Positive US and Chinese data helping to drive positive sentiment

Market Overview

Positive US data along with strong earnings from Morgan Stanley helped to propel risk appetite yesterday and this has been added to overnight with encouraging economic data out of China. A third month of US retail sales growth and an encouraging reading to the regional Philly Fed survey helped to swing Treasury yields higher, allowing the dollar to recover. Most impressive of all though has been the latest sharp move higher on Wall Street into all-time highs, something which is happening on an almost daily basis. The move has undoubtedly been ushered through via the hand of the liquidity operations from the Fed in recent weeks; however, getting “Phase One” signed, along with positive economic data and a decent start to earnings season have all pushed sentiment to a whole new level. Whilst moves on forex majors still seem to be fairly muted, the yen is once more weakening and there are even signs of a retreat on the strength of the Swiss franc. Oil is beginning to find support again, whilst equities are the place to be right now. Although there are always questions over how long this move can last, for now, the train is still running. Chinese data certainly encouraged overnight. China Q4 GDP was in line with expectations, holding at +6.0% (+6.0% exp, +6.0% in Q3) which meant +6.1% for 2019 . However, following decent trade data for December a few days ago, China Industrial Production also showed strongly at +6.9% (+5.9% exp, +6.2% last), with China Retail Sales also encouraging at +8.0% (+7.8% exp, +8.0%).

There is a clutch of data points to be on top of today on the economic calendar. At 0930GMT UK Retail Sales are expected to grow by +0.5% on an adjusted ex-fuel basis in December (following a -0.6% decline in November), with the year on year data picking up to +2.9% (from +0.8% in November). The final reading of Eurozone inflation is at 1000GMT which is expected to show no change to the headline HICP at +1.3% (+1.3% flash, +1.0% final November), with core HICP to remain again at +1.4% (+1.4% flash, +1.4% final November). On to US data, Building Permits at 1330GMT are expected to reduce slightly to 1.468m in December (from 1.474m in November), and Housing Starts expected to improve slightly to 1.375m (from 1.365m in November). US Industrial Production at 1415GMT is expected to fall by -0.2% in the month of December (after an increase of +1.1% in November), with Capacity Utilization dropping back to 77.1% (from 77.3% in November). Finally, the prelim reading of Michigan Sentiment in January is expected to tick slightly higher to 99.3 (from 99.2 in December), with the Michigan Current Conditions component expected to drop a touch to 115.0 (from 115.2) and Michigan Expectations component to improve to 89.0 (from 88.9).

There are more Fed speakers today with the Patrick Harker (voter, mild hawk) at 1400GMT, and Randall Quarles (voter, centrist) at 1745GMT.

