Pakistan: Heightened risk despite agreement with IMF

The IMF and the Government of Pakistan have reached an agreement to complete the combined 7th and 8th reviews of Pakistan’s Extended Fund Facility which has been interrupted since March. If the IMF Executive Board approves the deal in the coming weeks, Pakistan will receive the equivalent of almost USD 1.2 billion. An extension of the support programme from September 2022 to June 2023 could allow the country to receive an additional SDR 720 million (i.e. approximately USD 947 million).

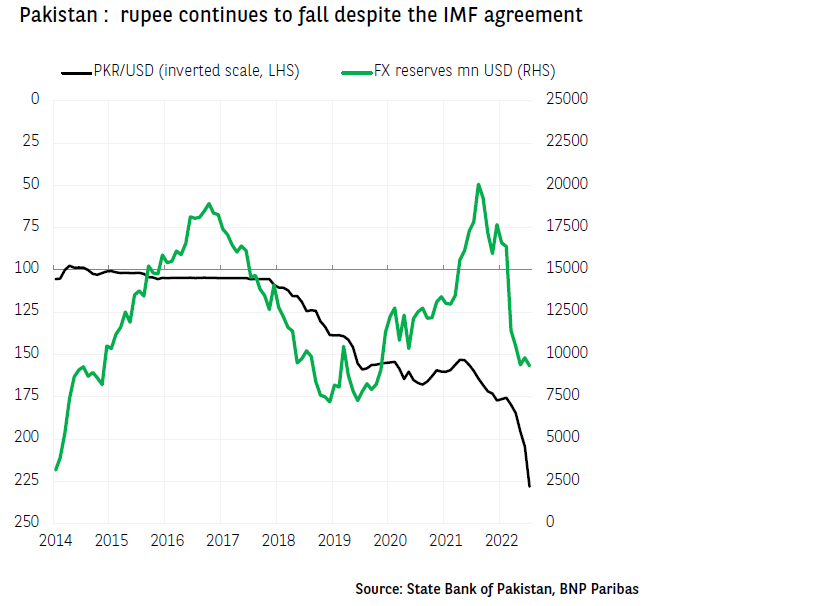

Although this agreement will partially and temporarily ease pressure on the country’s external accounts, the risk of a balance-of-payments crisis remains high. The high pressures on the Pakistani rupee have not eased. Despite increases in the key rate by the central bank (+800 bp since one year ago), the rupee has depreciated by more than 30% against the dollar over the last 12 months. Furthermore, unless the fall in commodity prices seen in recent weeks is sustained, the country’s external position should continue to deteriorate. Foreign exchange reserves amounted to only USD 9.3 billion in mid-July, equivalent to just one month of goods and services imports. To put things into perspective: the repayments of external debt for the 2022/2023 financial year, which will end on 30/06/2023, total USD 21 billion.

However, signing the agreement with the IMF could help to restructure the government’s debt with its main creditors, Saudi Arabia and China.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.