Quiet week ahead in the markets

Compared to last week’s bumper slate of event risk, this week will be considerably more subdued, influenced not only by limited global asset drivers but also by liquidity thinning ahead of the long Easter weekend.

Core PCE data

The headline event for the week will be the US Core PCE data (the Fed’s preferred measure for inflation), but given that it is released on Good Friday at 12:30 pm GMT, the response to this release could be minimal. The market consensus at the time of writing indicates we will see a slight softening in the MoM print: a rise of +0.3% in February from +0.4% in January, while the YoY release (also for February) is expected to rise +2.8%, matching January. At the headline level, PCE data (MoM) is anticipated to show a slight increase of +0.4% in February from January’s +0.3% reading, along with the YoY print expected to also show a marginal increase from +2.4% to +2.5%. You will recall that the FOMC meeting wrapped up last week, leaving the benchmark lending rate at 5.25%-5.50% for a fifth consecutive meeting (this is the highest rate in more than two decades). Although a no-change was widely expected, the latest Summary of Economic Projections (SEP) revealed that Fed officials continue to foresee three rate cuts this year (there was speculation of a potential downshift to two rate cuts, given the latest batch of inflation numbers). The March economic projections also revealed an upward revision in Core PCE inflation for 2024 from 2.4% (December 2023 projection) to 2.6%, though FOMC participants were unchanged in their projections for 2025 and 2026 at 2.2% and 2.0% (the Fed’s inflation target), respectively.

Other data this week:

US durable goods orders data for February will be released on Tuesday at 12:30 pm GMT. MoM, the current median estimate suggests an improvement from January to February from -6.1% to +1.3%, with durable goods orders (excluding transportation) also expected to show an increase on a MoM basis from -0.3% to +0.4%.

US consumer confidence (Conference Board) for March will be released on Tuesday at 2:00 pm GMT. Expectations indicate that consumer confidence will decrease marginally to 106.5 from 106.7 in February.

US growth GDP data (third estimate) for Q4 2023 will make the airwaves on Thursday at 12:30 pm GMT. Based on the second estimate, real GDP increased to an annualised rate of 3.2% in Q4 2023, with the third estimate suggesting that Q4 real GDP will remain unchanged at 3.2%.

In Asia Pac, Wednesday welcomes the Aussie CPI monthly indicator at 12:30 am GMT. January’s print came in unchanged from December 2023 at +3.4% on a YoY basis, though economists’ estimates suggest inflation to increase slightly at +3.6% in February.

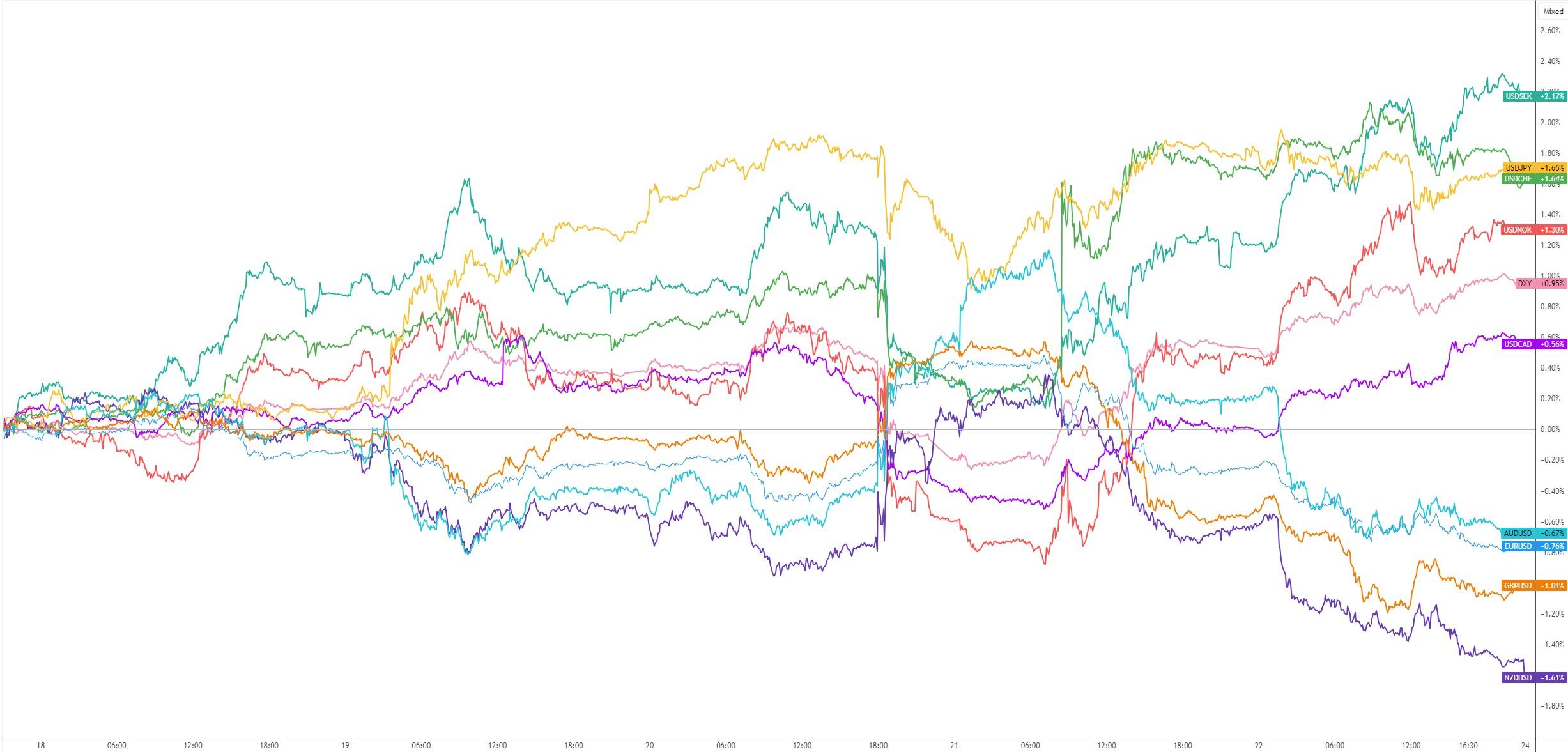

G10 FX (five-day change):

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,