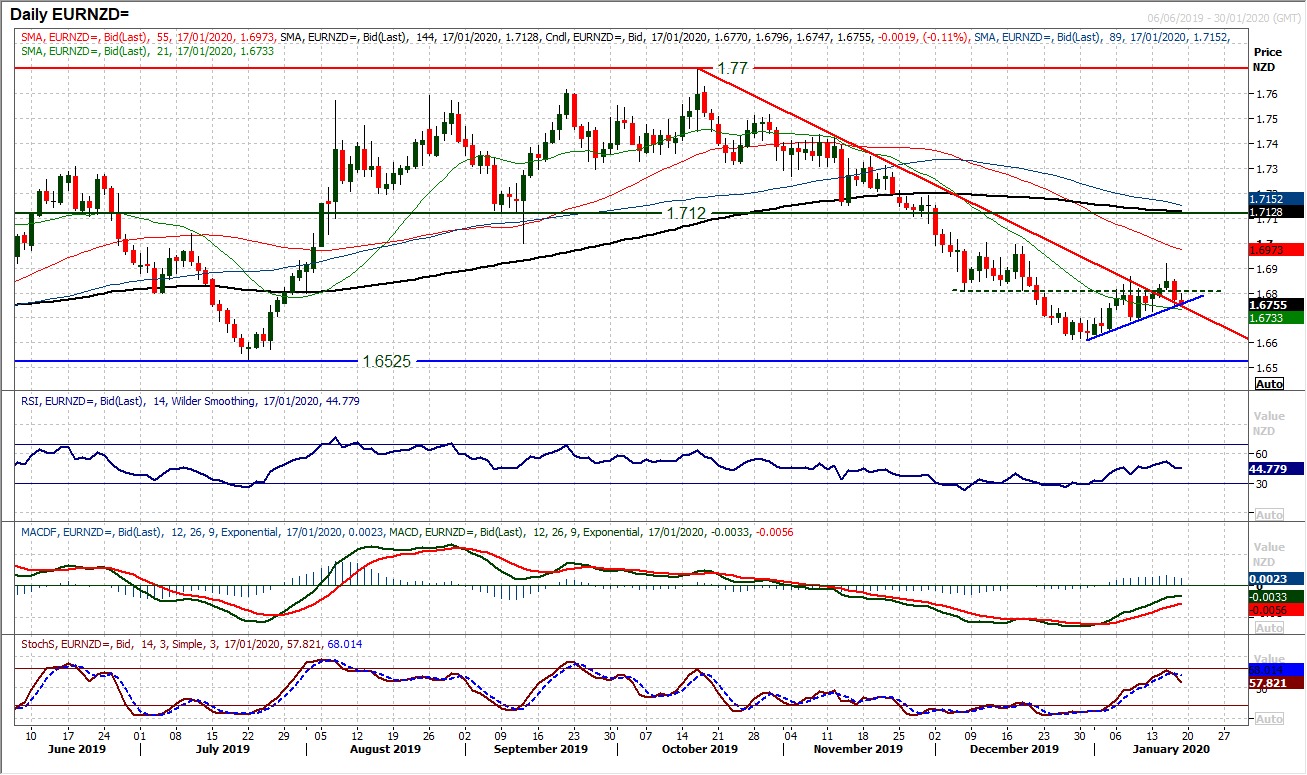

Chart of the Day – EUR/NZD

We have been looking at the recovery of the euro recently, and when crossed with a corrective looking Kiwi, this has driven a rebound on EUR/NZD. However, the move has been questioned by a sharp bear candle yesterday which suggests the market is at a key turning point. Until now, in the past couple of weeks, near term corrective slips have been bought into. This has formed an uptrend whilst also breaking a three month downtrend. Both trendline were tested yesterday and held into the close. This test continues this morning. Momentum indicators have been in decisive recovery mode, but has yesterday’s bearish session been a turning point? The RSI holding above 40 (the point where the recent higher low turned higher) is important now. The 21 day moving average is a gauge of support (currently 1.6735), but if the market continued lower today to breach the higher low at 1.6690 then it would suggest a euro recovery is still some way off. The bulls will subsequently see the near to medium term pivot around 1.6810 as a gauge, to regain upside initiative. The confluence of trendlines will also gauge the level of support for the recovery.

