Rates spark: Hawkish tail risks

The week kicked off with a bearish tone in rates markets, with key central bank decisions just ahead. Ever-rising energy costs only add to fears that the inflation fight is not yet decided. ECB hawks offered more pushback against an overly dovish interpretation of last week's hike, and the focus is shifting to other means of policy tightening than just rates .

A bearish tone in markets to start the week, and a renewed discussion of the ECB balance sheet

Ahead of the key Fed and Bank of England meetings, the week kicked off with a bearish tone in rates. It was, in particular, the front end that showed weakness in the US, with the 2Y US Treasury rate pushing further above 5%. The outlier was the UK, where it was more the belly of the curve and rates further out that led rates higher – perhaps it is the “Table Mountain” comparison used by the BoE’s Chief economist gaining more attention.

But more broadly speaking, it could also be markets bracing for more hawkish tail risks to their longer views. With a view to the European Central Bank, which had signalled that rates had reached a level which, if held long enough, would make a “substantial contribution” to reaching the inflation goals, markets are having second thoughts about their initial dovish interpretation.

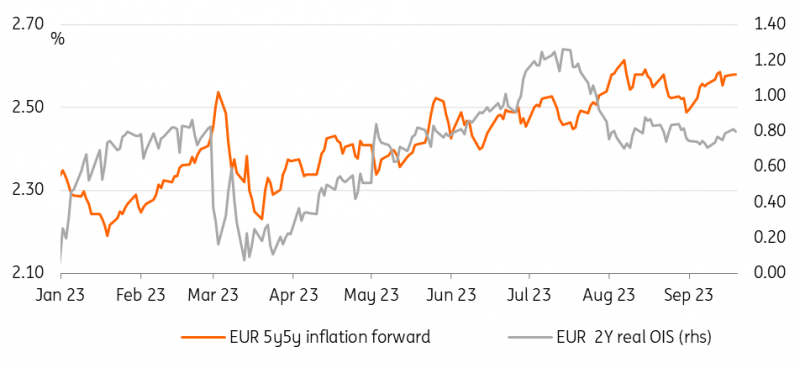

Oil prices are pushing higher, EUR market-based inflation expectations, i.e., longer-term inflation swaps, are not coming down, and real interest rates still remain well below the July highs. The decline of the latter, Isabel Schnabel had cautioned ahead of the European Central Bank's meeting, could counteract the ECB’s inflation-fighting efforts. So it may not be all that surprising to see the ECB’s hawks come to suggest it was too early to call the peak, with some also suggesting now is the time to think about speeding up the reduction of the balance sheet. If rates contribute substantially to reaching the inflation target, can the balance sheet provide the minor remainder that is needed?

Next to the ECB officials’ remarks, the key piece of news yesterday was a Reuters background story that the ECB wants soon to tackle the high level of excess reserves in the banking system. Basically, there are two ways this could be done, either via raising the minimum reserve requirement for banks or via the speeding up of quantitative tightening.

According to the article, several policymakers favour raising the reserve ratio from the current level of 1%, which currently is equivalent to around €165bn, to closer to 3% or 4%. As the ECB recently also decided to drop the remuneration of required reserves to 0%, it would also have the benefit of reducing the ECB’s interest rate costs.

Most saw room to phase out the Pandemic Emergency Purchase Programme (PEPP) by ending the portfolio’s reinvestments earlier. But all were 'nervous' about the potentially negative impact on sovereign spreads. The argument against outright selling of the other portfolios under the Asset Purchase Program (APP) was that it would crystallise mark-to-market losses, highlighting the ECB’s concern with interest rate costs. Perhaps the article's main take-away on quantitative tightening is that any decision might not come this year and would take effect only in “early 2024 or even later in the spring”.

The ECB still has work to do

Source: Refinitiv, ING

Read the original analysis: Rates spark: Hawkish tail risks

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.