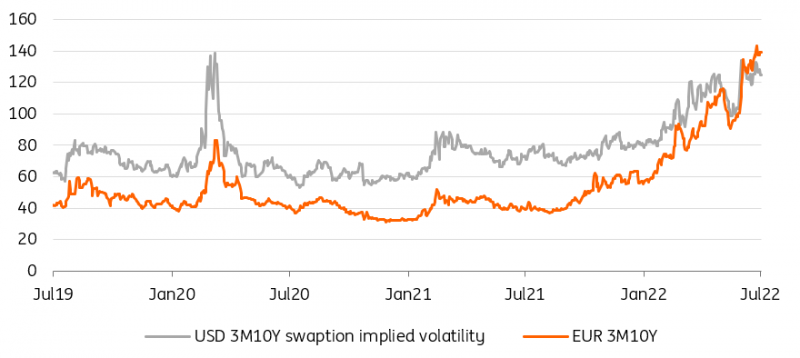

EUR rates are displaying higher volatility than their US counterpart

Source: Refinitiv, ING

EUR curve to follow in the UST’s footsteps?

In yesterday's rates sell-off episode Bunds actually underperformed US Treasuries. It makes sense considering that it is the European Central Bank which has to catch up in its fight to contain inflation. At the same time we would think the eurozone is more exposed to recessionary risks which should limit the relative upside in long-end yields. But as EUR rates are proving more volatile than their US counterpart we suspect that poor market liquidty is doing its part in amplifying current market moves.

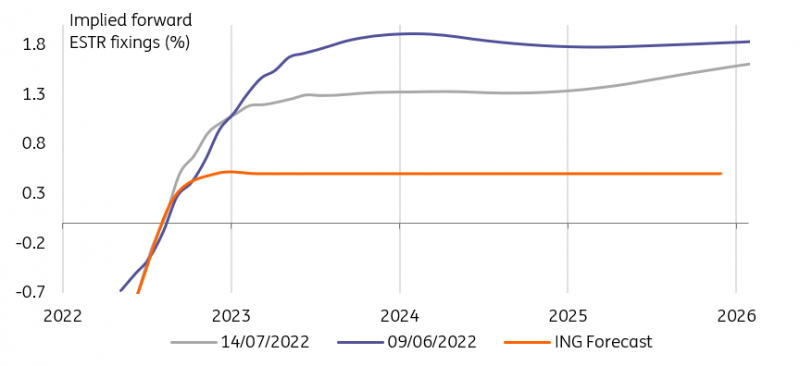

As the curve bear flattened the front end is pricing a growing chance of a larger than 25bp hike from the ECB next week. Some 35bp were priced at points yesterday, some 165bp in total by year-end. The forwards curve is not showing a humped shape, ie, no expectations of a quick pace of tightening to be followed up with rate cuts.

However, we find it premature to make a call for the EUR curve to follow the US curve’s lead towards a structural bear flattening. To us that would also require the ECB actually delivering on the markets expectations of fast-paced policy tightening. We doubt the ECB will be in a position to push through a hiking cycle as aggressively as priced with the economic window of opportunity closing fast.

Markets are pricing a fast pace of tightening for the ECB

Souce: Refinitiv, ING

Italian political jitters at the worst of possible times for the ECB

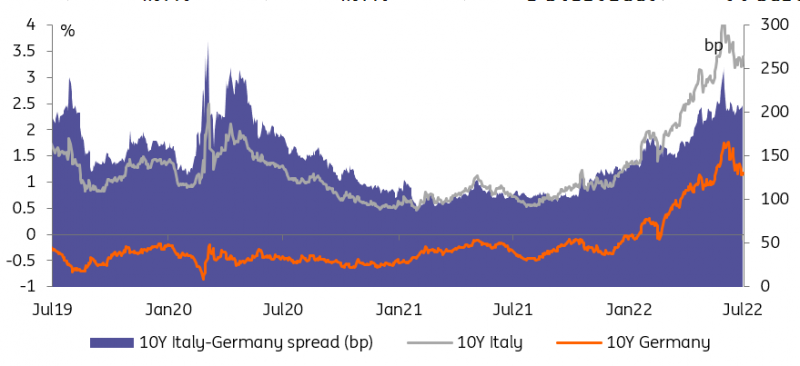

One of the more salient market moves in EUR rates space was the widening of the BTP/Bund spread. The 10Y spread was at times trading close to 20bp wider and it is now well above 200bp again, i.e. in the 'danger zone' of 200-250bp that has prompted verbal interventions from the ECB in the past. With a view to the ECB meeting next week this also pushes the topic of the anti-fragmentation tool into the foreground again. It is not just the timing that is unfortunate for the ECB, but also the nature of the latest spread widening, being rooted in the current political crisis in Rome.

The ECB is expected to flesh out more details of its new tool with which it aims to tackle unwarranted widening of sovereign spreads. However, one can hardly speak of unwarranted widening in the current political situation, which could tie the ECB’s hands at this stage. To make things worse, spelling out too strict conditionalities of the new programme could exacerbate an already fragile situation. But so could staying more reserved on the key details confronting a market that ideally longs for another 'whatever-it-takes' from the central bank.

Though it may not yet be the end of the Italian unity government as this will likely only be decided in the coming week. In any case, political trust will be damaged and for now the possibility of an early election in autumn still looms large.

Political uncertainty adds widening pressure to Italian bonds

Source: Refinitiv, ING

Read the original analysis: Rates spark: Italian jitters ill-timed for the ECB

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.