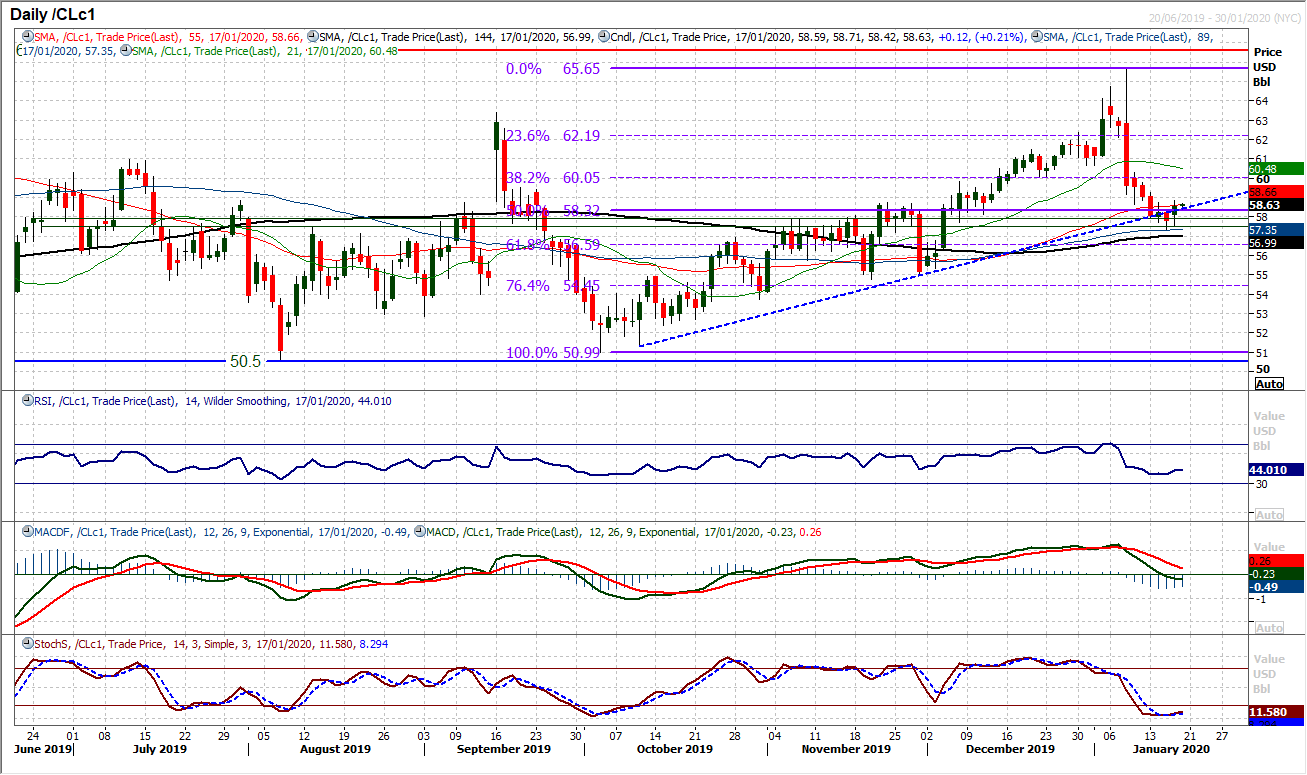

WTI Oil

The last few sessions have hinted that oil could now be building support once more. A massive retracement of the December into January rally has been seen over the past week and a half, but there are signs of stabilisation. Two positive candles in the past three sessions is suggesting a shift in market sentiment. Whilst the $57.50/$57.85 pivot band may not have been solid to the cent, it has still acted as a strong gauge and once more seems to be tempting the bulls back in. With the RSI again beginning to swing higher (from a shade under 40) as it has done on several occasions in recent months, this could be another corner being turned. The hourly chart shows a decent pick-up yesterday above resistance at $58.70 which now needs to be traded clear for the bulls to generate recovery momentum. The old resistance around $60.00 then needs to be negotiated.

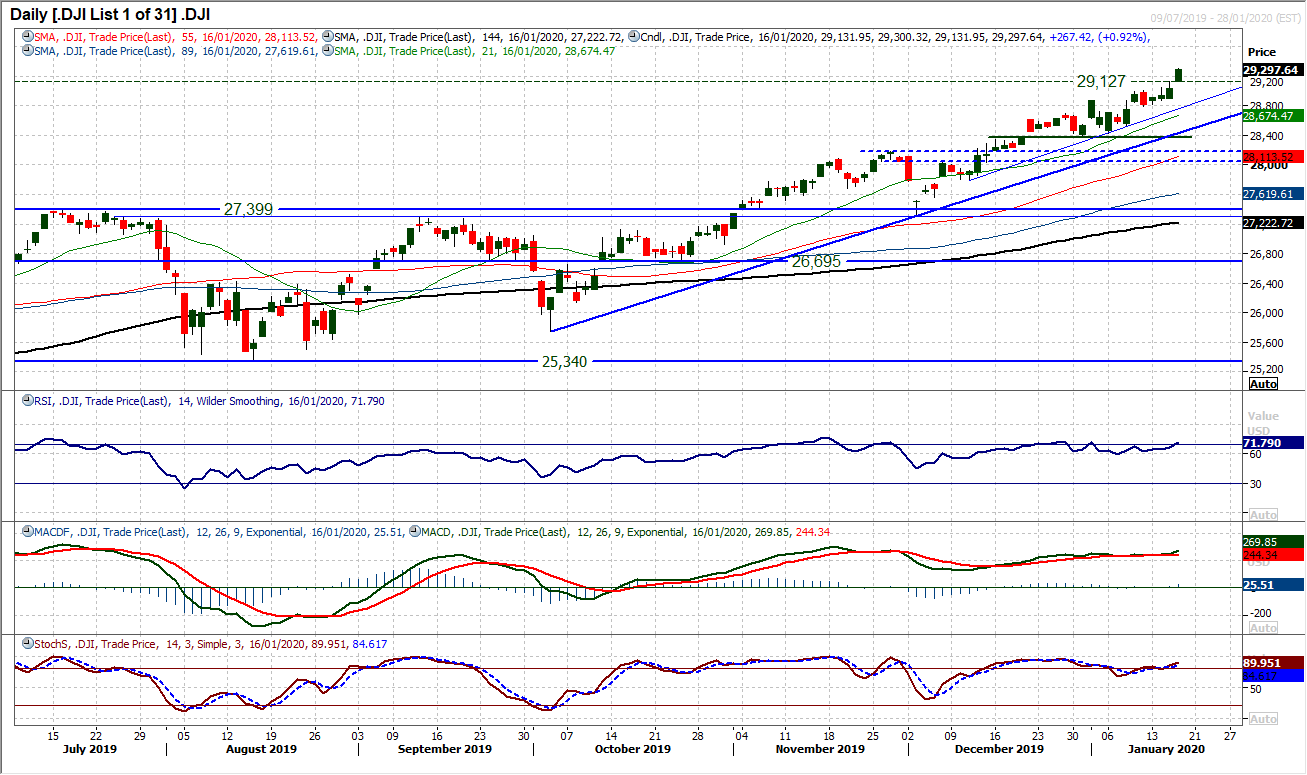

Dow Jones Industrial Average

There seems to be nothing to stop the Dow at the moment as new all-time highs are being posted on almost a daily basis (in five of the past six sessions). The latest breakout came with a gap higher and a close all but at the high of the day. Momentum is strong, with the RSI ticking back above 70 whilst MACD lines are edging higher again (after a period of being flat) and Stochastics are also strong. Intraday weakness has been seen as a buying opportunity for almost three weeks now. In ten of the past twelve sessions there has resulted in a positive one day candlestick. There is a breakout band of support 28,789/29,010 and with a five week uptrend sitting at 28,790 today there is much for the bulls to be positive about. In the absence of any exhaustion signals we are happy to stick with the trend higher.

Author

Richard Perry

Independent Analyst