Poland opens 1Q20 data releases

FX market developments

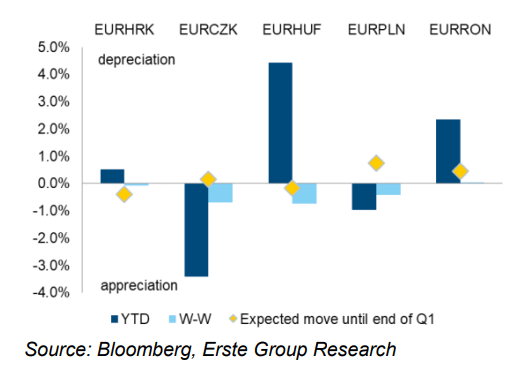

As the USD appreciated to levels not seen for nearly three years, CEE currencies also moved – but this move was, counter-intuitively, appreciation. We think this has to do with inflation reaching levels not seen for nearly a decade, and markets could think that central bankers may react. The CNB and MNB already did this; the former in a transparent fashion, the latter in a much more nontransparent way. Thanks to this, the forint nearly became the best performer last week. The Polish zloty also gained, despite the fact that the NBP is unlikely to hike. We think that the zloty, forint and koruna are all unlikely to gain in the near future, but the CZK could appreciate later this year.

Bond market developments

Bund yields finished the week close to levels where they started it, but some CEE countries showed stronger moves. 10Y HGB yields went up substantially, thanks to the MNB making it clear that they are already tightening and are willing to continue if needed. Shortterm rates also went up, which makes us think that the 3M Bubor could be around 70-80bp in the rest of 2020. Polish yields went up a bit too, but this move was much smaller. ROMGB yields continued to edge down, amid strong demand at bond auctions. We are thinking about our yield forecasts, but want to highlight that a 40% pension increase is still penciled in as of September. In the meantime, the budget deficit was already above 4% of GDP last year.

Author

Erste Bank Research Team

Erste Bank

At Erste Group we greatly value transparency. Our Investor Relations team strives to provide comprehensive information with frequent updates to ensure that the details on these pages are always current.