Rates spark: Don’t write off the curve flattening trend

We wouldn’t write off the curve flattening trend. Yes, hawkish market expectations are already high, but we fear medium-term growth expectations could deteriorate further. Risk premia could justify a steeper curve but they are already elevated. Once again, the big question is where the neutral rate is for developed economies.

Peak hawkishness? Maybe, but the curve could still flatten

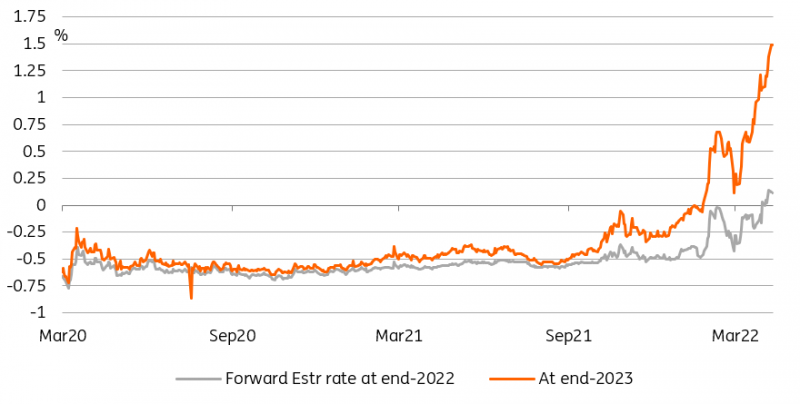

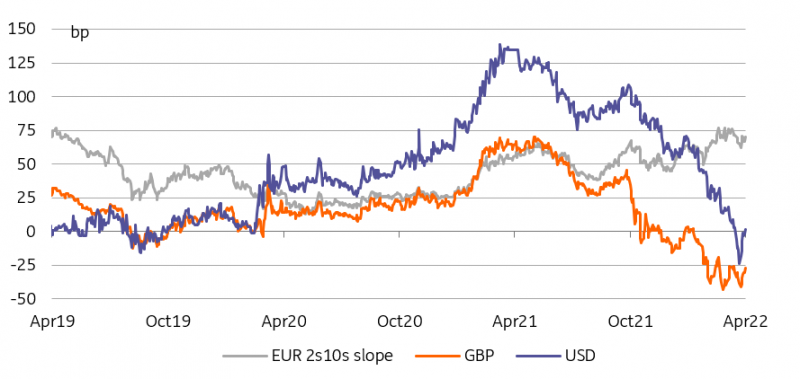

Even with the Fed signalling tightening in 50bp increments and with euro markets running well ahead of the tightening signalled by the ECB, one can reasonably wonder how far front-end yields can go. For reference, the EUR curve is pricing eight 25bp hikes by end-2023. For the US, this figure rises to 11 hikes. This means that on days with large bond sell-offs, the curve tends to steepen. This has helped the USD 2s10s curve dis-invert after a sharp flattening. In EUR rates, this has allowed the EUR curve to remain relatively steep.

Hikes priced by the Estr curve are catching up fast with the US

Source: Refinitiv, ING

Long-end rates have their own anchor in neutral interest rates

Does this mean that the curve flattening trend has run out of road? We’re not so sure. Long-end rates have their own anchor in the market’s view of where neutral interest rates are in each economy. In the US, that figure stands at around 2.5%. In the eurozone, things are less certain with the last tightening cycle being 17 years old, but it is fair to say that the neutral rate estimate should stand well beneath the US’s.

We're not yet giving up on curve flattening

Source: Refinitiv, ING

Risk premia are already high and today’s data should also help flattening

Arguing that the curve must re-steepen can either be justified by a much higher view on the neutral rate, or on a view that the risk premia baked in long-end rates will continue to rise dramatically. That last argument has gained in popularity with the Fed edging closer to balance sheet reduction. One way to assess how much it could rise is by looking at the implied volatility in swaptions. There are more than one maturities to choose from but the conclusion has to be that the interest rate risk priced by markets is already exceptionally high. Nothing says that risk premia can’t be higher still, but we doubt this can be sustained over long periods of time.

Options implied volatility suggests risk premia is already high

Source: Refinitiv, ING

Today’s US CPI, if it shows another upside surprise, has the potential to put the front-end back in the driving seat, and re-flatten the curve. Not only could this push up Fed hike expectations, it would also reinforce fears of a hard landing for the US economy on the joint impact of aggressive policy tightening and fall in real incomes. In the eurozone, the Zew survey is expected to show an even sharper drop in economic sentiment. How markets reconcile this with 200bp worth of hikes in less than two years is hard to see. We think either sentiment recovers quickly, or rates will be proven wrong.

Read the original Content: Rates spark: Don’t write off the curve flattening trend

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.