“Not so fast” Federal Reserve puts a pause on future rate cuts

Recent economic indicators and Federal Reserve statements have impacted market outlooks in the USA. What started as hopeful anticipation for a “soft landing” and imminent rate cuts swiftly shifted gears in January, challenging assumptions and reshaping market sentiments.

In my December article, Jerome Powell and the Federal Reserve suggested that inflation had eased over the past year, while remaining elevated, but economic growth had slowed from the third quarter’s strong pace. The market’s interpreted this news as a sign that rate hikes were over and that a “soft landing” was imminent. We saw USD depreciate, against all major currencies, in anticipation that the first interest rate cut was in play for the March 2024 FOMC meeting.

Validating the importance of monthly economic data, we’ve witnessed in January, that it was premature to think that the Fed would start their rate reduction policy as early as March. The year started with a strong CPI figure on January 11th. The Consumer Price Index rose to 3.4%, for the 12-month period ending December 2023. This was a larger than expected increase from the previous month’s CPI Report, which came in at 3.1%, for the 12-month period ending in November.

Subsequent to this announcement, Fed Governor, Christopher Waller, was quoted a few days later on Jan. 16th, stating “there was no reason to move quickly and cut rates as rapidly as in the past”. (Source BBG) We began to see USD appreciation taking hold, as the sentiment began shifting toward US interest rates remaining elevated and staying steady for longer than anticipated at year end.

This USD appreciation continued throughout the balance of January culminating with Fed Chairman Powell, speaking on the 31stafter the FOMC meeting. As expected US interest rates were unchanged with the benchmark fed-funds rate remaining steady in the range of 5.25% - 5.50%. In his speech after the decision was announced, he stated “The Federal Reserve does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably towards 2%” (Source BBG). In the same speech, Chairman Powell also stated “We’re not declaring victory at all. I don’t think it’s likely that the committee will reach a level of confidence by the time of the March meeting” (Source BBG). So the overall sentiment was clear. The Fed is not going to rush into a rate reduction policy until they’re comfortable that inflation data continues to progress towards their goal of 2%. The overall market sentiment is shifting focus on the first rate cut to take place now in May.

This was followed by the US January Jobs Report and unemployment figures, which were released on Friday, Feb 2nd. The US added more jobs in January than were expected. The expectation was for job growth to be at 185,000 and the number came in almost double at 353,000. The unemployment figure came in at 3.7%, lower than the anticipated rate of 3.8%. There were also upward revisions to original December jobs growth figures. Again, another confirmation that monthly economic data dependency will prevail to address the timing of a shift to rate reduction policies in the US.

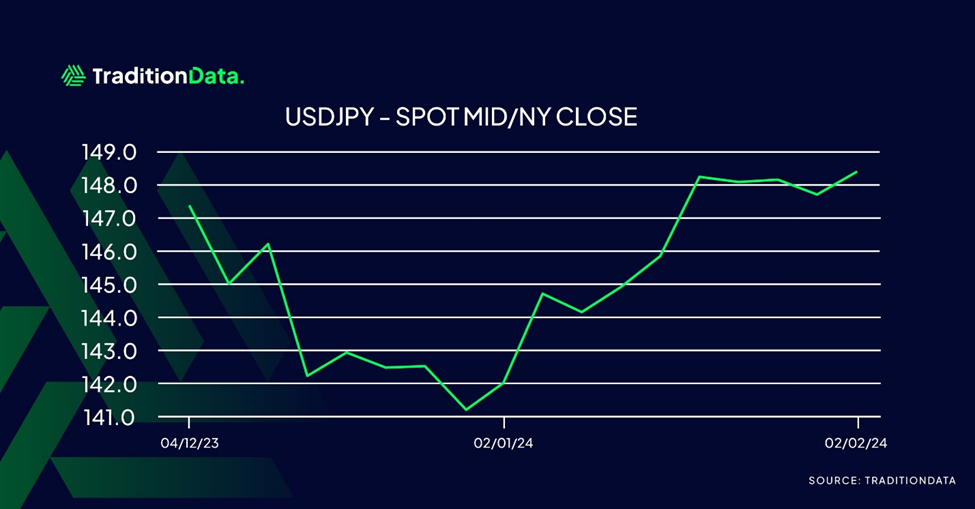

The below chart highlights a complete reversal of USDJPY over the two month period from Dec 2023-Jan 2024. USD depreciated in December, against JPY, based on the market sentiment that US rate hike policy had come to an end, and that rate cuts were imminent in early 2024. Concurrently in December, the Bank of Japan’s Governor Ueda, spoke about preparing for the end of Yield Curve Control (YCC) as well as their negative rates policy. In January, we saw a reversal of this trend as USD appreciated and recovered the ground it lost on JPY, based on the US inflation markers mentioned above.

This data has been compiled using TraditionData’s FX market data (Spot/Mid-rate), at 3pm EST (Monday and Friday), for each week Dec 4th, 2023 – Feb 2nd, 2024.

At TraditionData, we pride ourselves on our global footprint with local market expertise through our relationship with Tradition’s experienced broking business. We offer extensive coverage across Dollar, Yen, GBP and Euro-based products covering, FX spot / forwards, interest rate derivatives and inflation markets. Get in touch to find out how our OTC market data products can power your business, trading and risk decisions.

Author

Sal Provenzano

TraditionData

Sal Provenzano Is the FX Product Manager for the TraditionData business and has been tasked with shaping the future of the FX product range.